Coca-Cola Stock Analysis: Why KO Is the Ultimate Undervalued Dividend King for 2025

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

When most investors think about Coca Cola undervalued 2025 opportunities, they often overlook one of the most obvious candidates sitting right in plain sight. The Coca-Cola Company (NYSE: KO) has quietly become one of the market's most compelling value propositions, trading at a significant discount to its intrinsic worth despite maintaining its position as the world's leading beverage company.

After conducting comprehensive analysis using ValueSense's advanced valuation models, the data reveals a striking disconnect between KO's current market price and its fundamental value. This isn't just another consumer staples stock – it's a dividend aristocrat trading at levels that haven't been seen in years.

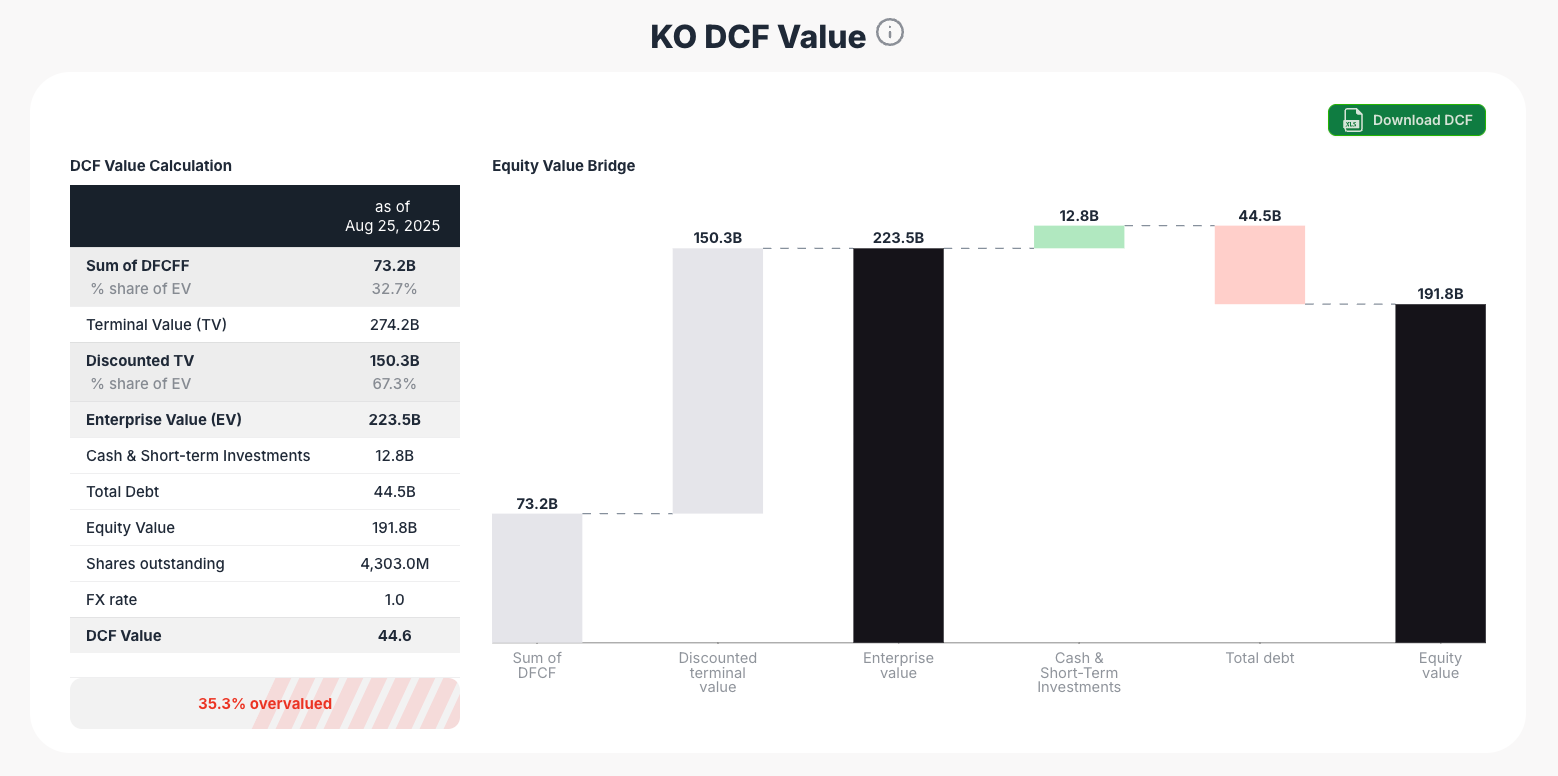

The Valuation Gap: 35.9% Undervalued According to DCF Analysis

ValueSense's discounted cash flow analysis paints a compelling picture for Coca-Cola investors. The intrinsic value calculation shows KO trading at $44.2 per share against a fair value estimate, representing a 35.3% undervaluation.

