Disney vs Netflix Stock Analysis 2025: The Ultimate Streaming Giants Showdown

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

The streaming wars have fundamentally reshaped the entertainment landscape, but for investors, the key question remains: which streaming stock offers better value in 2025? In a comprehensive analysis comparing Disney (DIS) vs Netflix (NFLX), we dive deep into the financial metrics, competitive positioning, and investment thesis for both media giants.

This detailed comparison reveals a classic "quality vs. value" investment scenario that every investor should understand. While Netflix has emerged as the streaming leader with superior profitability metrics, Disney trades at compelling valuations that suggest the market may be overly pessimistic about its turnaround prospects.

Watch Our Complete Video Analysis

Before diving into the detailed breakdown, watch our comprehensive video analysis where we examine every aspect of the Disney vs Netflix investment decision:

🎥 Watch: Disney vs Netflix - Complete Stock Analysis & Valuation Comparison

Executive Summary: Netflix Quality vs Disney Value

Our analysis using ValueSense analytics reveals two distinct investment opportunities:

Netflix (NFLX): The Quality Premium Play

- Superior profitability with 20.4% FCF margin vs Disney's 12.2%

- Exceptional capital efficiency: 39.8% ROIC vs Disney's 14.7%

- Strong revenue growth acceleration to 14.8% vs Disney's 5.0%

- Challenge: Expensive valuation requiring 21.4% FCF growth for 10 years

Disney (DIS): The Contrarian Value Opportunity

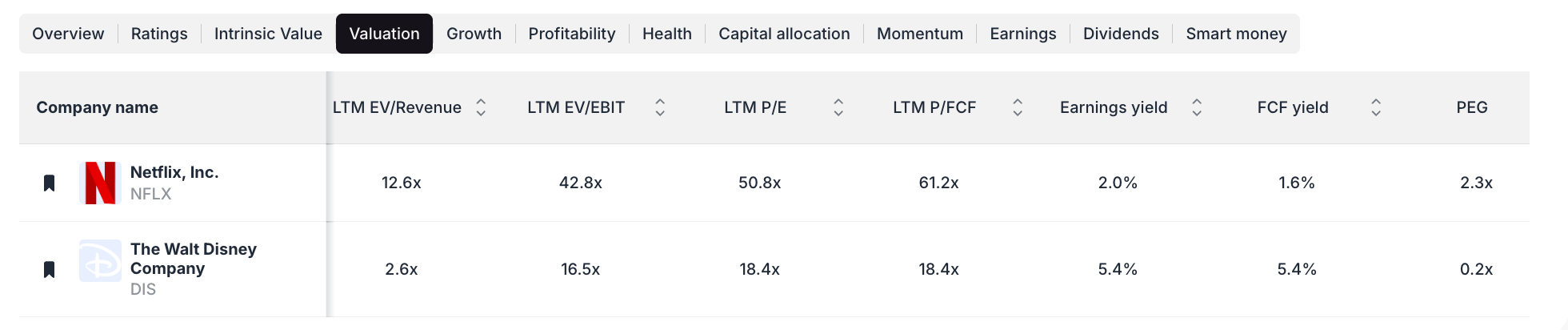

- Attractive valuation: 18x P/E vs Netflix's 50.8x P/E

- Strong FCF yield of 5.6% vs Netflix's 1.6%

- Diversified business model with profitable theme parks

- Opportunity: Market expects only 4.8% FCF growth - low hurdle to beat

Key Financial Metrics: Netflix Pulls Ahead

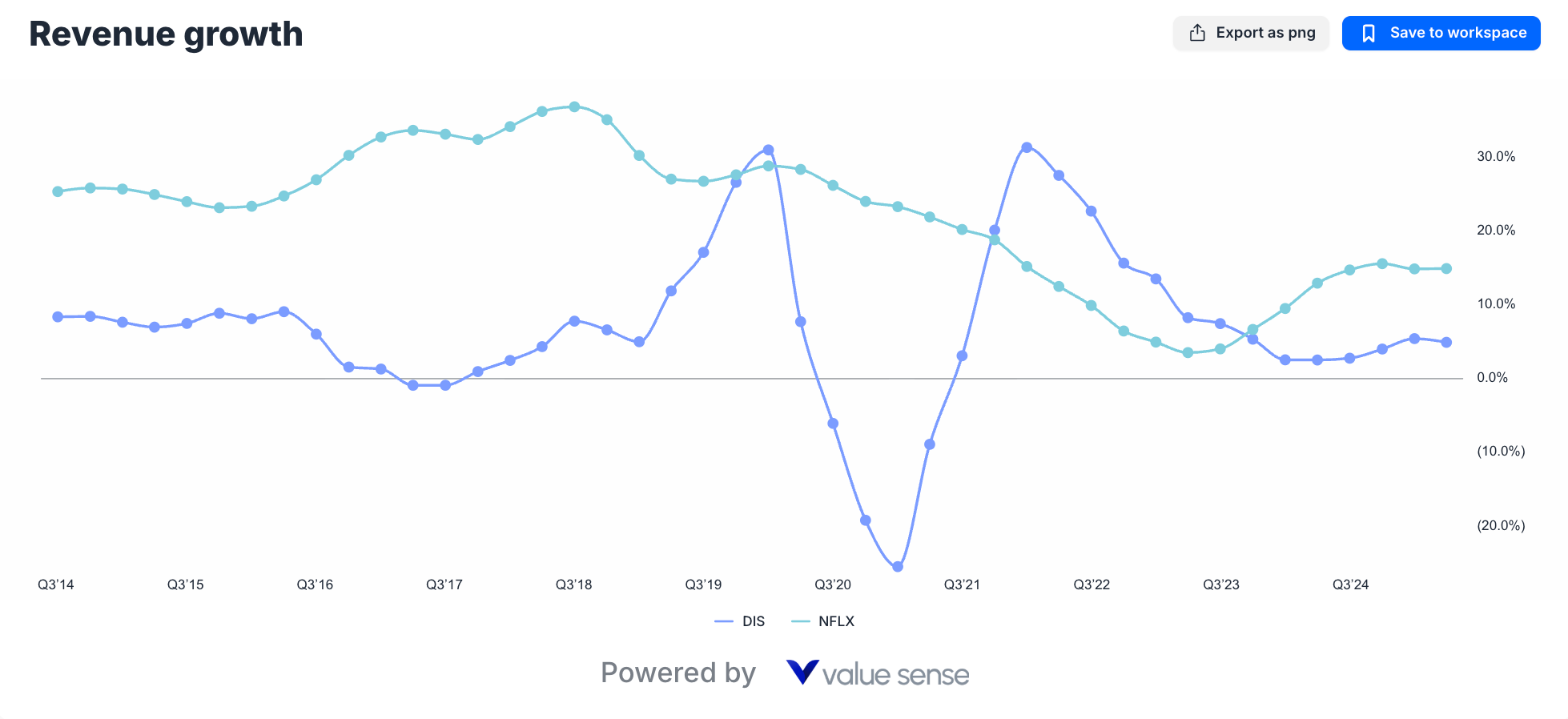

Revenue Growth Acceleration

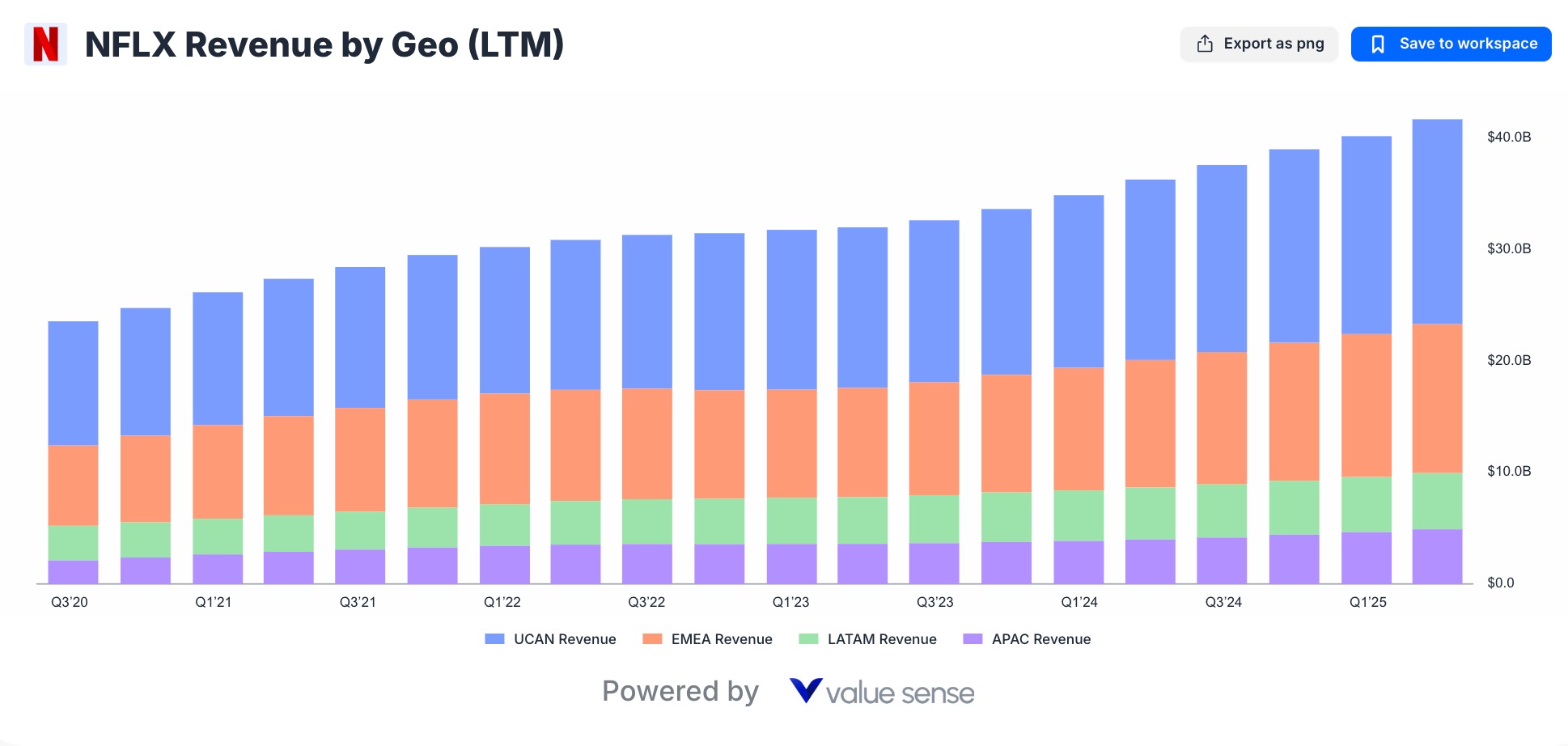

The revenue growth comparison reveals Netflix's dramatic reacceleration following its 2022 subscriber slowdown:

- Current Growth: 14.8% year-over-year (LTM)

- Growth Driver: International expansion in EMEA and APAC regions

- Trajectory: Nearly triple Disney's growth rate

- Outlook: Continued international subscriber acquisition

- Current Growth: 5.0% year-over-year (LTM)

