Investing for Growth: How to make money by only buying the best companies in the world by Terry Smith

Welcome to the Value Sense Blog, your resource for insights on the stock market! You're reading a book review written by the valuesense.io team.

On our platform, you'll find stock research and insights across all sectors. Dive into our research products and learn more about our unique approach at valuesense.io

We offer over 360+ automated stock ideas, a free AI-powered stock screener, interactive stock charting tools, and more than 10 intrinsic value models — all designed to help investors find undervalued growth opportunities.

Book Overview

“Investing for Growth: How to make money by only buying the best companies in the world” by Terry Smith is a modern classic that distills decades of investment wisdom into actionable guidance for today’s investors. Terry Smith, often referred to as “the English Warren Buffett,” is the founder and CEO of Fundsmith, one of the UK’s largest and most successful investment funds. With a career spanning investment banking, research, and fund management, Smith brings a rare combination of analytical rigor and practical experience to the table. His credentials are impressive: Fundsmith Equity Fund, launched in 2010, has consistently outperformed its benchmarks, making Smith’s approach widely respected among both retail and institutional investors.

The book was published in 2020, a decade after the launch of Fundsmith, and captures a period marked by significant market upheaval, including the aftermath of the Global Financial Crisis and the onset of the COVID-19 pandemic. This historical context is crucial, as Smith’s reflections are grounded in real-world events and hard-earned lessons. The narrative is structured around his annual letters, shareholder communications, and thematic essays, which collectively offer a transparent look into both the successes and challenges faced by Fundsmith over its first ten years.

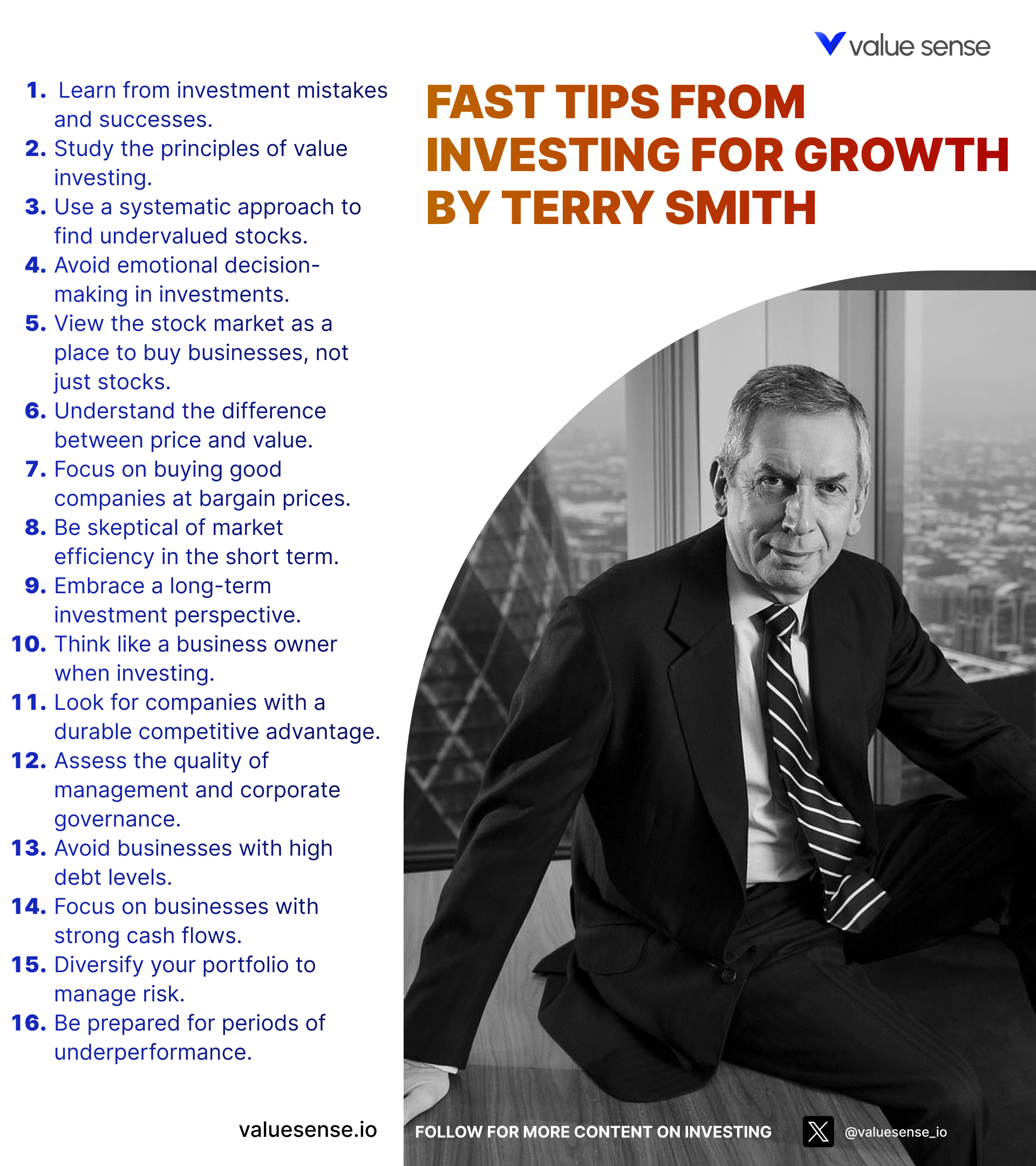

At its core, “Investing for Growth” is a manifesto for quality investing. Smith argues that the best way to build wealth is to buy and hold shares in high-quality companies—those with durable competitive advantages, consistent growth, and strong returns on capital. He contrasts this with the pitfalls of traditional value investing, market timing, and complex financial engineering, making a compelling case for simplicity, patience, and discipline. The book’s purpose is not just to explain Fundsmith’s strategy, but to empower readers to think critically about their own investment decisions and to adopt principles that have stood the test of time.