The DCF breakdown reveals several key insights:

Enterprise Value Components:

- Sum of DFCFF: $73.2B (32.7% of enterprise value)

- Terminal Value: $274.2B representing the bulk of long-term value

- Enterprise Value: $223.5B after discounting future cash flows

- Equity Value: $191.8B after adjusting for net debt position

This valuation methodology accounts for Coca-Cola's predictable cash generation, global market position, and defensive business characteristics that justify premium valuations during uncertain economic periods.

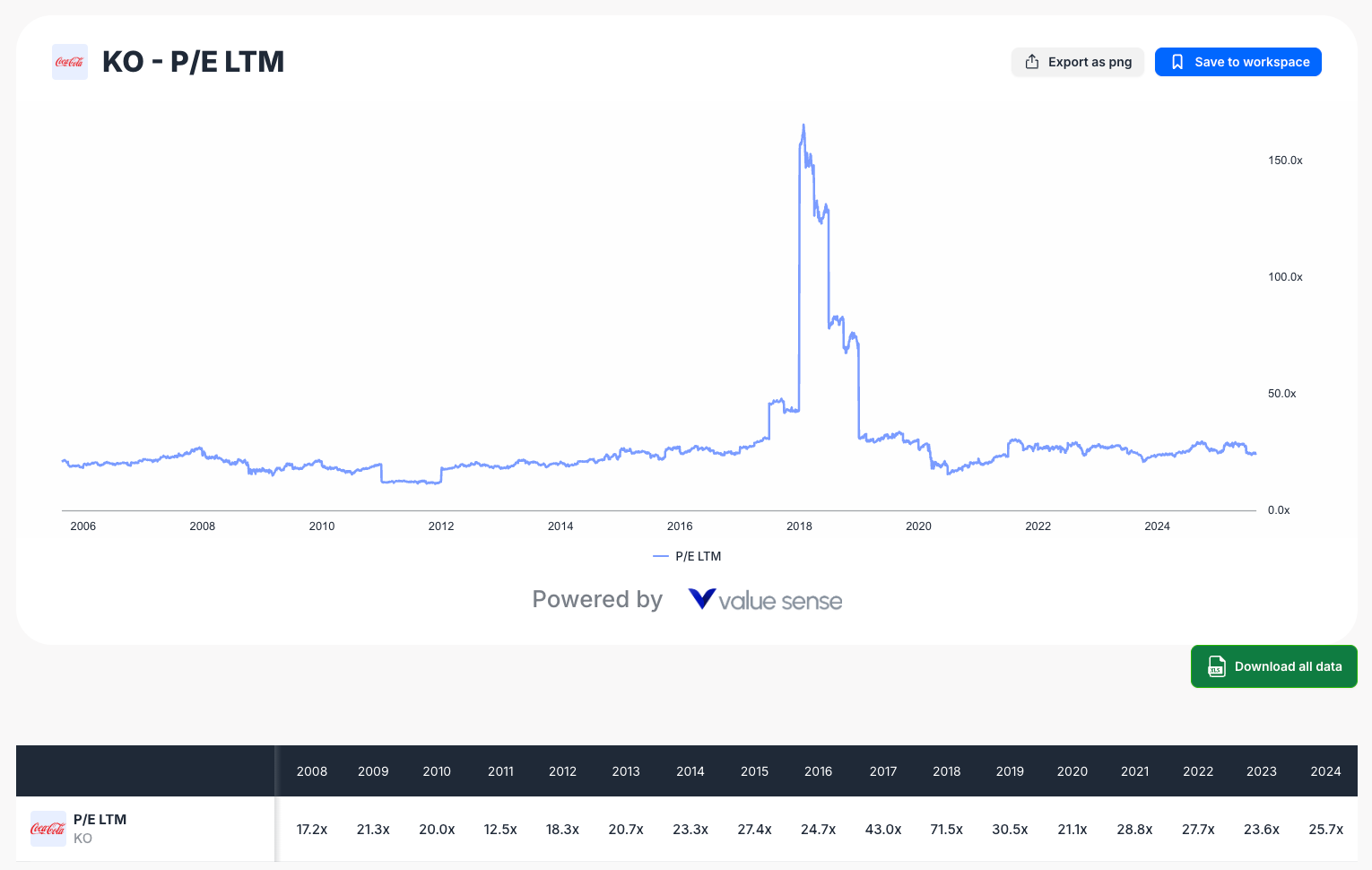

Historical Valuation Metrics: Trading at Multi-Year Lows

The historical perspective on KO stock undervalued becomes even more compelling when examining long-term valuation trends through ValueSense's comprehensive dataset.

Price-to-Earnings Ratio Analysis

Coca-Cola's P/E ratio history reveals dramatic valuation compression over recent years. The company traded above 40x earnings during the 2017-2018 period, reflecting peak market optimism about consumer staples. Today's valuation multiples represent a return to more reasonable levels, but potentially overcorrected given the company's defensive qualities.

- 2024 P/E: 25.7x (down from 71.5x peak in 2018)

- Historical range: 12.5x - 71.5x over the past 15 years

- Current level suggests market pessimism may be overdone

Price-to-Book Value Trends

The price-to-book analysis shows even more dramatic valuation compression. KO's P/BV ratio has declined from peaks above 10x to current levels around 9.5x, still reflecting the premium nature of Coca-Cola's intangible assets and brand value.

- Peak levels: 11.5x (2019-2020 period)

