HH International Portfolio in 2026: Top Holdings & Recent Changes

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

H&H International continues to demonstrate why extreme concentration paired with disciplined rebalancing can generate exceptional returns. The fund manager Duan Yongping's Q3 2025 portfolio reveals a masterclass in high-conviction investing, with $14.7 billion deployed across just 11 positions that reflect an unwavering focus on quality businesses trading at attractive valuations. The latest quarterly moves signal strategic recalibration—most notably a massive 53.53% addition to Berkshire Hathaway, while simultaneously trimming exposure to Chinese tech and semiconductor positions, suggesting a deliberate shift in geographic and sector positioning.

Portfolio Overview: Ultra-Concentrated Excellence with Surgical Precision

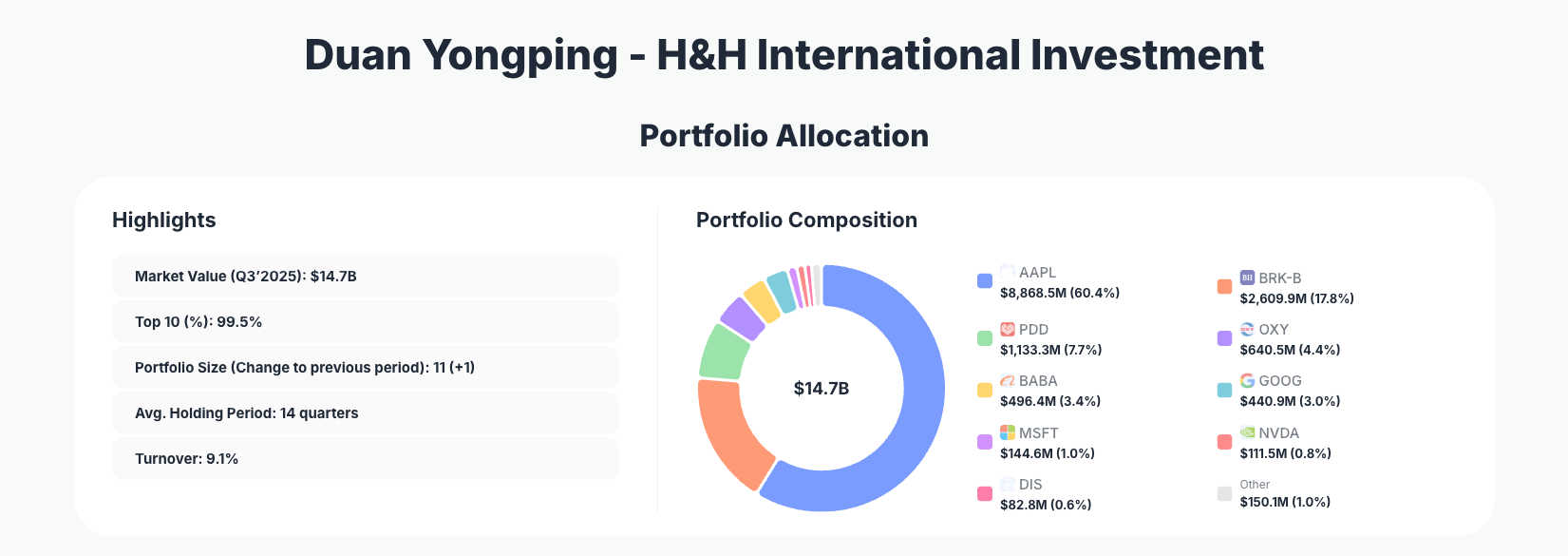

Portfolio Highlights (Q3 2025): - Market Value: $14.7B - Top 10 Holdings: 99.5% - Portfolio Size: 11 positions (+1 new addition) - Average Holding Period: 14 quarters (3.5 years) - Turnover: 9.1%

H&H International's portfolio structure exemplifies the power of conviction-based investing. With 99.5% of assets concentrated in the top 10 holdings and only 11 total positions, this is not a diversified fund—it's a carefully curated collection of businesses that Duan Yongping believes offer exceptional value. The remarkably low 9.1% turnover rate indicates that core positions remain stable, with changes reflecting deliberate strategic adjustments rather than reactive trading.

The 14-quarter average holding period (approximately 3.5 years) reveals a patient, fundamental-focused approach. This isn't a fund chasing quarterly momentum; it's an investor willing to sit through volatility while thesis and valuation dynamics evolve. The addition of one new position in Q3 2025 suggests selective opportunism—the fund is not aggressively deploying capital, but when it does, the conviction must be substantial.

What makes this portfolio particularly noteworthy is the balance between stability and adaptation. The low turnover combined with strategic moves like the 53.53% addition to Berkshire Hathaway demonstrates that H&H International doesn't abandon its process during market dislocations. Instead, it uses volatility as an opportunity to upgrade positions within its existing framework.

Top Holdings Analysis: Apple Dominance and Strategic Rebalancing

The portfolio is anchored by Apple at a commanding 60.4% of total assets, though the fund reduced this position by a modest 0.82%—a surgical trim that maintains conviction while taking marginal profits. This level of concentration in a single stock is extraordinary, yet it reflects Duan Yongping's deep conviction in Apple's competitive moat, cash generation, and valuation relative to intrinsic value.