This book is considered essential reading for several reasons. First, it demystifies the investment process, stripping away jargon and focusing on what truly matters: the underlying economics of businesses. Second, it provides a rare level of transparency, with Smith openly sharing mistakes, performance data, and the rationale behind major decisions. Third, Smith’s willingness to challenge industry norms—such as high management fees, the proliferation of ETFs, and the obsession with market timing—sets the book apart from more conventional investment guides. His blend of skepticism and optimism offers a refreshing perspective in a field often dominated by dogma or short-term thinking.

“Investing for Growth” is particularly valuable for long-term investors, both novice and experienced, who are seeking a clear, evidence-based framework for building wealth. It is also a must-read for financial professionals interested in fund management best practices and for anyone curious about the realities of running a successful investment fund. What makes the book unique is its combination of practical advice, historical analysis, and candid reflections—delivered with Smith’s trademark wit and intellectual honesty. Unlike many investment books that focus on trading tactics or market predictions, this work is fundamentally about mindset, process, and the enduring power of quality.

Key Themes and Concepts

“Investing for Growth” is rich with themes that challenge conventional wisdom and provide a robust foundation for long-term investment success. At its heart, the book is a treatise on the power of quality—why buying and holding the world’s best companies is a superior strategy to chasing undervalued or speculative stocks. Smith weaves together lessons from history, critiques of industry practices, and practical advice, creating a thematic tapestry that is both timeless and highly relevant to the challenges investors face today.

Several key themes run throughout the book, each supported by detailed analysis, real-world examples, and actionable insights. These themes not only define Smith’s investment philosophy but also serve as a guide for investors seeking to navigate the complexities of modern markets. Below, we explore the most important themes, illustrating how they appear throughout the book and how they can be applied in practice.

- Quality Investing: The central pillar of Smith’s philosophy is the relentless pursuit of quality. He defines quality companies as those with high returns on capital, strong competitive advantages, and the ability to grow profits consistently over time. Smith argues that paying a premium for such companies is justified, as their superior economics compound over the long term. Throughout the book, he contrasts this approach with traditional value investing, which often focuses on low price-to-earnings ratios or distressed assets. Smith provides numerous examples, such as the long-term performance of companies like Microsoft and Unilever, to demonstrate that quality trumps cheapness. For investors, this means prioritizing business fundamentals over market noise and resisting the temptation to chase short-term bargains.

- Critique of Traditional Fund Management: Smith is highly critical of the fund management industry, particularly its fee structures and incentives. He exposes how high management fees and performance fees erode investor returns, and how many funds fail to align their interests with those of their clients. Smith advocates for greater transparency, lower costs, and meaningful co-investment by fund managers. He provides data showing the impact of fees on long-term compounding and highlights the industry’s tendency to overcomplicate investment products to justify higher charges. This theme is a call to action for investors to scrutinize the funds they invest in, demand transparency, and favor managers who “eat their own cooking.”

- Market Timing and Investor Behavior: Another recurring theme is the futility of market timing and the dangers of emotional investing. Smith draws on historical examples, such as the Wall Street Crash and various bear markets, to show that even the most sophisticated investors struggle to predict market movements. He emphasizes the importance of staying invested, maintaining a long-term perspective, and avoiding the psychological traps of fear and greed. Smith’s annual letters often include data on fund inflows and outflows, illustrating how investors tend to buy high and sell low. The practical takeaway is clear: investors should focus on time in the market, not timing the market, and develop the discipline to hold through volatility.

- Value Creation and Shareholder Returns: Smith delves deeply into the mechanisms by which companies create value for shareholders, such as share buybacks and dividends. He explains the conditions under which buybacks enhance shareholder value—namely, when shares are repurchased below intrinsic value—and warns against buybacks driven by management incentives or financial engineering. Smith also compares the merits of buybacks versus dividends, advocating for transparent accounting and rational capital allocation. For investors, understanding these mechanisms is crucial for evaluating management quality and the sustainability of returns.

- Lessons from Historical Market Events: The book is replete with lessons drawn from major market events and crises, from the Wall Street Crash of 1929 to the Global Financial Crisis and beyond. Smith uses these episodes to highlight the recurring patterns of investor behavior, the dangers of leverage, and the importance of resilience. He argues that crises present opportunities for disciplined investors to acquire quality assets at attractive prices, provided they have the courage and resources to act. This theme reinforces the value of historical perspective and the need to prepare for, rather than fear, market downturns.

- Direct Communication with Investors: A distinctive feature of Fundsmith’s approach is its commitment to direct, transparent communication with investors. Smith’s annual letters and shareholder updates are candid, data-rich, and free from marketing spin. He believes that clear communication builds trust and helps investors understand the rationale behind strategic decisions, reducing the risk of panic or misinterpretation during turbulent times. This theme underscores the importance of transparency and education in fostering long-term investor loyalty and success.

- Debunking Investment Myths: Throughout the book, Smith challenges widely held beliefs about passive investing, asset allocation, and the role of small-cap stocks. He provides evidence-based arguments to debunk the myth that passive investing is always superior, or that diversification across many asset classes guarantees safety. Smith’s willingness to question orthodoxy encourages investors to think critically and avoid blindly following industry trends.

Book Structure: Major Sections

Part 1: Foundations of Investment Philosophy

This opening section, covering chapters 1 through 5, lays the groundwork for Terry Smith’s investment philosophy. It introduces readers to the core principles that underpin Fundsmith’s approach, including a resolute focus on quality companies and a healthy skepticism toward traditional fund management practices. Smith uses these chapters to set expectations, challenge industry norms, and explain why buying only the best companies is a superior long-term strategy.

Key concepts in this section include the definition of a quality company—one with high returns on capital, strong brand power, and robust cash flows. Smith critiques the high fees and opaque structures that plague much of the fund management industry, arguing that these practices often work against the interests of ordinary investors. He also introduces the “Fundsmith way,” emphasizing simplicity, transparency, and a relentless focus on business fundamentals. Real-world examples, such as the long-term outperformance of consumer staples and technology leaders, are used to illustrate these points.

