Aquamarine Capital Management Portfolio in 2026: Top Holdings & Recent Changes

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

Aquamarine Capital Management continues to showcase disciplined value investing inspired by Guy Spier's approach at Aquamarine Zurich AG. Their $147.5M Q4 2025 portfolio reflects aggressive portfolio reshaping with 100% turnover, shrinking from 14 to just 7 ultra-concentrated positions while trimming major holdings significantly.

Portfolio Snapshot: Extreme Concentration Amid Major Overhaul

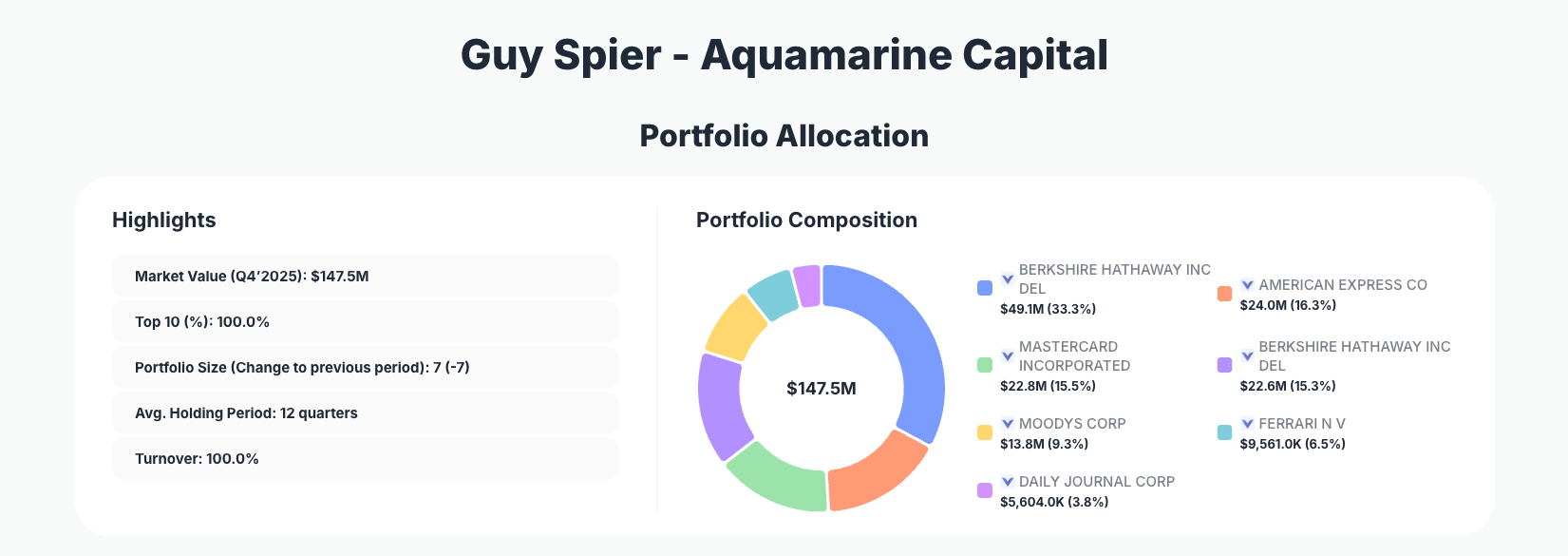

Portfolio Highlights (Q4 2025): - Market Value: $147.5M - Top 10 Holdings: 100.0% - Portfolio Size: 7 -7 - Average Holding Period: 12 quarters - Turnover: 100.0%

Aquamarine Capital Management's Q4 2025 portfolio demonstrates extreme concentration, with the top 10 holdings comprising the entire portfolio at 100%. This ultra-focused approach—now just 7 positions after slashing 7 holdings—signals high conviction in a select group of quality compounders, even as the fund manager executed dramatic reductions across core names. The 100% turnover rate underscores a proactive rebalancing, likely responding to valuation shifts or opportunity costs in a volatile market environment.

Despite the high turnover, the average holding period of 12 quarters reveals underlying patience with surviving positions, blending long-term ownership with tactical adjustments. This strategy mirrors Guy Spier's philosophy of owning exceptional businesses at reasonable prices, maintaining exposure to financial moats while streamlining for efficiency. Investors tracking this portfolio can glean insights into when even top-tier holdings warrant trimming.

The portfolio's contraction from 14 to 7 positions amplifies risk through concentration but also potential upside from oversized bets on proven winners. With every dollar allocated to just these few names, Aquamarine prioritizes depth over diversification, a hallmark of managers who deeply understand their holdings.

Top Holdings Breakdown: Reductions Dominate the Action

The portfolio's largest position remains BERKSHIRE HATHAWAY INC DEL at 33.3%, though significantly reduced by 30.58%, signaling profit-taking on the conglomerate's strength. AMERICAN EXPRESS CO follows at 16.3% after a sharp 69.05% cut, potentially locking in gains amid consumer spending pressures. MASTERCARD INCORPORATED holds 15.5% following a 39.16% reduction, maintaining payment network exposure but at lower weight.

A second BERKSHIRE HATHAWAY INC DEL tranche sits at 15.3% with no change, suggesting differentiated conviction between share classes. MOODYS CORP 9.3% and DAILY JOURNAL CORP 3.8% both remain unchanged, anchoring the portfolio with steady credit ratings and software plays. FERRARI N V was halved to 6.5% via a 50% reduction, trimming luxury auto exposure.