The second-largest position, Berkshire Hathaway, received a dramatic 53.53% addition, now representing 17.8% of the portfolio. This aggressive move is particularly significant—it signals that despite Berkshire's massive scale, Duan sees compelling value at current prices. The addition suggests confidence in both Berkshire's operational performance and its positioning for a potentially lower-rate environment in 2026.

PDD Holdings 7.7% saw a minor 1.02% reduction, maintaining its third-largest position. This Chinese e-commerce and fintech platform remains a core holding despite the fund's broader pullback from Chinese tech exposure, suggesting selective confidence in PDD's business model and growth trajectory.

The portfolio's geographic and sector rebalancing becomes evident in the significant reductions: Alibaba was cut by 25.86% to just 3.4%, while NVIDIA experienced a substantial 38.04% reduction to 0.8%. These moves suggest a reassessment of valuations in high-growth tech and semiconductor spaces, potentially reflecting concerns about stretched multiples or shifting competitive dynamics.

Alphabet received a 6.93% trim to 3.0%, while Occidental Petroleum 4.4% and Microsoft 1.0% remained unchanged, signaling stable conviction in these positions. Disney 0.6% also held steady, while ASML received a new buy at 0.5%, adding a semiconductor equipment manufacturer to the portfolio—a strategic addition that may hedge against pure semiconductor exposure while maintaining exposure to the AI infrastructure buildout.

What the Portfolio Reveals About Current Strategy

The Q3 2025 moves paint a clear picture of H&H International's evolving market outlook:

Quality Over Growth at Any Price: The reduction in high-flying semiconductor and Chinese tech positions, combined with the aggressive addition to Berkshire Hathaway, suggests a pivot toward proven, cash-generative businesses. This isn't a rejection of technology—Apple remains 60% of the portfolio—but rather a recalibration toward quality businesses with sustainable competitive advantages trading at reasonable valuations.

Geographic Rebalancing: The 25.86% cut to Alibaba and maintenance of PDD at reduced levels indicates a more cautious stance on Chinese equities broadly, while the Berkshire addition and Apple maintenance suggest confidence in U.S. large-cap quality. This may reflect concerns about Chinese regulatory environment, geopolitical tensions, or simply valuation-driven rebalancing.

Valuation Discipline: The NVIDIA reduction of 38.04% is particularly telling. Despite AI's transformative potential, the fund appears to believe current valuations don't adequately compensate for risks. This reflects the disciplined value-investing approach that defines H&H International—conviction in quality doesn't mean conviction at any price.

Selective Opportunism: The ASML buy and Berkshire addition suggest the fund is deploying capital where it sees the most attractive risk-reward, rather than maintaining static allocations. The low overall turnover combined with these strategic moves indicates a "buy the dip" mentality applied to high-quality businesses.

Portfolio Concentration Analysis

| Position | Value | % of Portfolio | Recent Change |

|---|---|---|---|

| Apple Inc. (AAPL) | $8,868.5M | 60.4% | Reduce 0.82% |

| Berkshire Hathaway (BRK-B) | $2,609.9M | 17.8% | Add 53.53% |

| PDD Holdings (PDD) | $1,133.3M | 7.7% | Reduce 1.02% |

| Occidental Petroleum (OXY) | $640.5M | 4.4% | No change |

| Alibaba Group (BABA) | $496.4M | 3.4% | Reduce 25.86% |

| Alphabet Inc. (GOOG) | $440.9M | 3.0% | Reduce 6.93% |

| Microsoft Corporation (MSFT) | $144.6M | 1.0% | No change |

| NVIDIA Corporation (NVDA) | $111.5M | 0.8% | Reduce 38.04% |

| The Walt Disney Company (DIS) | $82.8M | 0.6% | No change |

| ASML Holding N.V. (ASML) | $77.4M | 0.5% | Buy |

This concentration profile is extreme by institutional standards, yet it reflects a deliberate strategy rather than oversight. The top two positions—Apple and Berkshire Hathaway—comprise 78.2% of the portfolio, a level of concentration that would be unacceptable for most fund managers but perfectly aligned with H&H International's conviction-based approach.

The 99.5% concentration in the top 10 holdings leaves minimal room for diversification benefits, but it maximizes the impact of the fund's best ideas. This structure works only when the manager has genuine conviction in valuations and competitive positioning—and the 14-quarter average holding period suggests Duan Yongping is willing to live with volatility to capture long-term value creation.

The recent moves—particularly the Berkshire addition and Alibaba reduction—show that concentration doesn't mean stagnation. The fund actively rebalances when valuations shift, deploying capital to the most attractive opportunities while trimming positions that have appreciated or become less compelling on a risk-adjusted basis.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Investment Lessons from H&H International's Approach

Conviction Requires Concentration: H&H International demonstrates that true conviction in a business thesis justifies significant portfolio weight. The 60.4% Apple position isn't reckless—it reflects deep analysis of Apple's moat, cash generation, and valuation. For retail investors, this suggests that diversification for its own sake may be counterproductive; if you've done the work and understand a business, meaningful position sizing can enhance returns.