For investors, the practical application is clear: prioritize quality over quantity, avoid unnecessary complexity, and be wary of high-fee products that promise more than they deliver. Smith’s insistence on manager co-investment and fee transparency serves as a model for selecting both funds and individual stocks. Adopting these principles can help investors sidestep common pitfalls and align their portfolios with long-term wealth creation.

In today’s market environment—dominated by low-cost ETFs, robo-advisors, and a proliferation of financial products—these foundational lessons are more relevant than ever. Smith’s critique of industry practices encourages investors to look past marketing hype and focus on what truly matters: the underlying economics of the businesses they own. This section provides a timeless blueprint for building a resilient, high-quality portfolio.

Part 2: Critical Analysis of Investment Vehicles

Chapters 6 through 10 form a thematic exploration of investment vehicles, with a particular focus on exchange-traded funds (ETFs) and share buybacks. Smith dissects the risks and rewards associated with these instruments, providing a nuanced perspective that goes beyond surface-level analysis. The unifying theme is a critical examination of how different vehicles impact investor returns and market behavior.

Smith highlights the dangers of synthetic and leveraged ETFs, exposing their hidden risks, such as counterparty exposure and the distorting effects of daily compounding. He also scrutinizes share buybacks, arguing that they can create value when executed at prices below intrinsic value but can destroy value when used to manipulate earnings per share or satisfy management incentives. Data-driven examples illustrate how these practices have played out in real companies, sometimes to the detriment of long-term shareholders.

Investors can apply these insights by conducting due diligence on the structure of investment products and understanding the motivations behind corporate actions. Smith’s analysis encourages a skeptical approach to financial innovation and a preference for straightforward, transparent vehicles. By focusing on intrinsic value and capital allocation discipline, investors can avoid the traps set by poorly designed products and misaligned incentives.

As financial markets grow increasingly complex, with new ETFs and buyback programs announced daily, Smith’s warnings are especially pertinent. This section provides a toolkit for navigating the crowded landscape of modern investment products, empowering investors to make informed, rational choices that align with their long-term goals.

Part 3: Lessons from Market Events and Crises

This section, spanning chapters 11 through 15, draws on historical market events and crises to extract enduring lessons about investor behavior and market dynamics. Smith uses case studies—including the Wall Street Crash and the UBS trading scandal—to illustrate how fear, greed, and herd mentality can drive markets to extremes.

Key concepts include the dangers of speculation, the limitations of economic forecasting, and the psychological traps that ensnare both amateur and professional investors. Smith demonstrates how attempts at market timing often backfire, leading to subpar returns and missed opportunities. He uses historical data to show that staying invested through downturns is typically more rewarding than trying to predict market tops and bottoms.

For investors, the takeaway is to cultivate emotional discipline and a long-term perspective. By understanding the recurring patterns of market cycles, investors can prepare for volatility rather than react to it. Smith’s advice is to focus on business fundamentals, maintain adequate liquidity, and avoid leverage—especially during periods of market stress.

In the context of recent market turbulence, from the 2008 financial crisis to the COVID-19 selloff, these lessons are as relevant as ever. Smith’s historical approach reminds investors that while crises are inevitable, they also present opportunities for those who are prepared and disciplined. This section reinforces the value of patience, resilience, and a focus on quality amid uncertainty.

Part 4: Annual Reflections and Shareholder Communications

Chapters 16 through 20 comprise a series of annual letters and shareholder communications, offering a transparent window into Fundsmith’s performance and decision-making process. These chapters are unified by their commitment to openness, data-driven analysis, and direct engagement with investors.

Smith provides detailed performance reviews, benchmarking Fundsmith’s returns against relevant indices and explaining the drivers of outperformance or underperformance. He discusses key portfolio adjustments, the rationale behind major buys and sells, and the importance of maintaining a consistent investment process. The letters also address common investor concerns, such as dividend yields and the role of share buybacks, with candor and precision.

For investors, these communications serve as a model for effective stewardship and accountability. Smith’s willingness to admit mistakes, share detailed data, and explain his reasoning fosters trust and helps investors stay the course during volatile periods. The practice of regular, transparent updates can be adopted by individual investors as a way to track progress and maintain discipline.

In an era where many fund managers hide behind jargon or marketing spin, Smith’s approach stands out for its integrity and clarity. These annual reflections are not just a record of past performance—they are a masterclass in investor communication and a blueprint for building long-term relationships based on trust and transparency.

Part 5: Investment Strategies and Market Insights

The final thematic section, chapters 21 through 25, explores a range of investment strategies and market trends. Smith examines the role of different asset classes, the merits of small-cap stocks, and the evolving landscape of shareholder value creation. The unifying theme is a pragmatic, evidence-based approach to portfolio construction and market analysis.

Key concepts include the strategic use of small-caps in a global portfolio, the identification of bond proxies, and the evaluation of management’s ability to create sustainable value. Smith challenges the conventional wisdom on diversification, arguing that concentration in quality companies can be more effective than spreading bets across many mediocre assets. He also provides insights into the behavioral biases that influence asset allocation decisions.

Investors can apply these lessons by focusing on the quality and growth potential of individual holdings, rather than blindly diversifying for its own sake. Smith’s analysis of shareholder value metrics and management incentives offers a framework for evaluating potential investments and constructing resilient portfolios. The emphasis on evidence and pragmatism encourages investors to question received wisdom and adapt to changing market conditions.