- Growth Pattern: "Flattish" overall performance across segments

- Key Challenge: Streaming segment losses offsetting Parks strength

- Recovery Thesis: Streaming profitability turnaround potential

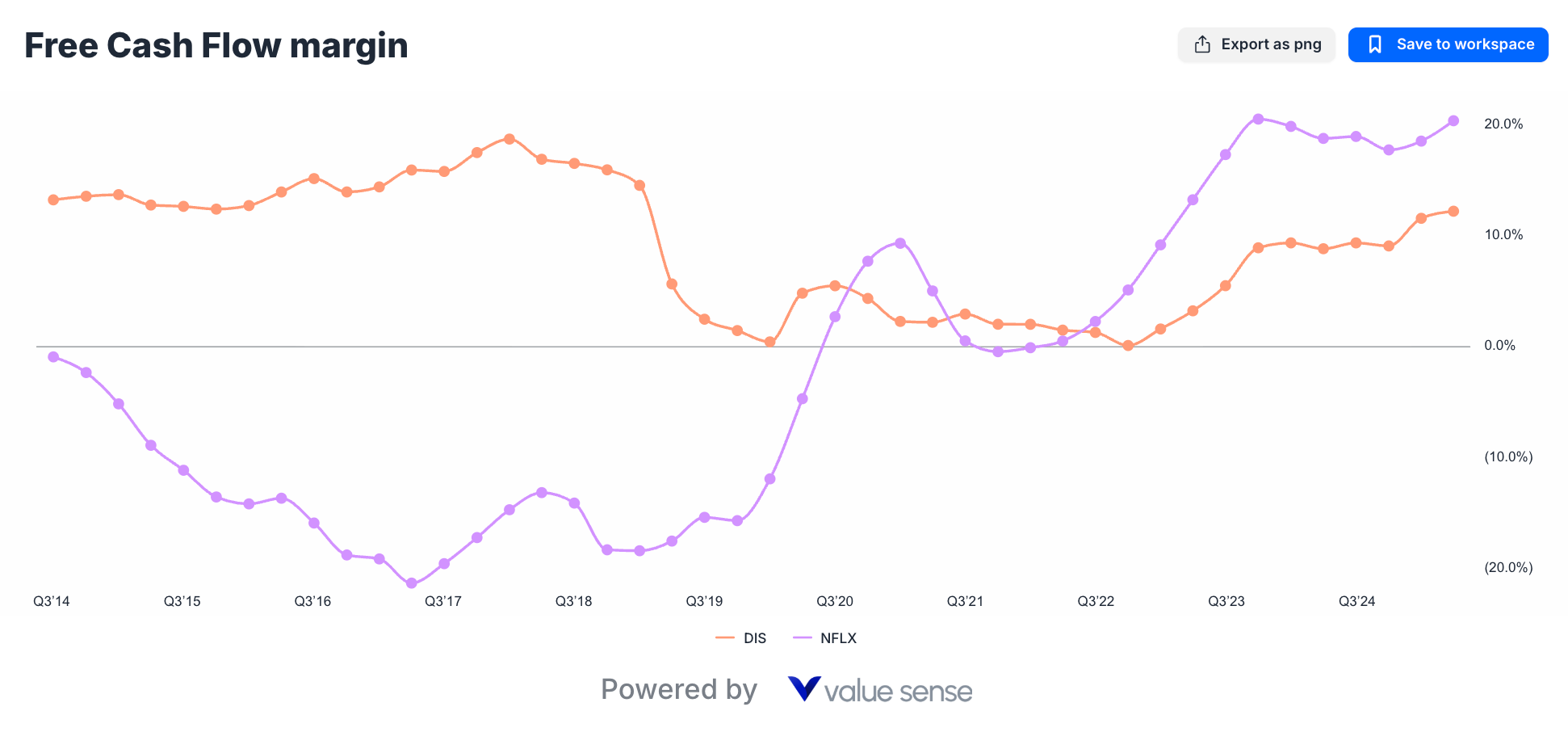

Free Cash Flow Margin Expansion

Netflix's transformation from cash-burning growth company to profitable streaming leader shows dramatically in FCF metrics:

- Current Margin: 20.4% - industry-leading performance

- Historical Context: Massive improvement from content spending peak

- Driver: Winning streaming wars allows reduced content capex

- Sustainability: Operating leverage from subscriber scale

- Current Margin: 12.2% - solid but declining

- Historical Strength: Previously more consistent FCF generator

- Challenge: Streaming investments pressuring margins

- Diversification Benefit: Parks cash flow supports streaming losses

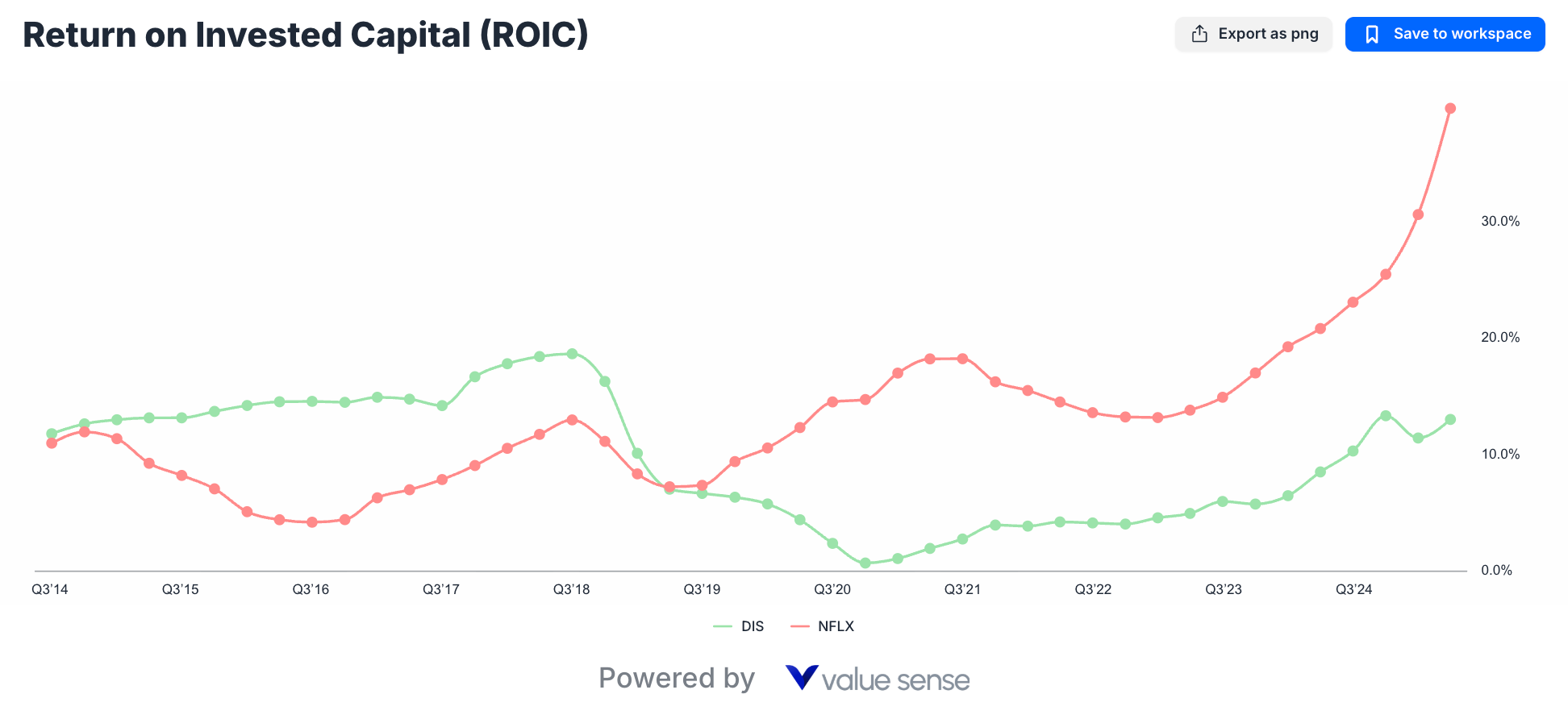

Return on Invested Capital Excellence

Perhaps no metric better illustrates Netflix's operational superiority than ROIC performance:

- Current ROIC: 39.8% - exceptional capital allocation

- Trend: Sharply rising as content investments scale

- Implication: Every dollar invested generates significant returns

- Competitive Advantage: Scale economics in content acquisition

- Current ROIC: 14.7% - reasonable but lagging

- Stability: More consistent but lower absolute returns

- Challenge: Heavy capital requirements across multiple businesses

- Opportunity: Potential improvement if streaming reaches profitability

Business Model Analysis: Diversification vs Focus

Netflix: Pure-Play Streaming Dominance

Netflix's focused strategy has created the world's most successful streaming platform:

Competitive Advantages:

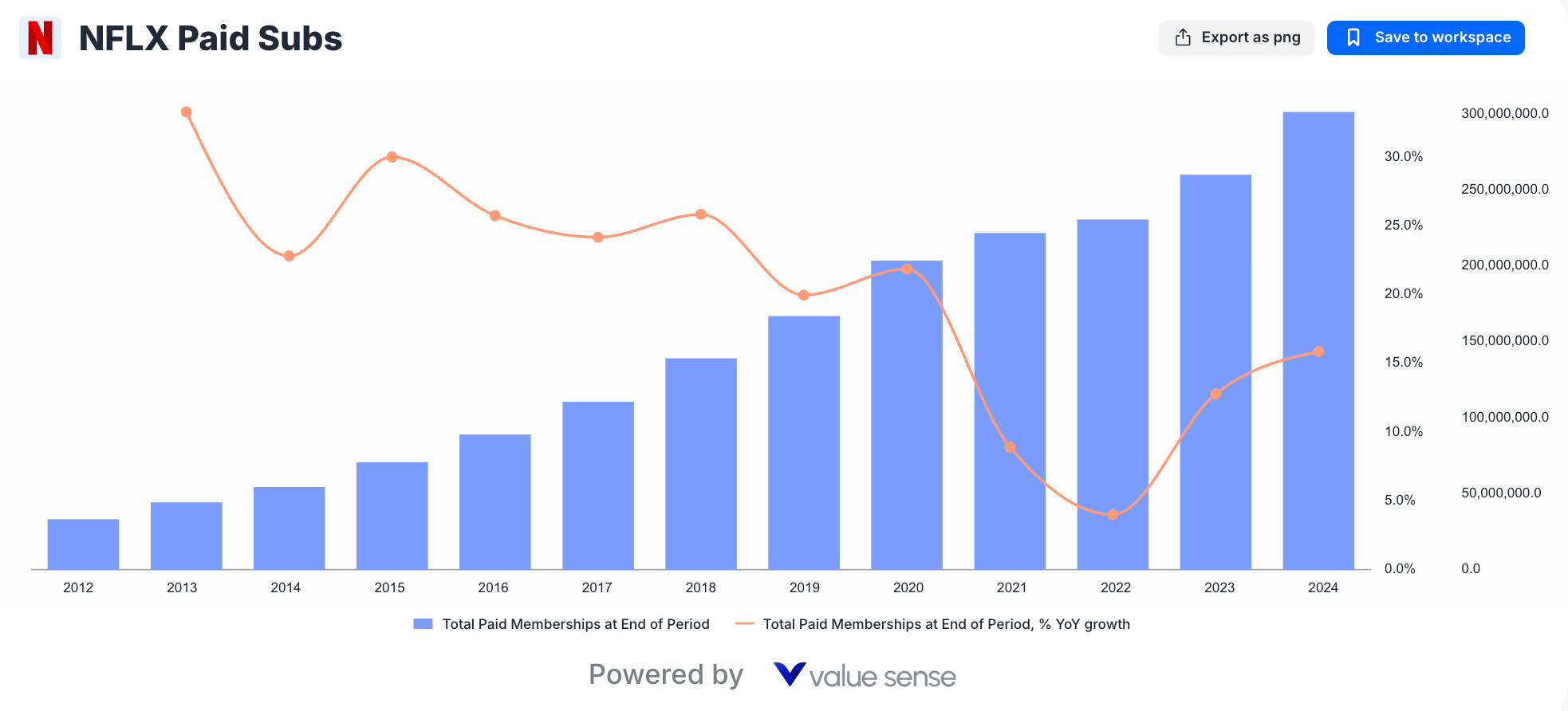

- Global Scale: 260+ million subscribers worldwide

- Content Library: Vast catalog spanning all genres and languages

- Technology Platform: Superior streaming experience and recommendations

- Brand Recognition: Synonymous with streaming entertainment

- Operating Leverage: Fixed content costs spread across growing subscriber base

Growth Strategy:

- International Expansion: Major opportunity in EMEA and APAC

- Content Optimization: Data-driven content creation and acquisition

- Pricing Power: Premium pricing in mature markets

- Adjacent Opportunities: Gaming, live events, advertising tiers

Disney: Diversified Entertainment Conglomerate

Disney's diversified model provides stability but complexity:

Business Segment Breakdown:

- Entertainment (60% of revenue): Streaming, linear networks, content sales

- Sports (15% of revenue): ESPN and sports content

- Experiences (25% of revenue): Theme parks, resorts, cruise lines

Competitive Advantages:

- Unparalleled IP: Marvel, Star Wars, Disney classics, Pixar

- Multiple Revenue Streams: Parks subsidize streaming investments

- Brand Loyalty: Multi-generational emotional connections

- Global Footprint: Theme parks and content worldwide

- Defensive Characteristics: Non-cyclical entertainment demand

Turnaround Challenges:

- Streaming Profitability: DTC segment burning cash

- Linear Decline: Traditional TV revenues falling

- Capital Intensity: Multiple businesses require significant investment

Valuation Analysis: Value vs Growth Premium

Traditional Valuation Metrics

The valuation gap between Disney and Netflix reflects their different market positioning:

- P/E Ratio: 50.8x - growth stock premium

- FCF Yield: 1.6% - expensive relative to cash generation

- Justification: Superior growth and profitability metrics

- Risk: High expectations with little margin for error

- P/E Ratio: 18x - value stock discount

- FCF Yield: 5.6% - attractive cash yield for patient investors

- Opportunity: Potential rerating if turnaround succeeds

- Safety: Low expectations provide downside protection

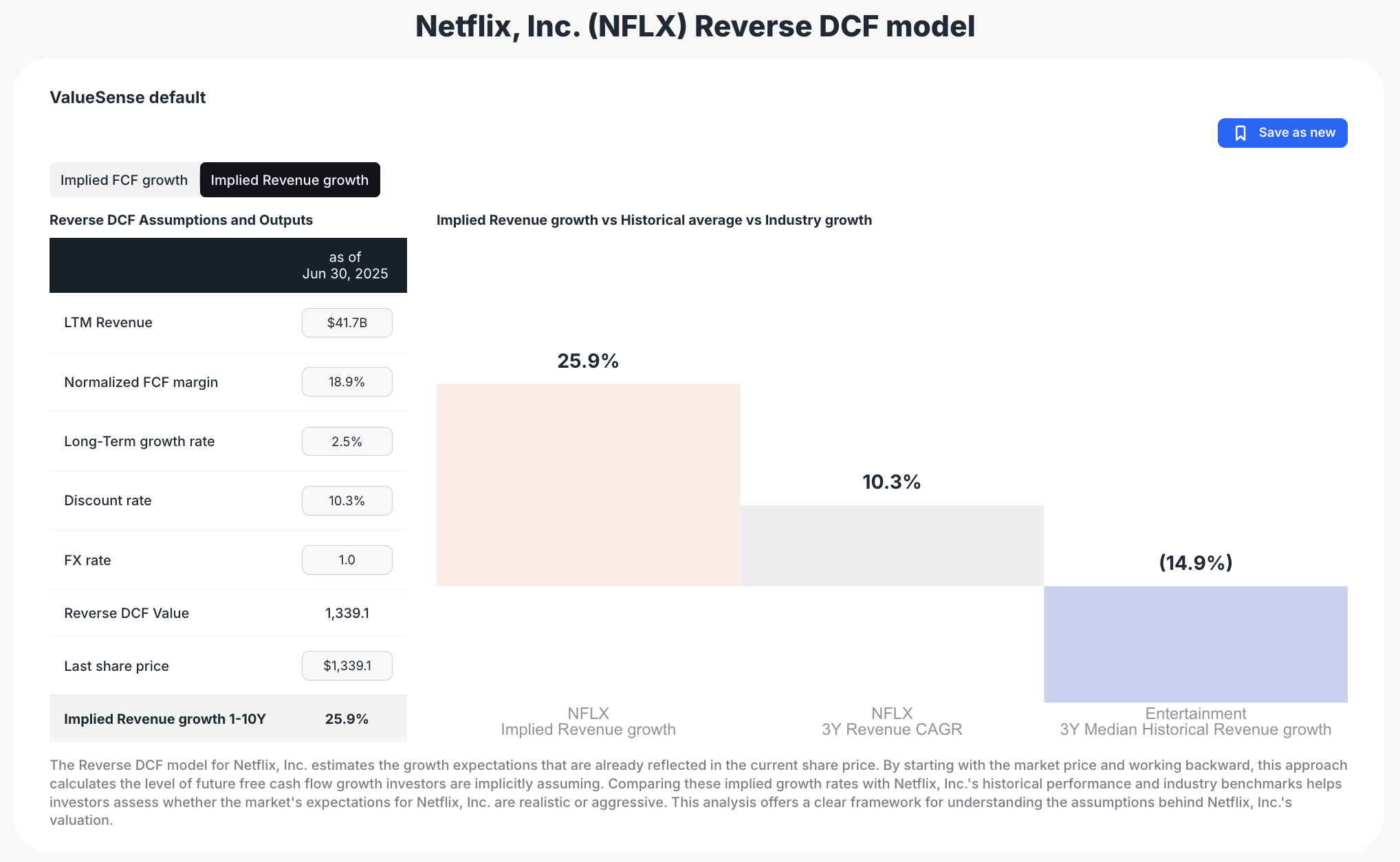

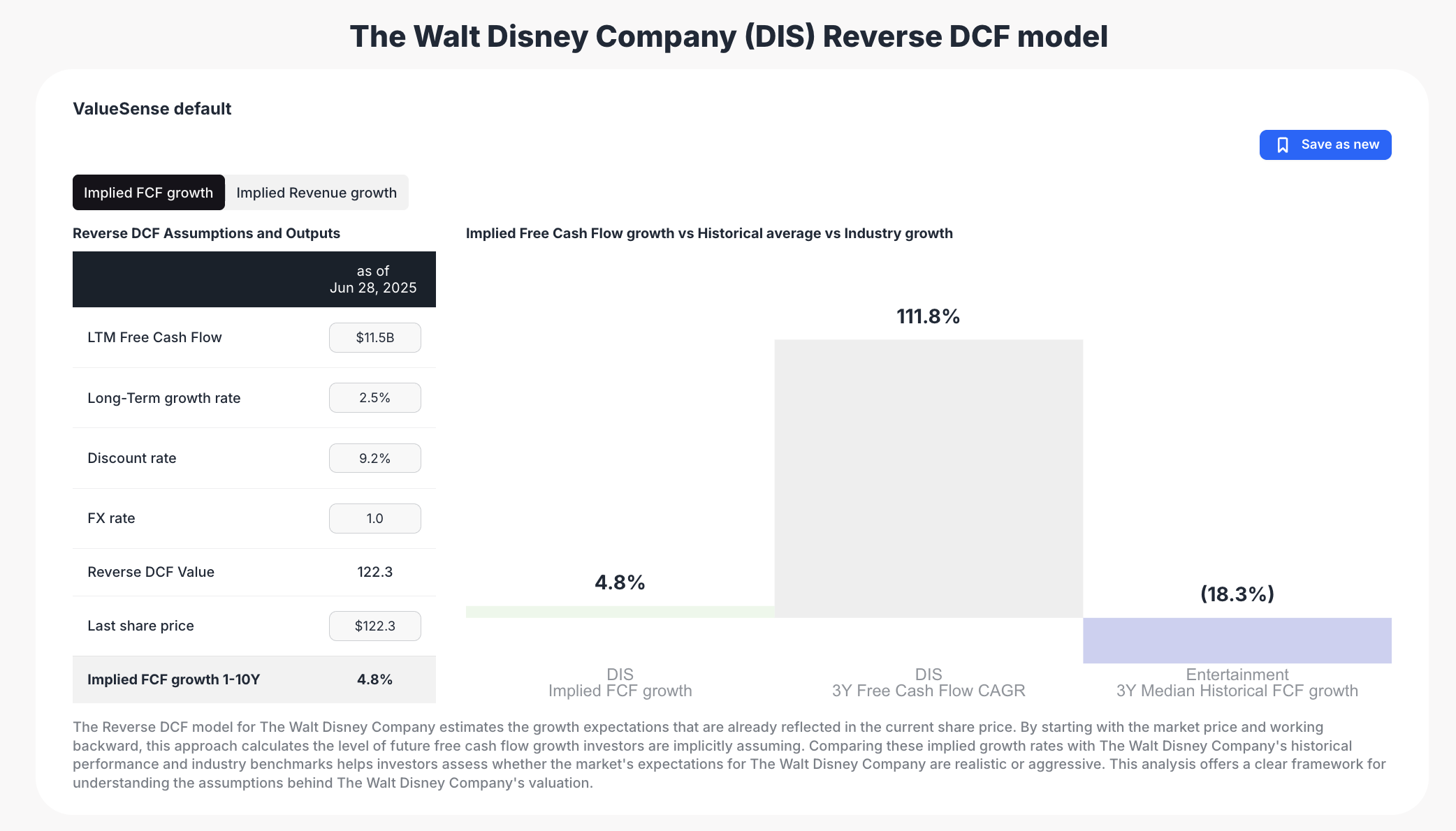

Reverse DCF Analysis: Market Expectations

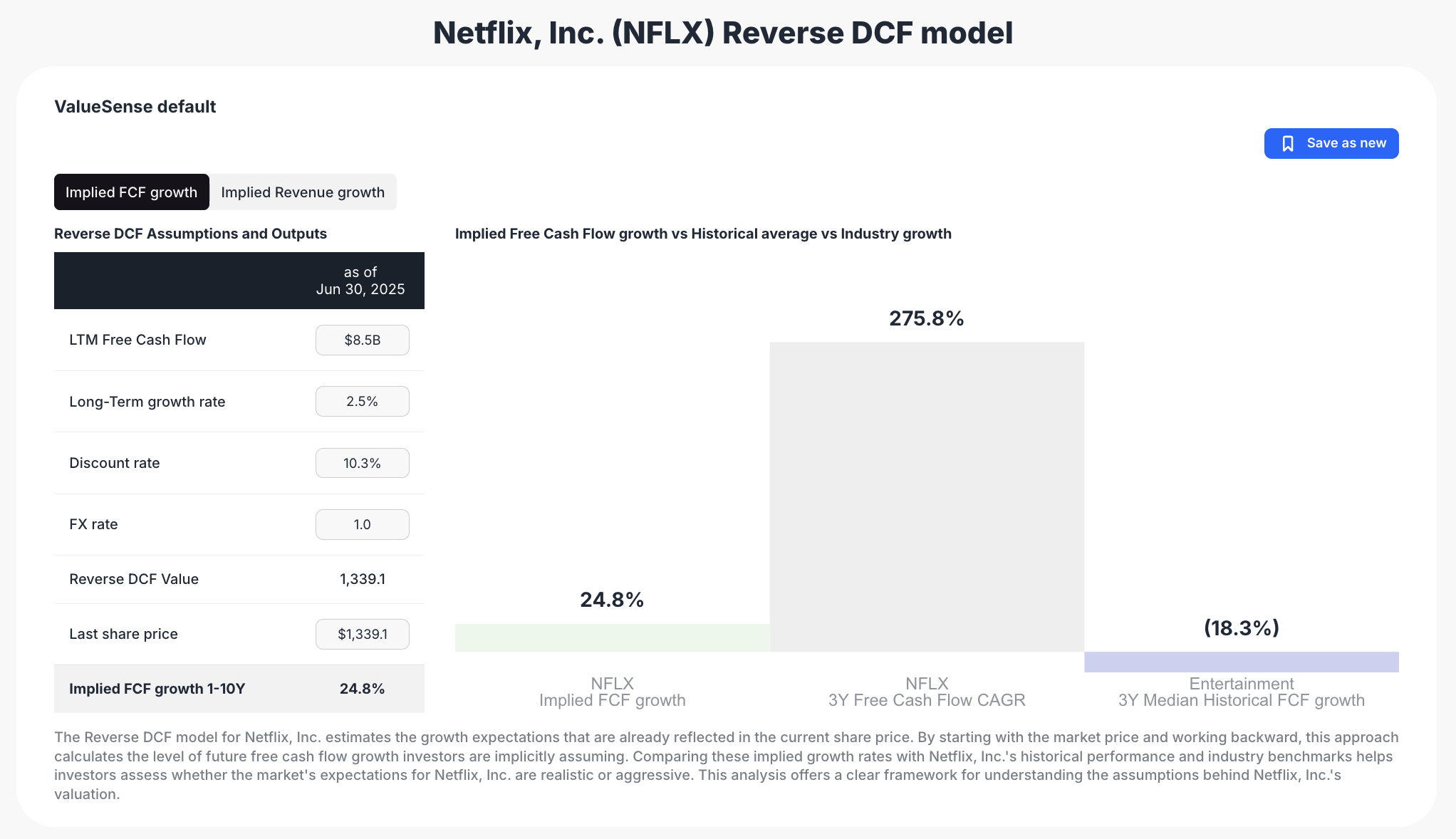

Our reverse discounted cash flow analysis reveals what the market expects from each company:

Netflix Implied Expectations:

- FCF Growth Required: 24.8% annually for 10 years

- Revenue Growth Needed: 25.9%

- Assessment: Extremely aggressive assumptions

- Risk: Little room for disappointment

Disney Implied Expectations:

- FCF Growth Required: Only 4.8% annually for 10 years

- Assessment: Very achievable hurdle rate

- Opportunity: Any positive catalysts could drive significant outperformance

- Margin of Safety: Low expectations provide investment cushion

Investment Thesis: Two Distinct Opportunities

The Netflix Quality Play

Investment Rationale: Netflix represents a best-in-class, high-quality growth company that has definitively won the streaming wars. The investment thesis centers on:

Strengths:

- Market Leadership: Dominant global streaming position

- Superior Metrics: Industry-leading profitability and capital efficiency

- Growth Runway: Significant international expansion opportunity

- Execution Track Record: Proven ability to scale and improve margins

Required Beliefs:

- Streaming market will continue expanding globally

- Netflix can maintain competitive advantages against tech giants

- International markets will achieve similar profitability as mature regions

- Content spending can remain disciplined while driving growth

Risk Factors:

- Valuation Risk: Stock priced for near-perfect execution

- Competition: Amazon, Apple, Google have deeper pockets

- Content Costs: Arms race could pressure margins

- Market Saturation: Limited room for error in mature markets

The Disney Contrarian Value Play

Investment Rationale: Disney represents a classic contrarian opportunity where market pessimism has created attractive entry valuations for a high-quality business with multiple turnaround catalysts.