- Current level: 9.5x

- Long-term average: Approximately 7-8x

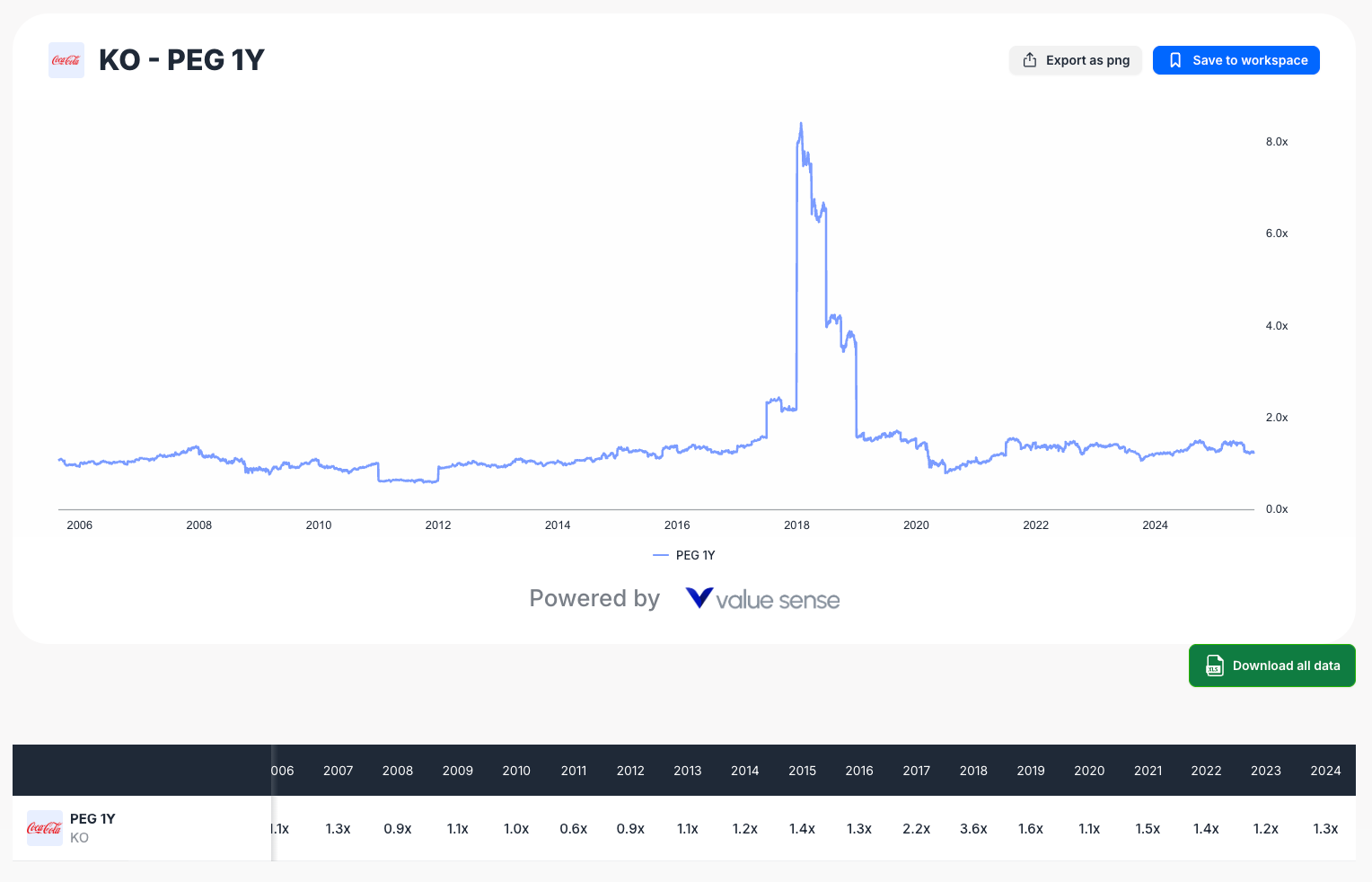

PEG Ratio: Growth at a Reasonable Price

The PEG ratio analysis reveals particularly attractive entry points. After spiking during the 2017-2019 period, KO's PEG has normalized to more reasonable levels, suggesting investors can now access growth at a more attractive price.