As global markets become more interconnected and complex, the insights in this section provide a roadmap for navigating uncertainty and capturing long-term growth. Smith’s willingness to challenge orthodoxy and embrace innovation—while remaining grounded in fundamental analysis—makes this section especially valuable for forward-thinking investors.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Deep Dive: Essential Chapters

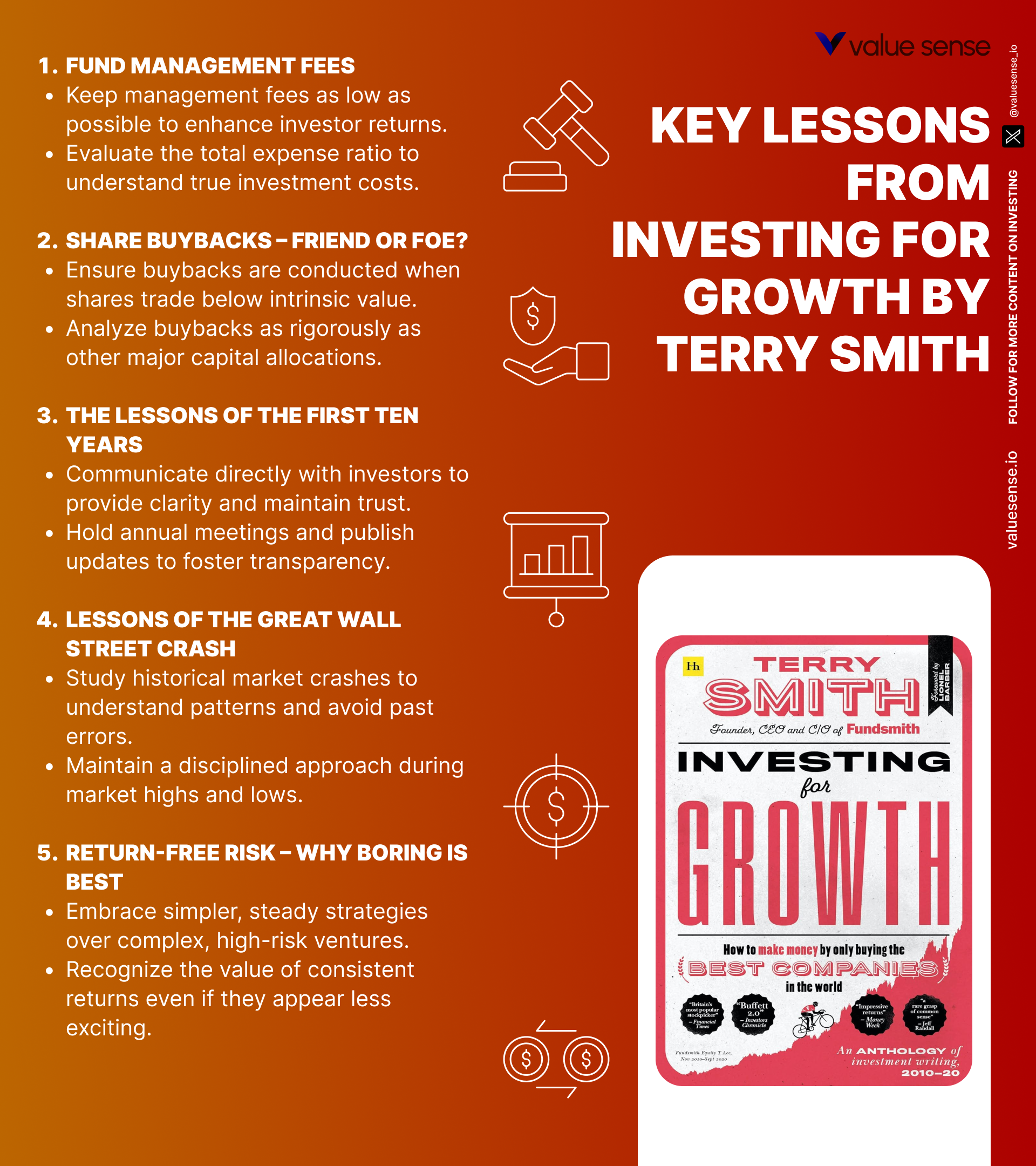

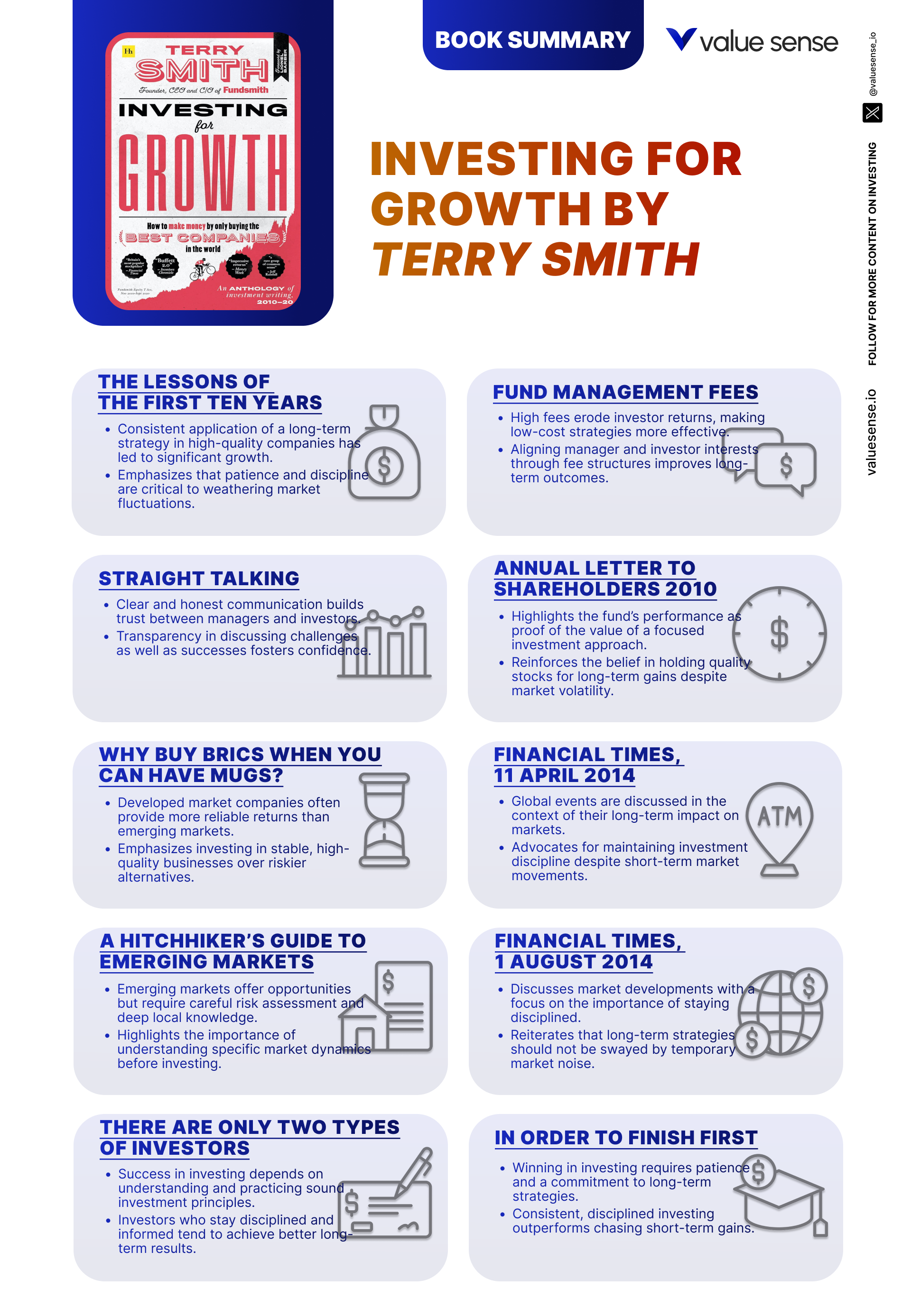

Chapter 2: The lessons of the first ten years

This chapter is a cornerstone of the book, providing a retrospective analysis of Fundsmith’s first decade. It is critically important because it distills the practical lessons learned from real-world experience into actionable guidance for investors. Smith uses this chapter to address misconceptions about quality investing, highlight the importance of intrinsic value, and reflect on the challenges of economic forecasting. The chapter sets the tone for the rest of the book, emphasizing transparency, humility, and a relentless focus on fundamentals.

Smith begins by sharing performance data that demonstrates the superiority of quality investing over both traditional value strategies and the broader market. He cites specific examples, such as the long-term outperformance of companies like Microsoft and L’Oréal, to illustrate the power of compounding returns. The chapter includes candid discussions of mistakes made, such as underestimating the resilience of certain business models or overreacting to macroeconomic forecasts. Smith also provides quotes from annual letters, reinforcing the importance of direct communication with investors and the avoidance of unnecessary complexity.

Investors can apply these lessons by prioritizing the identification and accumulation of high-quality companies with durable competitive advantages. Smith advocates for a disciplined approach, focusing on intrinsic value rather than short-term market fluctuations. He encourages investors to avoid the temptation to time the market or chase hot sectors, instead recommending a patient, long-term perspective. Practical steps include conducting thorough fundamental analysis, monitoring return on capital, and maintaining a concentrated portfolio of best ideas.

In the context of recent market volatility and the proliferation of passive investment vehicles, Smith’s reflections are especially relevant. The chapter’s emphasis on learning from mistakes, maintaining transparency, and focusing on what truly matters provides a blueprint for building resilience in any market environment. By sharing both successes and failures, Smith offers a rare level of candor that sets this chapter apart from more conventional investment literature.

Chapter 4: Fund management fees