Strengths:

- Attractive Valuation: Trading below historical multiples

- Diversified Cash Flow: Parks provide stability during streaming transition

- Unmatched IP: Content library that competitors cannot replicate

- Turnaround Optionality: Multiple paths to improve profitability

Required Beliefs:

- Streaming segment can achieve profitability within 2-3 years

- Theme parks will maintain strong performance despite economic cycles

- Linear TV decline will stabilize at manageable levels

- Management can successfully execute turnaround strategy

Risk Factors:

- Execution Risk: Turnaround more difficult than anticipated

- Secular Decline: Linear TV revenues may fall faster than expected

- Economic Sensitivity: Parks vulnerable to recession

- Streaming Competition: May require higher content spending than planned

Sector Trends and Catalysts

Streaming Industry Dynamics

Market Maturity Patterns:

- Mature Markets: UCAN showing subscriber saturation

- Growth Markets: EMEA and APAC driving industry expansion

- Revenue Evolution: ARPU growth replacing subscriber growth in mature regions

- Profitability Focus: Industry shift from growth-at-all-costs to sustainable margins

Competitive Landscape:

- Netflix Advantages: First-mover scale and international penetration

- Disney Differentiators: Premium IP and family-friendly positioning

- Big Tech Threat: Amazon, Apple, Google using streaming for ecosystem benefits

- Consolidation Pressure: Smaller players struggling with content costs

Key Catalysts to Watch

Netflix Catalysts:

- International Expansion: Subscriber growth in underpenetrated markets

- ARPU Growth: Price increases in established markets

- Advertising Tier: Revenue diversification through ad-supported plans

- Content Efficiency: Higher engagement per dollar spent on content

Disney Catalysts:

- Streaming Profitability: DTC segment reaching break-even

- Cost Management: Successful cost reduction across linear networks

- Parks Performance: Continued strength in experiences segment

- Content Pipeline: Marvel and Star Wars driving subscriber engagement

Technical Analysis and Market Performance

Historical Performance Context

Netflix Stock Performance:

- 2022 Crash: Stock fell over 70% from peaks on subscriber concerns

- 2023-2024 Recovery: Strong rebound as fundamentals improved

- Current Level: Back to premium valuations reflecting quality recognition

- Volatility: High beta stock sensitive to growth expectations

Disney Stock Performance:

- 10-Year Return: Only 28% total return over decade

- Recent Performance: Trading significantly below 2021 highs

- Value Territory: Multiple consecutive years of underperformance

- Contrarian Setup: Negative sentiment creating opportunity

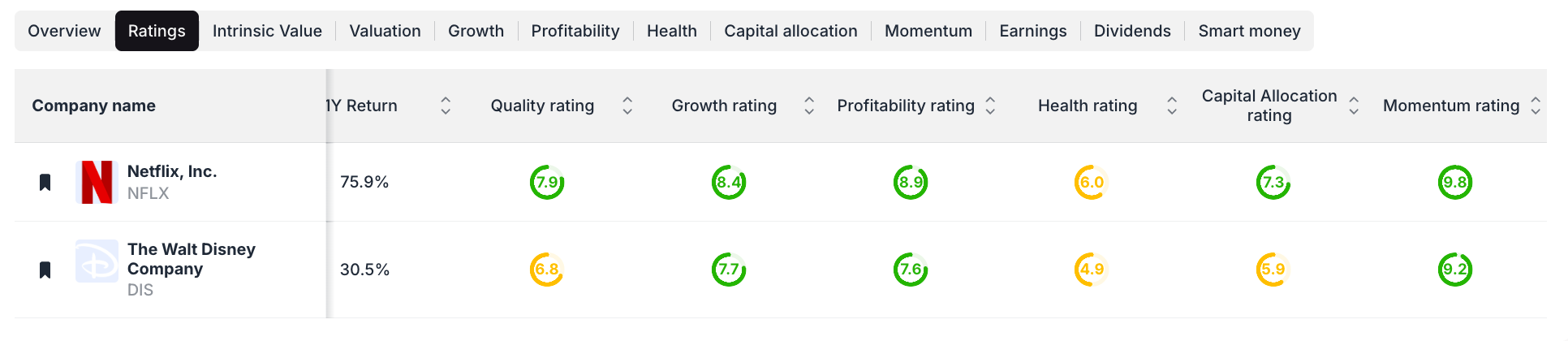

Quality Ratings Comparison

ValueSense proprietary quality analysis:

- Netflix Quality Score: 7.9/10 - reflecting superior operational metrics

- Disney Quality Score: 6.9/10 - solid but facing execution challenges

- Gap Analysis: Netflix's quality premium justified by financial performance

Risk Assessment and Portfolio Considerations

Netflix Investment Risks

Valuation Risk:

- Current stock price assumes flawless execution for decade

- Any growth disappointment could trigger significant correction

- Multiple compression risk if growth slows

Competitive Risk:

- Tech giants have unlimited content budgets

- Market fragmentation reducing pricing power

- International expansion facing local competition

Operational Risk:

- Content hit/miss ratio affecting subscriber retention

- Currency headwinds from international operations

- Regulatory risk in various global markets

Disney Investment Risks

Execution Risk:

- Streaming turnaround more complex than anticipated

- Cost cutting may damage content quality

- Management transition uncertainty

Secular Risk:

- Linear TV decline accelerating beyond expectations

- Theme park sensitivity to economic downturns

- Changing consumer entertainment preferences

Financial Risk:

- High debt levels limiting strategic flexibility

- Capital allocation between streaming and traditional businesses

- Dividend sustainability during transition period

Portfolio Allocation Strategy

Netflix Position Sizing

Growth Portfolio Allocation: 3-5%

- Suitable for investors seeking exposure to streaming leadership

- Position size reflects high valuation and execution risk

- Consider dollar-cost averaging given volatility

Quality Growth Strategy: 5-8%

- Appropriate for investors prioritizing business quality over valuation

- Larger allocation justified by superior operational metrics

- Long-term holding period reduces timing risk

Disney Position Sizing

Value Portfolio Allocation: 4-7%

- Core position for contrarian value investors

- Attractive risk-reward given low expectations

- Diversification benefits from different business model

Dividend Growth Strategy: 3-5%

- Moderate allocation given dividend sustainability questions

- Focus on total return rather than current yield

- Monitor streaming profitability progress

Conclusion: Two Valid Investment Approaches

The Disney vs Netflix analysis reveals two legitimate but different investment opportunities that suit different investor profiles and market outlooks.