Valuation Discipline Trumps Growth Stories: The 38% NVIDIA reduction despite AI's transformative potential shows that even compelling secular trends don't justify any valuation. H&H International is willing to miss upside if the risk-reward isn't attractive. This is a critical lesson for investors tempted by momentum in high-growth sectors.

Patient Capital Compounds: The 14-quarter average holding period combined with 9.1% turnover reveals that long-term wealth creation comes from holding quality businesses through cycles, not from frequent trading. The fund's willingness to sit through volatility while thesis remains intact is a hallmark of successful value investing.

Rebalancing is Active Management: Low turnover doesn't mean passive holding. The Berkshire addition and Alibaba reduction show that H&H International actively reassesses positions as valuations and competitive dynamics evolve. The fund rebalances toward the most attractive opportunities, not away from volatility.

Geographic and Sector Flexibility Within a Framework: While maintaining core positions in Apple and quality businesses, the fund is willing to reduce Chinese tech exposure and trim semiconductor positions. This flexibility within a disciplined framework allows adaptation to changing market conditions without abandoning the core investment process.

Looking Ahead: What Comes Next?

H&H International's Q3 2025 positioning sets up intriguingly for 2026. The aggressive Berkshire addition suggests confidence in a lower-rate environment that could benefit asset managers and financial services. The maintenance of Apple at 60% reflects conviction that the company's services transition and AI integration will drive long-term value creation.

The reduction in NVIDIA and Alibaba, combined with the ASML buy, suggests the fund is positioning for a potential slowdown in AI capex growth while maintaining exposure to semiconductor equipment—a more defensive posture that hedges against AI enthusiasm cooling while preserving upside if the buildout continues.

With 99.5% of assets in the top 10 holdings and only 11 total positions, the fund has minimal dry powder for new investments. Future moves will likely come through rebalancing existing positions rather than new additions, unless a significant market dislocation creates compelling opportunities. The low turnover rate suggests the fund is comfortable with current positioning and will only make changes if valuations shift materially or thesis dynamics evolve.

The 14-quarter average holding period indicates patience for Apple and Berkshire to compound value over the next 2-3 years, suggesting Duan Yongping is not expecting near-term exits from core positions. This long-term orientation, combined with disciplined valuation work, positions H&H International well for capturing value creation in quality businesses through market cycles.

FAQ About H&H International's Portfolio

Q: Why did H&H International add 53.53% to Berkshire Hathaway in Q3 2025?

A: The aggressive Berkshire addition suggests Duan Yongping sees compelling value at current prices, likely reflecting confidence in Berkshire's operational performance, cash generation, and positioning for a potentially lower-rate environment in 2026. The move also signals that despite Berkshire's massive scale ($14.7B in assets), the fund believes the company's intrinsic value exceeds current market price. This is consistent with H&H International's value-investing approach—deploying capital to the most attractive risk-reward opportunities.

Q: What does the 38% reduction in NVIDIA tell us about H&H International's AI outlook?

A: The significant NVIDIA trim doesn't necessarily indicate bearishness on AI—Apple remains 60% of the portfolio, reflecting confidence in AI's transformative potential. Rather, the reduction suggests valuation discipline: the fund believes NVIDIA's current price doesn't adequately compensate for risks, including potential slowdowns in capex growth, competitive pressures, or multiple compression. This reflects a core principle of value investing—conviction in a secular trend doesn't mean conviction at any valuation.

Q: How concentrated is H&H International's portfolio, and is this risky?

A: With 99.5% in the top 10 holdings and 60.4% in Apple alone, this is an extremely concentrated portfolio. However, concentration isn't inherently risky—it's a deliberate strategy reflecting deep conviction in valuations and competitive positioning. The 14-quarter average holding period and 9.1% turnover suggest Duan Yongping has done extensive analysis and is willing to live with volatility to capture long-term value creation. For retail investors, this demonstrates that meaningful position sizing in well-researched ideas can enhance returns, though it requires genuine conviction and analytical rigor.

Q: What's the significance of the 25.86% Alibaba reduction?

A: The substantial Alibaba cut suggests H&H International is reassessing Chinese tech exposure, potentially reflecting concerns about regulatory environment, competitive dynamics, or valuation. However, the fund maintained a 3.4% position, indicating it hasn't abandoned conviction in the business. This selective reduction—keeping some exposure while trimming significantly—is typical of disciplined rebalancing: the fund is reducing risk while maintaining optionality if valuations become more attractive.

Q: How can I track H&H International's portfolio and follow their moves?

A: You can monitor H&H International's quarterly 13F filings and portfolio changes on ValueSense's H&H International superinvestor tracker. The platform provides real-time analysis, historical changes, and visualizations of all holdings. Keep in mind that 13F filings carry a 45-day reporting lag, so the reported positions may differ from the fund's real-time book—but they remain a valuable window into the strategy's structure and evolution. ValueSense's tools make it easy to track position changes, monitor concentration levels, and compare H&H International's moves against other superinvestors.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2026)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!