This chapter is vital because it addresses one of the most significant—yet often overlooked—determinants of long-term investment returns: fees. Smith’s critique of traditional fund management fee structures is both rigorous and uncompromising, making this chapter essential reading for anyone investing through funds or considering professional management. The main concept is that high fees, particularly performance fees and opaque charges, can severely erode investor returns over time, undermining the benefits of compounding.

Smith provides detailed examples and data to illustrate how seemingly small differences in fees can lead to dramatically different outcomes over decades. He exposes the conflicts of interest inherent in performance fee arrangements and questions the alignment between fund managers and investors. The chapter includes quotes from industry reports and regulatory filings, highlighting the lack of transparency that often characterizes the sector. Smith also discusses the importance of manager co-investment, arguing that fund managers should have “skin in the game” to ensure their interests are aligned with those of their clients.

For investors, the practical application is to scrutinize the fee structures of any funds they consider. Smith recommends favoring funds with clear, low, and transparent fees, and avoiding those with complex or performance-based charges. He also suggests looking for managers who invest a significant portion of their own wealth alongside their clients, as this fosters accountability and long-term thinking. Investors should use available tools and disclosures to compare fee levels and assess their impact on projected returns.

Historically, the investment industry has been slow to reform fee practices, but the rise of low-cost index funds and increased regulatory scrutiny have begun to shift the landscape. Smith’s arguments remain highly relevant, particularly as new products—such as smart beta ETFs and alternative funds—proliferate. By shining a light on the true cost of investing, this chapter empowers readers to make more informed, cost-effective choices that enhance long-term wealth accumulation.

Chapter 7: Share buybacks – friend or foe?

This chapter is critically important because it tackles the contentious issue of share buybacks, a topic that has significant implications for shareholder value and corporate governance. Smith’s nuanced analysis goes beyond the simplistic “good or bad” dichotomy, exploring the conditions under which buybacks create or destroy value. The main concept is that buybacks can be a powerful tool for capital allocation, but only when executed with discipline and transparency.

Smith uses specific examples, such as the buyback programs of major US corporations, to illustrate both the benefits and pitfalls of this practice. He provides data on the impact of buybacks on earnings per share, return on equity, and overall shareholder returns. The chapter includes quotes from company filings and management statements, highlighting the motivations—both genuine and self-serving—that drive buyback decisions. Smith also compares buybacks to dividends, discussing the relative merits of each as a means of returning capital to shareholders.