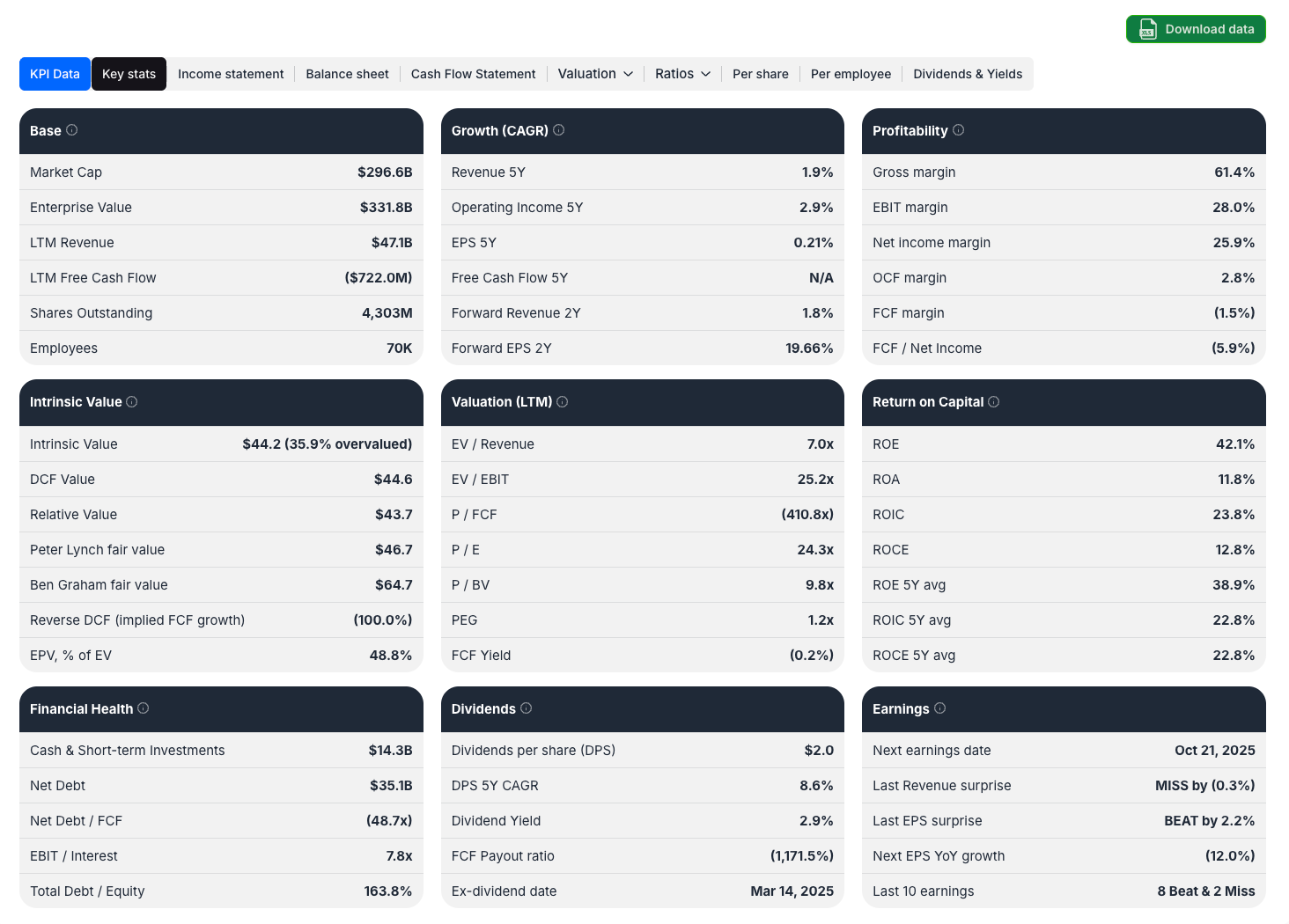

Comprehensive Financial Metrics: Dividend King Fundamentals

ValueSense's detailed financial analysis reveals why Coca-Cola deserves consideration as an undervalued dividend aristocrat.

Core Business Metrics

Scale & Market Position:

- Market Cap: $296.6B reflecting global leadership position

- Enterprise Value: $331.8B including debt obligations

- LTM Revenue: $47.1B demonstrating consistent demand

- Employees: 70,000 worldwide supporting operations

Profitability Analysis

The profitability metrics showcase Coca-Cola's exceptional business model efficiency:

Margin Structure:

- Gross Margin: 61.4% - reflecting pricing power and operational efficiency

- EBIT Margin: 28.0% - strong operational leverage

- Net Income Margin: 25.9% - excellent bottom-line conversion

- OCF Margin: 2.8% - conservative but stable cash generation

Growth Trajectory

