Gardner Russo & Quinn Portfolio in 2026: Top Holdings & Recent Changes

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

Gardner Russo & Quinn, led by veteran fund manager Thomas Russo, showcases its disciplined global value approach in the latest 13F filing. Their $9.3B portfolio reflects strategic trims in core mega-cap positions amid market highs, alongside bold new bets on streaming and materials that signal confidence in select growth narratives.

Portfolio Overview: Extreme Concentration with Global Flair

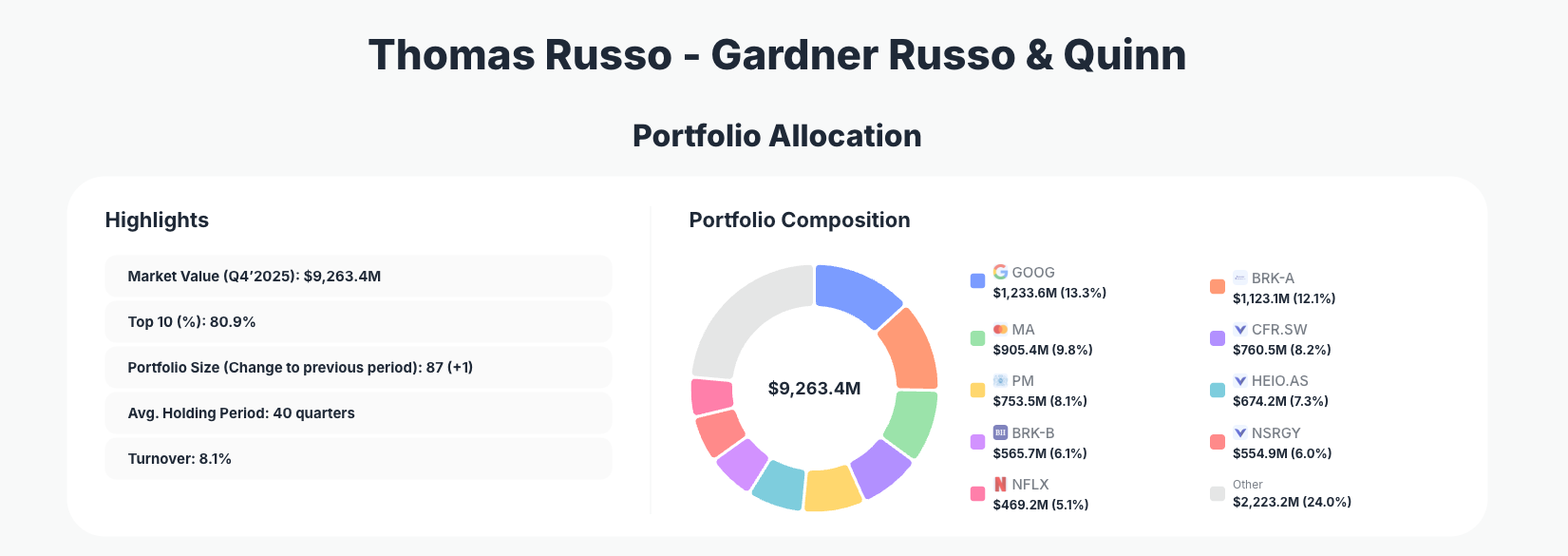

Portfolio Highlights (Q4’2025): - Market Value: $9,263.4M - Top 10 Holdings: 80.9% - Portfolio Size: 87 +1 - Average Holding Period: 40 quarters - Turnover: 8.1%

The Gardner Russo & Quinn portfolio exemplifies a high-conviction strategy, with the top 10 holdings commanding a staggering 80.9% of the $9.3 billion total. This level of concentration underscores Thomas Russo's philosophy of owning exceptional global businesses for decades, rather than chasing breadth. The addition of one new position brings the total to 87, yet turnover remains low at 8.1%, indicating minimal churn and a focus on long-term compounding.

An average holding period of 40 quarters—over 10 years—highlights the firm's patience, allowing winners like GOOG and BRK-A to mature despite recent trims. This portfolio balances U.S. giants with international consumer staples, reflecting a moat-focused approach resilient to economic cycles. Recent moves suggest tactical profit-taking in overvalued names while initiating aggressive positions in high-growth outliers.

Top Holdings: Strategic Trims and Explosive New Bets

The portfolio leads with Alphabet Inc. (GOOG) at 13.3%, though trimmed by 15.46%—a significant reduction signaling caution on tech valuations after strong gains. Close behind is Berkshire Hathaway Inc. (BRK-A) (12.1%, Reduce 3.44%), maintaining its role as a core conviction holding, paired with BRK-B (6.1%, Reduce 3.10%) for diversified exposure to the Berkshire ecosystem.

Mastercard Incorporated (MA) holds steady at 9.8% after a modest Reduce 2.12%, embodying payment network durability, while Compagnie Financiere Richemont (8.2%, Reduce 2.83%) reflects ongoing commitment to luxury goods. On the addition side, Philip Morris International Inc. (PM) grew to 8.1% with an Add 0.76%, betting on tobacco's defensive cash flows. Heineken Holding NV (7.3%, Reduce 0.92%) and Nestle SA Sponsored ADR (6.0%, Reduce 2.79%) anchor the consumer staples theme with minor adjustments.