Investors can apply these lessons by analyzing the context and rationale behind buyback announcements. Smith recommends assessing whether buybacks are conducted at prices below intrinsic value and whether they are funded by genuine excess cash or by taking on debt. He also advises investors to be wary of buybacks that are primarily designed to boost executive compensation or mask operational weaknesses. Practical steps include reviewing company disclosures, monitoring capital allocation policies, and favoring management teams with a track record of disciplined decision-making.

In recent years, buybacks have come under increased scrutiny from regulators, politicians, and investors alike. Smith’s balanced approach provides a framework for evaluating buybacks on a case-by-case basis, rather than adopting a blanket view. By focusing on the underlying economics and incentives, investors can make more informed judgments about the impact of buybacks on long-term value creation.

Chapter 9: Exchange-traded funds are worse than I thought

This chapter stands out for its critical examination of ETFs, particularly the risks associated with synthetic and leveraged products. Smith’s analysis is important because ETFs have become ubiquitous in modern portfolios, yet their complexities are often misunderstood by retail investors. The main concept is that not all ETFs are created equal, and some carry hidden risks that can undermine their perceived safety and efficiency.

Smith provides detailed explanations of how synthetic ETFs use derivatives and counterparty arrangements to replicate index performance, exposing investors to risks that are not present in traditional, physically-backed funds. He discusses the impact of daily compounding in leveraged ETFs, showing how these products can deviate significantly from their stated objectives over time. The chapter includes data on ETF failures and mis-selling scandals, as well as quotes from regulatory warnings and fund prospectuses. Smith also highlights the potential for liquidity mismatches and the dangers of herd behavior in ETF trading.

For investors, the practical application is to conduct thorough due diligence on any ETF before investing. Smith recommends understanding the structure, underlying assets, and counterparty exposures of each product. He suggests avoiding complex or leveraged ETFs unless the risks are fully understood and aligns with the investor’s objectives. Investors should also be aware of the potential for tracking errors and liquidity issues, especially during periods of market stress.

The explosive growth of the ETF industry has democratized access to global markets but has also introduced new risks. Smith’s warnings are especially timely given recent episodes of ETF volatility and the proliferation of niche products. By shedding light on the complexities and potential pitfalls of ETFs, this chapter equips investors to make more informed, prudent choices in constructing their portfolios.

Chapter 12: Lessons of the great Wall Street Crash

This chapter is essential because it draws timeless lessons from one of the most significant events in financial history—the Wall Street Crash of 1929. Smith uses this episode to explore the psychological and structural factors that contribute to market bubbles and crashes. The main concept is that speculation, leverage, and herd behavior are recurring features of financial markets, and that understanding these forces is key to long-term investment success.

Smith provides a detailed narrative of the events leading up to the crash, including the role of margin lending, rampant speculation, and regulatory failures. He uses historical data to illustrate the magnitude of the collapse and its aftermath, including the prolonged bear market and the impact on investor psychology. The chapter includes quotes from contemporary sources and reflections on the parallels between past and present market cycles. Smith also discusses the limitations of economic forecasting and the dangers of overconfidence.

Investors can apply these lessons by maintaining a healthy skepticism toward market exuberance and avoiding excessive leverage. Smith advocates for a long-term perspective, focusing on the underlying value of businesses rather than short-term price movements. He also recommends building portfolios that can withstand periods of volatility, including maintaining adequate liquidity and diversifying across high-quality assets.

In light of recent market bubbles and corrections, Smith’s historical analysis is highly relevant. The chapter’s emphasis on investor psychology, risk management, and the importance of learning from history provides a valuable framework for navigating future market cycles. By internalizing these lessons, investors can avoid the most common pitfalls that have plagued markets for generations.

---

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best) overall value plays for 2025

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

---

Chapter 16: Annual letter to shareholders 2011

This chapter is significant because it marks Fundsmith’s first full year of operation and sets the standard for the fund’s approach to transparency, performance analysis, and shareholder communication. Smith’s annual letter provides a detailed account of the fund’s results, the rationale behind key decisions, and the lessons learned from both successes and setbacks. The main concept is that candid, data-driven communication builds trust and helps investors stay focused on the long-term strategy.

Smith shares performance data, comparing Fundsmith’s returns to relevant benchmarks and dissecting the contributions of individual holdings. He discusses the impact of dividend yields, the role of share buybacks, and the reasoning behind portfolio adjustments. The letter includes specific examples of stocks that outperformed or underperformed, as well as reflections on broader market trends. Smith also addresses common investor questions and concerns, such as the sustainability of growth and the risks associated with concentration.

For investors, the practical application is to adopt a similar approach to tracking and communicating investment performance. Smith’s example demonstrates the value of regular, honest updates that go beyond headline returns to explain the underlying drivers of results. Investors can use this model to evaluate fund managers, assess the quality of their own decision-making, and maintain discipline during periods of volatility.

The tradition of annual letters, popularized by figures like Warren Buffett, is a hallmark of great investment stewardship. Smith’s 2011 letter stands out for its clarity, candor, and attention to detail, setting a benchmark for others in the industry. In a world where many fund managers obfuscate or deflect, Smith’s approach is a breath of fresh air and a valuable resource for investors seeking transparency and accountability.

Chapter 18: Ten golden rules of investment

This chapter is a distillation of Smith’s investment philosophy into ten practical, actionable rules. It is critically important because it provides a concise roadmap for successful investing, drawing on decades of experience and empirical evidence. The main concept is that adherence to a few fundamental principles can dramatically improve investment outcomes and reduce the risk of costly mistakes.

Smith lists and explains each rule in detail, covering topics such as focusing on quality companies, avoiding market timing, paying attention to valuation, and maintaining a long-term horizon. He provides examples and anecdotes to illustrate the application of each rule, drawing on both his own experience and the broader history of financial markets. The chapter includes memorable quotes and pithy observations that encapsulate the essence of disciplined investing.

