Ensemble Capital Management Portfolio in 2026: Top Holdings & Recent Changes

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

Ensemble Capital Management continues to exemplify disciplined, long-term value investing through precise portfolio management. Their Q3 2024 $1.18B portfolio shows a pattern of significant reductions across top holdings, signaling a strategic rebalancing amid market highs while maintaining intense concentration in high-quality businesses.

Portfolio Overview: Concentration with Calculated Discipline

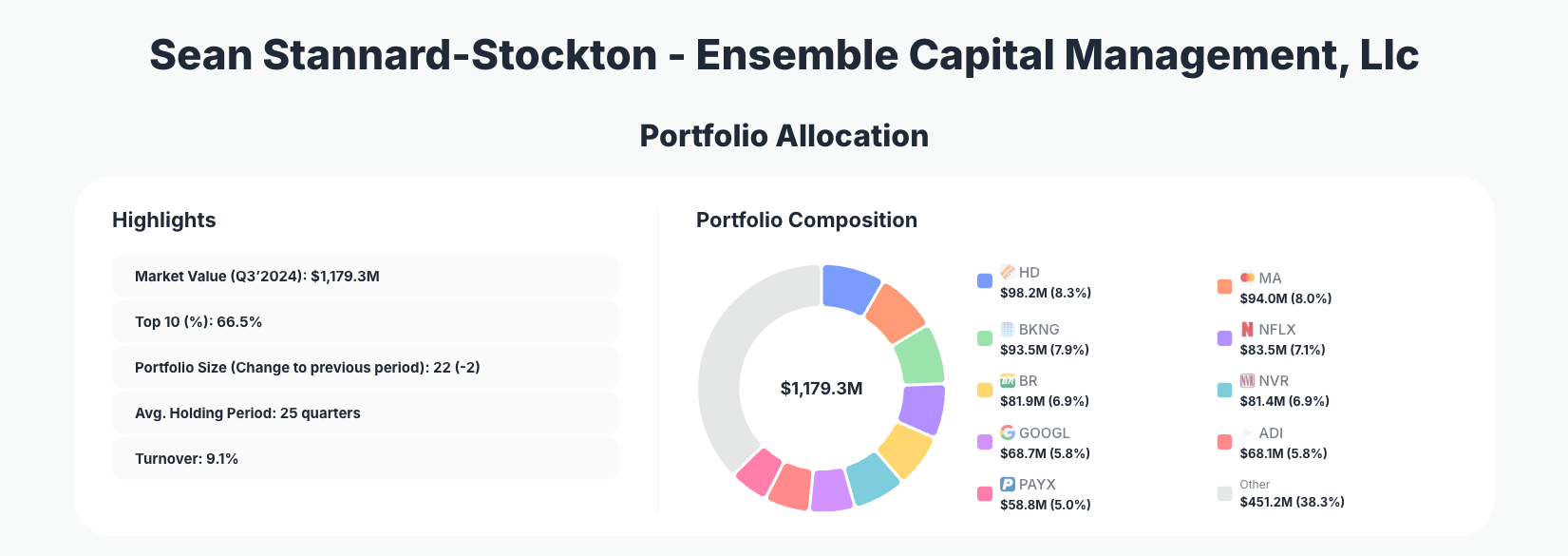

Portfolio Highlights (Q3’2024): - Market Value: $1,179.3M - Top 10 Holdings: 66.5% - Portfolio Size: 22 -2 - Average Holding Period: 25 quarters - Turnover: 9.1%

Ensemble Capital Management's portfolio remains a textbook example of concentrated investing, with the top 10 holdings commanding 66.5% of the $1.18 billion total. This level of focus underscores their philosophy of owning a small number of deeply researched, high-quality companies rather than diversifying broadly. The reduction in portfolio size to 22 positions (-2 from prior quarter) further emphasizes selectivity, trimming underperformers or overweights to maintain conviction-driven allocations.

The average holding period of 25 quarters—over six years—highlights patience as a core tenet, aligning with their low 9.1% turnover rate. This isn't passive indexing; it's active stewardship of positions where they see durable competitive advantages. Accessing their full portfolio details on ValueSense reveals how these metrics have evolved, providing retail investors with institutional-grade transparency from 13F filings.

In a market environment of elevated valuations, this quarter's moves suggest prudent risk management without abandoning their core strategy. The firm's approach prioritizes businesses with strong moats, predictable cash flows, and management alignment, making their portfolio a compelling study for value-oriented investors.

Top Holdings: Widespread Reductions Across Quality Leaders

Ensemble Capital's top positions feature consistent trims across consumer, financial, tech, and industrial leaders, reflecting a portfolio-wide reallocation. Leading the pack is The Home Depot at 8.3% $98.2M, reduced by 17.51%, followed closely by Mastercard (8.0%, $94.0M, Reduce 13.97%) and Booking Holdings (7.9%, $93.5M, Reduce 17.85%). These reductions in stalwart growth names indicate profit-taking after strong runs.

Further down, Netflix holds 7.1% ($83.5M, Reduce 11.62%), while Broadridge Financial (6.9%, $81.9M, Reduce 14.35%) and NVR (6.9%, $81.4M, Reduce 24.27%) saw notable cuts—the largest among top holdings. Alphabet (5.8%, $68.7M, Reduce 16.89%) and Analog Devices (5.8%, $68.1M, Reduce 7.58%) continue to reflect tech exposure, with trims suggesting valuation discipline.

Rounding out the top 10, Paychex (5.0%, $58.8M, Reduce 17.78%) and Ferrari (4.8%, $56.2M, Reduce 15.31%) maintain meaningful stakes despite reductions. These 10 positions alone represent two-thirds of the portfolio, blending cyclical consumer plays like Home Depot and NVR with resilient fintech (Mastercard, Paychex, Broadridge) and digital leaders (Netflix, Booking, Alphabet). The uniform trimming pattern across all top holdings points to a deliberate de-risking, potentially freeing capital for new opportunities outside the top tier.