Standouts include the explosive Netflix, Inc. (NFLX) initiation at 5.1% via Add 872.89%, a massive new position highlighting conviction in streaming dominance, and Martin Marietta Materials, Inc. (MLM) (4.9%, Add 5.68%), adding infrastructure cyclicality. These 10 positions, all with notable changes, dominate the Gardner Russo & Quinn portfolio, blending timeless quality with opportunistic growth.

What the Portfolio Reveals

Gardner Russo & Quinn's Q4 moves reveal a strategy prioritizing quality compounders with global moats, even at premium valuations. Trims in GOOG, MA, and Berkshire shares suggest profit-taking amid peak multiples, while adds in NFLX and MLM indicate selective growth exposure.

Sector focus spans tech (24%+ via GOOG/NFLX), financials (Berkshire/MA), luxury/consumer (Richemont/Heineken/Nestle/PM), showing diversification beyond U.S. borders—heavy European tilt via ADRs underscores geographic risk management. Dividend strategy shines in PM and staples, providing yield stability, balanced by non-dividend growers like NFLX.

This approach manages risk through extreme concentration (80.9% top 10) in proven franchises, low turnover, and decade-long holds, betting on enduring competitive advantages over short-term momentum.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Portfolio Concentration Analysis

| Position | Value | % of Portfolio | Recent Change |

|---|---|---|---|

| Alphabet Inc. (GOOG) | $1,233.6M | 13.3% | Reduce 15.46% |

| Berkshire Hathaway Inc. (BRK-A) | $1,123.1M | 12.1% | Reduce 3.44% |

| Mastercard Incorporated (MA) | $905.4M | 9.8% | Reduce 2.12% |

| Compagnie Financiere Richemont (_) | $760.5M | 8.2% | Reduce 2.83% |

| Philip Morris International Inc. (PM) | $753.5M | 8.1% | Add 0.76% |

| Heineken Holding NV (_) | $674.2M | 7.3% | Reduce 0.92% |

| Berkshire Hathaway Inc. (BRK-B) | $565.7M | 6.1% | Reduce 3.10% |

| Nestle SA Sponsored ADR (_) | $554.9M | 6.0% | Reduce 2.79% |

| Netflix, Inc. (NFLX) | $469.2M | 5.1% | Add 872.89% |

| Martin Marietta Materials, Inc. (MLM) | $452.4M | 4.9% | Add 5.68% |

This table illustrates Gardner Russo & Quinn's hallmark concentration, with the top holding at 13.3% and the decile summing to 80.9%—far above diversified peers. The pattern of reductions in six of ten positions (totaling ~28% trimmed) reflects disciplined rebalancing, freeing capital for high-conviction adds like NFLX's 872.89% explosion and PM's nudge higher. Berkshire's dual-class presence (18.2% combined) signals ultimate trust in quality conglomerates, while global names like Richemont and Nestle add currency and sector hedges. Overall, this setup prioritizes moat strength over diversification, betting big on businesses that withstand inflation and disruption.

Investment Lessons from Thomas Russo's Gardner Russo & Quinn Approach

- Concentrate ruthlessly in understood businesses: 80.9% in top 10 shows conviction trumps diversification when you grasp global moats like GOOG or MA.

- Patience defines returns: 40-quarter average hold proves selling winners prematurely destroys compounding—exemplified by long-term staples like Nestle.

- Trim winners, hunt asymmetric opportunities: Major GOOG cut funded 872% NFLX ramp, balancing valuation discipline with growth bets.

- Global quality over domestic growth: European consumer giants alongside U.S. tech highlight borderless moat hunting.

- Low turnover builds conviction: 8.1% churn avoids noise, letting positions like Berkshire mature through cycles.

Looking Ahead: What Comes Next?

With trims generating liquidity from a fully invested $9.3B book, Gardner Russo & Quinn appears positioned for opportunistic deployment amid 2026 uncertainties. The portfolio's low turnover and new position (+1 to 87) suggest selective expansion into undervalued compounders, potentially in consumer resilience or infrastructure via MLM expansion.

Market highs favor further trims in tech like GOOG, while NFLX's bet eyes AI-driven streaming monetization. Staples and Berkshire provide downside protection, setting up for volatility—watch for adds in defensive growth as rates stabilize.

FAQ about Gardner Russo & Quinn Portfolio

Q: What are the biggest changes in Gardner Russo & Quinn's Q4 2025 13F?

A: Key moves include a 15.46% trim in GOOG (top holding), 3-4% reductions in Berkshire shares and MA, offset by a massive 872.89% add to NFLX and smaller boosts to PM and MLM.

Q: Why is Gardner Russo & Quinn's portfolio so concentrated?

A: Thomas Russo favors deep conviction in 10-15 global moats, with 80.9% in top 10, enabling outsized returns from compounders like Berkshire and Nestle over diversification.

Q: What sectors dominate the portfolio?

A: Tech (~24% via GOOG/NFLX), financials/conglomerates (Berkshire/MA ~28%), and consumer staples/luxury (PM/Heineken/Nestle/Richemont ~30%), blending growth with defensive global brands.

Q: How can I track Gardner Russo & Quinn's future 13F filings?

A: Use ValueSense's superinvestor tracker at valuesense.io/superinvestors/gardner-russo-quinn for real-time updates—note the 45-day 13F lag means Q1 2026 data arrives mid-May.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2026)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!