Investors can apply these rules by using them as a checklist for evaluating potential investments and managing their portfolios. Smith recommends regular self-assessment to ensure that decisions are grounded in sound principles rather than emotional reactions or market fads. The rules serve as a framework for building resilience, maintaining focus, and avoiding the most common pitfalls that derail investors.

In an age of information overload and constant market noise, Smith’s ten golden rules provide a much-needed anchor. The chapter’s emphasis on simplicity, patience, and rationality is as relevant today as it was in previous generations. By internalizing these rules, investors can navigate the complexities of modern markets with greater confidence and clarity.

Chapter 22: Why it is safe to pay up for quality

This chapter is pivotal because it challenges the traditional value investing dogma that insists on buying only “cheap” stocks. Smith argues persuasively that paying a premium for high-quality companies is often justified by their superior growth prospects and resilience. The main concept is that growth is an essential component of value, and that quality companies can compound returns at high rates over long periods, even if their initial valuations appear elevated.

Smith provides data and case studies showing how companies with high returns on capital and strong competitive advantages have outperformed cheaper, lower-quality peers over time. He analyzes the drivers of intrinsic value, including earnings growth, reinvestment opportunities, and pricing power. The chapter includes quotes from industry legends and references to academic research that support the case for quality investing. Smith also addresses common misconceptions about high valuations, explaining the importance of looking beyond simple metrics like price-to-earnings ratios.

For investors, the takeaway is to focus on the sustainability and growth potential of businesses, rather than being fixated on short-term valuation multiples. Smith recommends conducting thorough due diligence to assess the true quality of a company’s business model and management team. He also suggests being willing to hold quality stocks through periods of market volatility, confident in their ability to deliver superior long-term returns.

In recent years, the debate between value and growth investing has intensified, with many investors questioning whether it is safe to “pay up” for quality. Smith’s analysis provides a compelling answer, grounded in both empirical evidence and practical experience. By reframing the discussion around intrinsic value and long-term compounding, this chapter offers a valuable perspective for navigating today’s dynamic markets.

Chapter 25: The myths of fund management

This chapter is essential because it debunks several pervasive myths that shape investor behavior and industry practices. Smith challenges conventional wisdom on topics such as passive investing, asset allocation, and the role of small-cap stocks, providing evidence-based arguments that encourage critical thinking. The main concept is that many widely held beliefs in the investment world are either outdated or unsupported by data, and that investors must be willing to question orthodoxy to achieve superior results.

Smith systematically addresses each myth, using data, case studies, and quotes from industry reports to expose their flaws. He critiques the notion that passive investing is always superior, highlighting the limitations of index construction and the potential for active management to add value in certain contexts. Smith also questions the obsession with diversification, arguing that concentration in quality companies can be more effective. The chapter includes discussions of asset allocation models, the risks of small-cap investing, and the importance of manager skill.

Investors can apply these insights by adopting a more nuanced approach to portfolio construction and manager selection. Smith recommends evaluating the evidence behind popular investment strategies and being open to alternative perspectives. He also suggests focusing on the underlying economics of investments, rather than relying on simplistic rules or industry dogma.

In a world where financial advice is often driven by marketing and groupthink, Smith’s willingness to challenge the status quo is both refreshing and necessary. This chapter encourages investors to think independently, question assumptions, and make decisions based on facts rather than fashion. By debunking investment myths, Smith empowers readers to take control of their financial futures.

Chapter 30: Never let a crisis go to waste

This chapter is particularly important because it reframes market crises as opportunities rather than threats. Smith argues that disciplined, long-term investors can use periods of market dislocation to acquire high-quality assets at attractive prices. The main concept is that crises, while painful in the short term, are an inevitable feature of financial markets and can be harnessed for long-term gain.

Smith provides historical examples, such as the Global Financial Crisis and the COVID-19 selloff, to illustrate how market downturns create opportunities for those with the courage and resources to act. He discusses the psychological barriers that prevent most investors from buying during periods of fear and uncertainty, and provides data on the subsequent recoveries of quality stocks. The chapter includes quotes from legendary investors and references to academic research on market cycles and behavioral finance.

For investors, the practical application is to maintain a watchlist of high-quality companies and to have a plan in place for deploying capital during market downturns. Smith recommends maintaining adequate liquidity, avoiding leverage, and cultivating the emotional discipline to act when others are paralyzed by fear. He also suggests reviewing historical case studies to build confidence in the long-term resilience of quality businesses.

Recent market crises have tested the resolve of even the most seasoned investors. Smith’s perspective offers a roadmap for turning adversity into opportunity, emphasizing the importance of preparation, patience, and a focus on fundamentals. By viewing crises as a normal part of the investment landscape, rather than as existential threats, investors can build portfolios that are both resilient and opportunistic.

Practical Investment Strategies

- Prioritize Quality Over Price: Focus on companies with high returns on capital, strong competitive advantages, and consistent growth. Begin by screening for businesses with stable margins, robust cash flows, and low debt. Use metrics like return on equity (ROE), return on invested capital (ROIC), and free cash flow yield to identify quality. Avoid the temptation to buy mediocre companies just because they appear cheap; instead, be willing to “pay up” for sustainable excellence. Build a watchlist of global leaders in sectors with high barriers to entry and proven pricing power.

- Scrutinize Fund Fees and Manager Alignment: Before investing in any fund, carefully analyze the fee structure. Look for funds with low, transparent fees and avoid those with complex performance charges or hidden costs. Check whether fund managers have significant personal investments in their own funds (“skin in the game”), as this aligns their interests with yours. Use online tools or fund disclosures to compare fee levels and project their long-term impact on your returns. Don’t be swayed by marketing—focus on net returns after all costs.

- Beware of Complex or Synthetic Investment Products: When considering ETFs or other structured products, dig into the underlying mechanics. Avoid synthetic or leveraged ETFs unless you fully understand their risks, such as counterparty exposure and daily compounding effects. Favor physically-backed ETFs for core holdings, and always check for liquidity, tracking error, and transparency. Read the prospectus and seek independent reviews before investing in any complex product. Simplicity and transparency should be your guiding principles.