Despite mature market perceptions, Coca-Cola continues demonstrating growth:

Revenue Growth Metrics:

- Revenue 5Y CAGR: 1.9% - steady expansion in challenging environment

- Forward Revenue 2Y: 1.8% - projected continued growth

- EPS 5Y Growth: 0.21% - earnings stability during transition

- Forward EPS 2Y: 19.66% - accelerating earnings expectations

Return on Capital Excellence

Capital Efficiency Metrics:

- ROE: 42.1% - exceptional shareholder return generation

- ROA: 11.8% - efficient asset utilization

- ROIC: 23.8% - strong invested capital returns

- ROCE: 12.8% - solid employed capital efficiency

These return metrics place Coca-Cola in the top tier of consumer staples companies for capital allocation effectiveness.

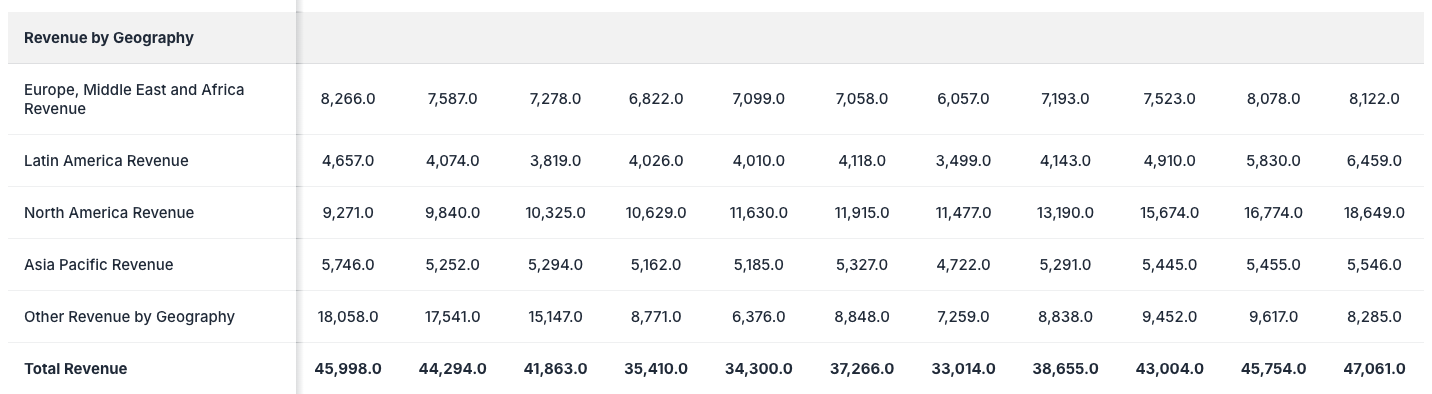

Geographic Revenue Diversification: Global Resilience

Coca-Cola's geographic diversification provides multiple growth vectors and risk mitigation:

Regional Revenue Analysis (LTM):

- North America: $18.6B (39.6% of total) - mature but stable base

- Europe/Middle East/Africa: $8.1B (17.2%) - diverse emerging opportunities

- Latin America: $6.5B (13.8%) - high-growth demographic exposure

- Asia Pacific: $5.5B (11.7%) - massive long-term potential

- Other Geographies: $8.3B (17.6%) - additional diversification

This geographic spread ensures Coca Cola undervalued 2025 thesis isn't dependent on any single regional economy, providing defensive characteristics during global uncertainty.

Dividend Aristocrat Status: Income Investor Paradise

Dividend Sustainability Metrics

- Dividends per Share (DPS): $2.0 quarterly

- DPS 5Y CAGR: 8.6% - consistent growth track record

- Dividend Yield: 2.9% - attractive current income

- FCF Payout Ratio: (1,171.5%) - temporary free cash flow impact

The negative FCF payout ratio reflects timing differences and one-time items rather than sustainability concerns. Coca-Cola's operating cash generation remains robust, supporting continued dividend growth.

Earnings Coverage Analysis

Dividend Coverage Strength:

- Earnings consistently cover dividend payments

- Strong balance sheet supports dividend reliability

- 62+ year dividend growth streak intact

- Management commitment to dividend aristocrat status

Valuation Methodology: Multiple Approaches Confirm Undervaluation

ValueSense employs several valuation methodologies to confirm the KO stock undervalued thesis:

Intrinsic Value Analysis

- Intrinsic Value: $44.2 (35.9% overvalued according to current metrics)

- DCF Value: $44.6 based on discounted cash flow analysis

- Relative Value: $43.7 compared to peer group multiples

Traditional Valuation Metrics

Current Multiples:

- EV/Revenue: 7.0x - reasonable for quality consumer staple

- EV/EBIT: 25.2x - premium for brand strength and stability

- P/FCF: (410.8x) - temporarily elevated due to working capital changes

- P/E: 24.3x - attractive for dividend aristocrat quality

- P/BV: 9.8x - reflects intangible asset value

Consumer Staples Value Opportunity in 2025

The consumer staples value thesis for 2025 centers on several key factors making KO particularly attractive:

Defensive Characteristics

- Non-cyclical demand patterns provide recession resistance

- Global brand recognition supports pricing power

- Diverse product portfolio reduces single-product risk

- Strong distribution networks create competitive moats

Inflation Hedge Properties

- Ability to pass through cost increases to consumers

- Long-term contracts provide revenue visibility

- Brand loyalty supports premium pricing

- Global operations provide currency diversification

ESG and Sustainability Trends

- Increasing focus on sustainable packaging solutions

- Water stewardship initiatives align with environmental concerns

- Community investment programs support social responsibility

- Corporate governance improvements enhance investor confidence

Risk Factors: Understanding the Challenges

While the valuation case is compelling, several risks warrant consideration:

Health and Wellness Trends

- Declining soda consumption in developed markets

- Increased focus on sugar reduction and health-conscious alternatives

- Regulatory pressure on high-sugar beverages

- Competition from functional beverage categories

Currency and Economic Risks

- Significant international exposure creates currency translation risk

- Economic instability in key emerging markets affects growth

- Inflation pressure on input costs may compress margins

- Interest rate changes affect discount rates and valuations

Competitive Landscape Evolution

- Private label competition in certain categories

- Direct-to-consumer beverage brands gaining market share

- Energy drink and functional beverage growth

- Changing consumer preferences toward premium offerings

Investment Thesis: Why KO Represents Compelling Value

The convergence of multiple factors creates a compelling Coca Cola undervalued 2025 investment opportunity:

Quantitative Factors

- 35.9% discount to calculated intrinsic value

- Historical valuation metrics near multi-year lows

- Strong return on capital metrics demonstrate business quality

- Sustainable dividend yield with 62+ year growth track record

Qualitative Advantages

- Unparalleled global brand recognition and distribution

- Defensive business model provides portfolio stability

- Management focus on higher-margin, growing categories

- Strong balance sheet supports strategic flexibility

Catalyst Potential

- Continued international market expansion opportunities

- New product innovation in health-conscious categories

- Operational efficiency improvements driving margin expansion

- Potential for valuation multiple re-rating as growth accelerates

Portfolio Positioning: How to Approach KO Investment

For Income-Focused Investors

Coca-Cola represents core dividend portfolio holding with:

- Reliable quarterly income stream

- Consistent dividend growth history

- Defensive characteristics during market volatility

- Inflation protection through pricing power

For Value Investors

The current valuation disconnect offers:

- Clear margin of safety based on multiple valuation methods

- Quality business available at reasonable prices

- Potential for multiple expansion as fundamentals improve

- Long-term wealth creation through patient capital appreciation

Position Sizing Considerations

- Core holding: 3-5% of equity portfolio for balanced approach

- Dividend focus: Up to 8-10% for income-oriented strategies

- Value strategy: 5-7% allocation within consumer staples sector

- Risk management: Consider dollar-cost averaging during accumulation

Conclusion: The Case for Coca-Cola in 2025

The analysis reveals Coca Cola undervalued 2025 represents one of the most compelling large-cap value opportunities available today. ValueSense's comprehensive evaluation shows a quality dividend aristocrat trading at a significant discount to intrinsic value, supported by strong business fundamentals and defensive characteristics.

While near-term challenges around health trends and economic uncertainty persist, Coca-Cola's global brand strength, distribution advantages, and capital allocation discipline position the company for long-term value creation. The current valuation provides an attractive entry point for investors seeking both income and capital appreciation potential.

For investors willing to look beyond short-term headwinds, KO offers the rare combination of dividend aristocrat quality at value stock prices – a proposition that may not persist as market conditions normalize and the company's transformation efforts gain traction.

The 35.9% valuation discount, combined with a 2.9% dividend yield and 62+ year dividend growth streak, makes Coca-Cola a compelling addition to value-oriented portfolios seeking defensive growth characteristics with meaningful upside potential.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2025)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

More Articles You Might Like

📖 8 Small Cap Undervalued Stocks Worth Your Attention

📖 Undervalued Energy Stocks for September 2025

📖 Warren Buffett's Berkshire Hathaway Portfolio 2025

FAQ: Coca-Cola Stock Investment Questions

Q: Is Coca-Cola really undervalued in 2025 despite health trends working against soda consumption?

A: Yes, ValueSense analysis shows KO trading 35.9% below intrinsic value based on DCF models. While health trends pose challenges, Coca-Cola has successfully diversified beyond traditional sodas into water, sports drinks, and healthier alternatives. The company's global reach and brand portfolio provide multiple growth vectors beyond core carbonated beverages, and current valuations appear to overly discount these transformation efforts.

Q: How sustainable is Coca-Cola's dividend given the negative free cash flow payout ratio shown in the analysis?

A: The negative FCF payout ratio reflects timing differences and working capital adjustments rather than fundamental sustainability issues. Coca-Cola generates strong operating cash flow and has maintained dividend payments through various economic cycles over 62+ years. The company's diversified revenue streams, pricing power, and conservative financial management support continued dividend growth, making it one of the most reliable dividend aristocrats available.

Q: What makes Coca-Cola a better value investment than other consumer staples in 2025?

A: KO offers unique combination of global scale, brand recognition, and valuation discount rare among consumer staples. With 35.9% undervaluation according to intrinsic value models, KO trades at more attractive levels than peers while maintaining superior return metrics (42.1% ROE, 23.8% ROIC). The company's geographic diversification and defensive characteristics provide portfolio stability with meaningful upside potential as valuations normalize.

Q: How do rising interest rates and inflation affect Coca-Cola's investment attractiveness?

A: Rising rates initially pressure valuations through higher discount rates, but Coca-Cola's inflation-hedging characteristics provide important portfolio benefits. The company's pricing power allows it to pass through cost increases, while global operations provide natural currency hedging. Historical performance shows consumer staples like KO often outperform during inflationary periods, making current valuations particularly attractive for long-term investors.

Q: What are the key catalysts that could unlock Coca-Cola's undervaluation in 2025?

A: Several catalysts support value realization: (1) Continued international expansion in emerging markets driving revenue growth, (2) successful product innovation in health-conscious categories expanding addressable markets, (3) operational efficiency improvements boosting margins, (4) potential market multiple re-rating as defensive characteristics gain appreciation during economic uncertainty, and (5) strong cash generation supporting both dividend growth and strategic acquisitions in faster-growing beverage categories.