Notably, Seritage Growth Properties (SRG) was completely sold at 100%, exiting the REIT entirely and contributing to the portfolio's shrinkage. These moves across Berkshire, Amex, Mastercard, and others highlight a deliberate de-risking while preserving core quality names like Moody's and Daily Journal.

What the Portfolio Reveals About Guy Spier's Strategy

Aquamarine's Q4 moves paint a picture of disciplined risk management in a high-valuation environment: - Quality moats prioritized: Heavy emphasis on financial services (Amex, Mastercard, Moody's) and conglomerates like Berkshire, favoring durable competitive advantages. - Profit-taking discipline: Massive reductions (e.g., 69% in Amex, 50% in Ferrari) show willingness to sell winners when valuations stretch. - Ultra-concentration for alpha: 100% in top holdings reflects conviction that a few great businesses outperform diversification. - Long-term orientation: 12-quarter average hold supports buy-and-hold with periodic trims, not frequent trading.

This sector skew toward finance (over 70% exposure) and consumer luxury suggests optimism for economic resilience but caution on overextended multiples.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Portfolio Concentration Analysis

| Position | Value | % of Portfolio | Recent Change |

|---|---|---|---|

| BERKSHIRE HATHAWAY INC DEL | $49.1M | 33.3% | Reduce 30.58% |

| AMERICAN EXPRESS CO | $24.0M | 16.3% | Reduce 69.05% |

| MASTERCARD INCORPORATED | $22.8M | 15.5% | Reduce 39.16% |

| BERKSHIRE HATHAWAY INC DEL | $22.6M | 15.3% | No change |

| MOODYS CORP | $13.8M | 9.3% | No change |

| FERRARI N V | $9,561.0K | 6.5% | Reduce 50.00% |

| DAILY JOURNAL CORP | $5,604.0K | 3.8% | No change |

| Seritage Growth Properties | $0.0 | 0.0% | Sell 100% |

This table underscores Aquamarine's extreme bet on just seven names, with Berkshire commanding nearly half the portfolio across two classes despite trims. The 69% slash in American Express and full SRG exit highlight aggressive portfolio pruning, reducing overall size by 7 positions while boosting concentration—the top three alone claim 65% of assets. Such positioning amplifies returns from winners like stable Moody's and Daily Journal but heightens vulnerability to sector-specific headwinds in finance.

The unchanged core (Berkshire Class A, Moody's, Daily Journal) provides ballast amid the turnover, suggesting these as permanent capital allocations. This structure demands deep conviction, as any single misstep could materially impact performance.

Investment Lessons from Aquamarine Capital Management's Approach

Aquamarine's Q4 filing offers timeless principles from Guy Spier's value investing playbook: - Trim winners ruthlessly: Even stellar names like Amex (69% cut) get reduced when valuations demand it—discipline over attachment. - Concentrate on understood businesses: 100% in top holdings shows diversification is for the uninformed; focus generates superior long-term results. - Long holding periods build wealth: 12 quarters average proves patience compounds returns in quality compounders like Moody's. - Turnover serves strategy: 100% churn isn't trading frenzy but active management—exit laggards like SRG, refine winners. - Quality moats over growth hype: Finance-heavy tilt favors predictable cash flows from Mastercard and Berkshire over speculative bets.

Looking Ahead: What Comes Next?

With 100% turnover and a shrunken 7-stock portfolio, Aquamarine appears poised for selective redeployment, potentially into undervalued moats overlooked in the late-2025 rally. Cash raised from trims (e.g., massive Amex and Ferrari sales) positions the fund to pounce on dips in financials or consumer names. Current holdings like dual Berkshire stakes and Moody's set up for steady compounding if rates stabilize.

Watch for opportunities in beaten-down quality amid 2026 volatility—Spier's history suggests bargains in admired businesses. The streamlined structure enhances agility for new convictions, though full allocation implies limited dry powder unless further sales materialize.

FAQ about Aquamarine Capital Management Portfolio

Q: Why did Aquamarine slash positions like American Express by 69% and Ferrari by 50%?

These reductions likely reflect profit-taking on elevated valuations after strong runs, freeing capital while retaining meaningful stakes. The 30.58% Berkshire trim follows similar logic, balancing conviction with risk control in a concentrated book.

Q: What does 100% top-10 concentration and 100% turnover reveal about their strategy?

It signals ultra-high conviction in a handful of quality names, with turnover enabling tactical shifts without abandoning long-term holds (12-quarter average). This isn't day-trading but disciplined rebalancing for optimal positioning.

Q: Why the complete exit from Seritage Growth Properties (SRG)?

The 100% sell-off eliminated REIT exposure, possibly due to property market concerns or better opportunities elsewhere, streamlining to pure-play quality compounders.

Q: How does the finance-heavy tilt (Amex, Mastercard, Moody's) position them?

This focus bets on resilient moats in payments, credit, and ratings amid economic cycles, prioritizing predictable earnings over cyclical sectors.

Q: How can I track Aquamarine Capital Management's 13F filings and follow their moves?

Use ValueSense's superinvestor tracker at aquamarine-zuric for real-time 13F updates—note the 45-day reporting lag means positions are snapshots. Combine with our intrinsic value tools to analyze their holdings like Berkshire or Mastercard for your portfolio.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2026)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!