Choose Netflix If:

- You believe in paying premium prices for exceptional quality

- International streaming expansion will drive sustained growth

- Superior management execution justifies valuation premium

- Your portfolio can handle high-beta growth exposure

Choose Disney If:

- You prefer contrarian value opportunities with multiple catalysts

- Diversified business models appeal to your risk tolerance

- Low market expectations provide attractive risk-reward setup

- You believe streaming turnaround is achievable within 2-3 years

The Verdict: Both stocks offer compelling investment cases, but for different reasons. Netflix represents quality growth at a premium price, while Disney offers potential value recovery at discounted valuations. The optimal choice depends on your investment style, risk tolerance, and conviction about each company's execution capabilities.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2025)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

More Articles You Might Like

📖 AltaRock Portfolio 2025: The Mark Massey's Latest Moves

📖 Undervalued Healthcare Stocks August 2025

📖 Coca-Cola Stock Analysis

FAQ: Disney vs Netflix Investment Decision

Q: Which stock is better for long-term investors - Disney or Netflix?

A: Both offer long-term value but for different reasons. Netflix provides exposure to the winning streaming platform with superior profitability metrics, while Disney offers a contrarian value opportunity with multiple turnaround catalysts. Netflix suits growth investors willing to pay premium valuations, while Disney appeals to value investors seeking recovery plays with diversified business models.

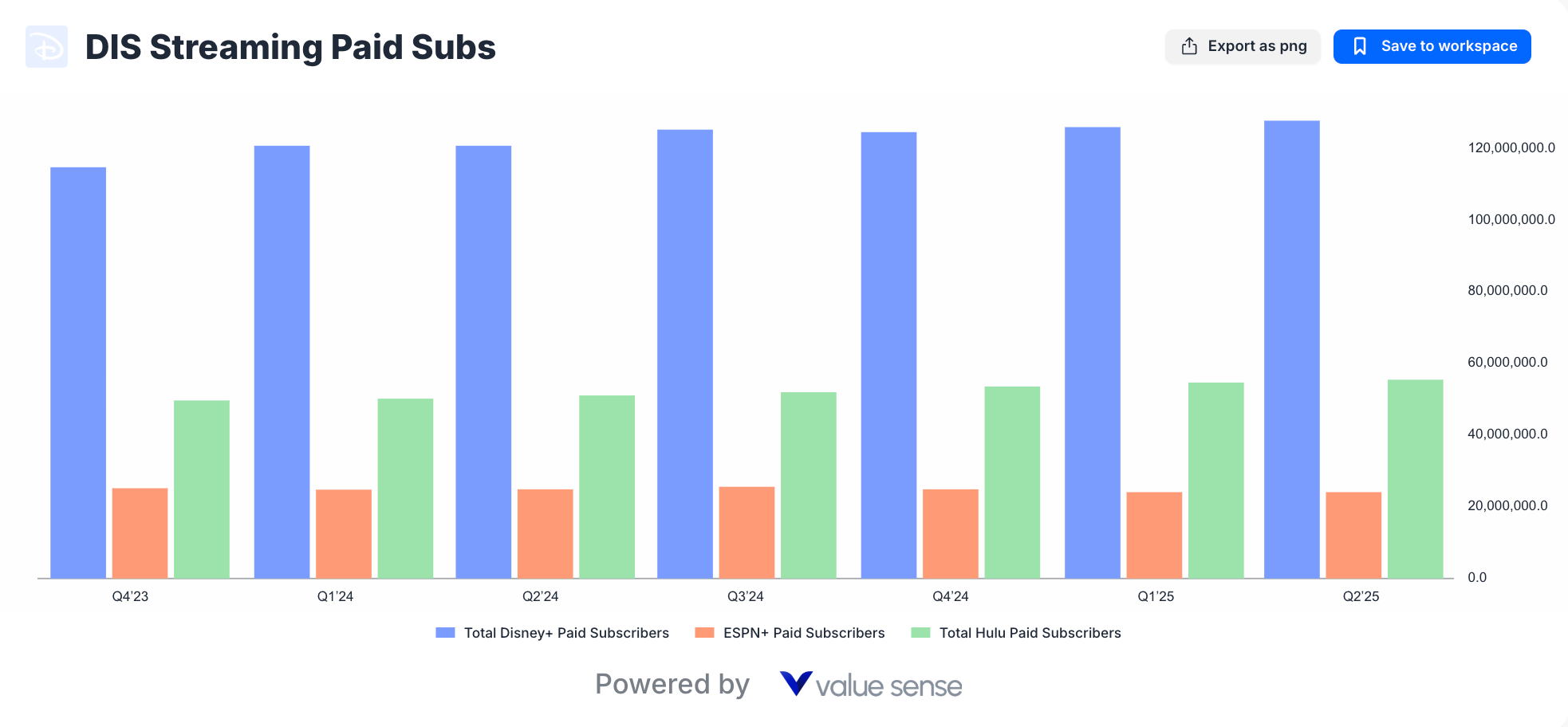

Q: How do the streaming subscriber metrics compare between Disney and Netflix?

A: Netflix shows strong subscriber growth acceleration driven by international markets (EMEA and APAC), while Disney's streaming subscriber growth has stagnated across its services. Netflix's global scale advantage is evident with 260+ million subscribers, compared to Disney's challenged Disney+ growth trajectory requiring renewed focus on content and market expansion.

Q: What are the biggest risks for each stock in 2025?

A: Netflix's primary risk is valuation - the stock requires 21.4% annual FCF growth for 10 years to justify current prices, leaving little room for execution errors. Disney faces execution risk in turning around its streaming business while managing linear TV decline and maintaining theme park performance during potential economic weakness.

Q: How do the dividend prospects compare between Disney and Netflix?

A: Netflix doesn't pay dividends, focusing on reinvestment and share buybacks. Disney maintains a dividend but sustainability depends on streaming profitability progress and overall cash flow improvement. Disney's 5.6% FCF yield suggests better current income potential, while Netflix offers pure capital appreciation opportunity.

Q: Which stock performs better during different market conditions?

A: Netflix typically outperforms during growth-favorable markets due to its premium business model and international expansion story. Disney may outperform during value rotations or economic uncertainty due to its defensive characteristics, diversified revenue streams, and attractive valuation providing downside protection during market stress.