What the Portfolio Reveals

Ensemble Capital's Q3 moves paint a picture of disciplined quality investing amid frothy markets. Key themes emerge:

- Quality Over Speculation: Holdings like Mastercard, Netflix, and Alphabet emphasize durable moats—network effects, content dominance, and scale—over fleeting growth stories. Reductions suggest they're locking in gains when valuations stretch.

- Sector Focus on Resilient Growth: Heavy tilt toward consumer discretionary (Home Depot, Booking, Ferrari, NVR at ~28% combined), fintech/services (Mastercard, Broadridge, Paychex ~20%), and tech (Netflix, Alphabet, Analog Devices ~19%). Minimal exposure to volatile cyclicals or commodities.

- Risk Management via Trimming: Average reduction of ~15% across top 10 signals proactive position sizing, avoiding overconcentration in winners. Low turnover 9.1% balances activity with patience.

- Long-Term Horizon: 25-quarter average hold reinforces buy-and-hold for compounding machines, not trading.

This strategy prioritizes businesses with predictable earnings power, aligning with Ensemble's focus on "investing at a reasonable price in exceptional companies."

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Portfolio Concentration Analysis

| Position | Value | % of Portfolio | Recent Change |

|---|---|---|---|

| The Home Depot, Inc. (HD) | $98.2M | 8.3% | Reduce 17.51% |

| Mastercard Incorporated (MA) | $94.0M | 8.0% | Reduce 13.97% |

| Booking Holdings Inc. (BKNG) | $93.5M | 7.9% | Reduce 17.85% |

| Netflix, Inc. (NFLX) | $83.5M | 7.1% | Reduce 11.62% |

| Broadridge Financial Solutions, Inc. (BR) | $81.9M | 6.9% | Reduce 14.35% |

| NVR, Inc. (NVR) | $81.4M | 6.9% | Reduce 24.27% |

| Alphabet Inc. (GOOGL) | $68.7M | 5.8% | Reduce 16.89% |

| Analog Devices, Inc. (ADI) | $68.1M | 5.8% | Reduce 7.58% |

| Paychex, Inc. (PAYX) | $58.8M | 5.0% | Reduce 17.78% |

| Ferrari N.V. (RACE) | $56.2M | 4.8% | Reduce 15.31% |

This table underscores Ensemble Capital's high-conviction model, with the top 10 averaging 6.65% per position and no single holding exceeding 8.3%. The portfolio shrank to 22 names -2, amplifying concentration risk but also potential upside from conviction bets. Uniform reductions—ranging from 7.58% (ADI) to 24.27% (NVR)—totaling over 150% in aggregate cuts, likely generated cash for redeployment. This isn't panic selling; it's sophisticated rebalancing, maintaining quality while addressing valuation gaps. Investors tracking via ValueSense can see how this positions them for volatility.

Investment Lessons from Ensemble Capital Management

Ensemble's Q3 13F filing distills timeless principles for patient investors:

- Trim Winners Ruthlessly: Even top performers like NVR -24% and Home Depot -17.51% get cut when valuations demand it—discipline over attachment.

- Concentrate in Moats: 66.5% in 10 names proves understanding trumps diversification; own what you know deeply.

- Long Holding Periods Pay: 25 quarters average shows compounding beats frequent trading (9.1% turnover).

- Quality Endures Cycles: Fintech, home improvement, and digital consumer staples weather storms better than broad indices.

- Position Sizing is Dynamic: Consistent reductions signal constant valuation vigilance, freeing capital for asymmetric bets.

These lessons, drawn from their portfolio evolution, offer a blueprint for building wealth through selective conviction.

Looking Ahead: What Comes Next?

With portfolio size down to 22 and significant trims generating liquidity (implied cash from ~15% average reductions across top holdings), Ensemble appears positioned for opportunistic buys. The absence of new positions in the top 10 suggests they're hunting beyond current leaders—potentially in undervalued industrials, healthcare, or emerging moats overlooked by growth-chasers. Low turnover hints at waiting for better entry points amid 2024's market highs.

Current holdings like Mastercard and Alphabet set up well for economic recovery, with consumer proxies (Home Depot, Booking) poised for housing/travel rebounds. In a potential 2025 slowdown, their quality focus could shine, especially if rates ease. Track their next 13F on ValueSense for signals on fresh convictions.

FAQ about Ensemble Capital Management Portfolio

Q: Why did Ensemble reduce every top 10 holding in Q3 2024?

A: The uniform trims (7-24%) across leaders like NVR, Home Depot, and Booking reflect valuation discipline—locking in gains after strong rallies while maintaining core exposure. This generated cash amid high market valuations, per their 13F.

Q: How concentrated is Ensemble's strategy, and is it risky?

A: Extremely—top 10 at 66.5% across 22 positions—but mitigated by quality moats and 25-quarter holds. It's high-conviction value investing, not speculation; historical performance justifies the risk for aligned investors.

Q: What sectors dominate Ensemble's portfolio?

A: Consumer discretionary (~28%: HD, BKNG, NVR, RACE), financial services/fintech (~20%: MA, BR, PAYX), and tech/comms (~19%: NFLX, GOOGL, ADI). Focus on resilient, moat-heavy names avoids broad beta.

Q: How can I track Ensemble Capital's future moves?

A: Use ValueSense's superinvestor tracker at https://valuesense.io/superinvestors/ensemble-capital for real-time 13F updates (note 45-day lag). Combine with intrinsic value tools for your own analysis.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2026)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!