- Embrace Long-Term Compounding and Avoid Market Timing: Resist the urge to time the market or react emotionally to news headlines. Develop a disciplined investment process that focuses on holding quality companies through market cycles. Set clear criteria for buying and selling, such as deterioration in fundamentals or a significant overvaluation, rather than reacting to short-term price movements. Automate regular portfolio reviews and rebalancing, but avoid unnecessary trading. Remember that time in the market, not timing the market, is the key to compounding wealth.

- Analyze Capital Allocation Decisions: Evaluate how companies use their cash—whether through buybacks, dividends, or reinvestment. Favor management teams with a track record of rational, shareholder-friendly capital allocation. Review annual reports for details on buyback prices, dividend policies, and reinvestment returns. Be wary of buybacks that are primarily intended to boost executive compensation or cover up weak fundamentals. Use shareholder letters and earnings calls to assess management’s long-term vision and discipline.

- Prepare for Market Crises with a Playbook: Develop a plan for taking advantage of market downturns. Maintain a list of high-quality companies you’d like to own and set target prices based on intrinsic value. Keep a portion of your portfolio in cash or liquid assets to deploy during selloffs. Study past crises to build confidence in the resilience of quality businesses. When volatility strikes, review your playbook and act decisively, rather than succumbing to fear or inertia.

- Communicate and Document Your Investment Rationale: Whether managing your own portfolio or working with clients, adopt the habit of writing regular investment letters or memos. Clearly explain the reasoning behind major decisions, including buys, sells, and portfolio adjustments. Use data and specific examples to support your arguments. This practice not only builds trust but also enforces discipline and helps you learn from past mistakes. Transparency, both with yourself and others, is a key driver of long-term success.

- Question Investment Myths and Think Independently: Don’t accept conventional wisdom at face value. Critically evaluate the evidence behind popular strategies, such as passive investing, extreme diversification, or the pursuit of small-cap stocks. Be willing to concentrate your portfolio in your best ideas, provided they meet rigorous quality and valuation criteria. Continuously educate yourself, seek out diverse perspectives, and adapt your process as new information emerges. Independent thinking is your greatest asset in a crowded, often herd-driven market.

Modern Applications and Relevance

The principles outlined in “Investing for Growth” are more relevant than ever in today’s rapidly changing investment landscape. While the book was published in the wake of the COVID-19 pandemic and after a decade of bull markets, its core lessons have stood the test of multiple cycles, including the inflation shocks, tech bubbles, and financial crises that have shaped the modern era. Smith’s focus on quality, transparency, and long-term thinking provides a counterbalance to the short-termism and speculation that often dominate headlines.

Since the book’s publication, several trends have reinforced its message. The explosive growth of passive investing and ETFs has democratized access to markets but also introduced new risks, such as liquidity mismatches and the proliferation of complex synthetic products. Smith’s warnings about these dangers have proven prescient, as episodes of market stress—such as the March 2020 liquidity crunch—have exposed the vulnerabilities of certain ETF structures. Investors who heeded his advice to favor simplicity and transparency have been better positioned to navigate these challenges.

At the same time, the ongoing debate between value and growth investing has intensified, with many investors questioning whether it is still “safe to pay up for quality” in an era of high valuations and rapid technological change. Smith’s analysis, grounded in empirical evidence, demonstrates that quality companies continue to deliver superior returns over the long term, even in volatile or uncertain environments. The resilience of businesses with strong moats, robust cash flows, and disciplined management has been evident during recent downturns, reinforcing the book’s central thesis.

Modern examples abound. Companies like Microsoft, Adobe, and L’Oréal—cited by Smith—have continued to outperform broader indices, thanks to their ability to adapt, innovate, and compound capital. Meanwhile, the pitfalls of poor capital allocation, excessive leverage, and financial engineering have been on display in high-profile corporate failures and scandals. Smith’s emphasis on scrutinizing management incentives, understanding the true drivers of value, and maintaining a long-term horizon is as applicable today as it was a decade ago.

To adapt Smith’s classic advice to current conditions, investors should combine rigorous fundamental analysis with an awareness of new risks and opportunities. This means not only focusing on quality and valuation but also staying abreast of technological disruption, regulatory changes, and evolving market structures. The tools and data available to investors have never been more powerful, but the need for independent thinking, discipline, and skepticism remains paramount. “Investing for Growth” provides a timeless framework that can be tailored to any market environment, making it an indispensable resource for modern investors.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Implementation Guide

- Define Your Investment Universe and Criteria: Start by identifying the characteristics of quality companies you want in your portfolio. Use specific metrics such as return on capital employed (ROCE), consistent revenue and earnings growth, low debt-to-equity ratios, and strong free cash flow generation. Screen for companies with durable competitive advantages, such as brand strength, network effects, or regulatory moats. Document your criteria and create a watchlist of global leaders in industries with high barriers to entry.

- Conduct Deep Fundamental Analysis: Allocate time to thoroughly analyze each company on your watchlist. Review annual reports, earnings calls, and management commentary to assess business model resilience and capital allocation discipline. Compare historical performance to industry peers and look for evidence of pricing power, innovation, and adaptability. Set aside several weeks for this research phase to ensure you understand each company’s strengths, weaknesses, and long-term prospects.

- Construct a Concentrated, High-Conviction Portfolio: Build your portfolio around your best ideas, focusing on 15–30 stocks that meet your quality and valuation criteria. Allocate capital based on conviction level, business quality, and risk profile, rather than simply equal-weighting. Consider diversifying across industries and geographies, but avoid over-diversification that dilutes your best ideas. Use target position sizes and maximum allocation limits to manage risk while maintaining focus.

- Establish a Disciplined Review and Rebalancing Schedule: Set a regular schedule—such as quarterly or semi-annual reviews—to assess portfolio performance, monitor company fundamentals, and make adjustments as needed. Use this time to revisit your investment thesis for each holding, check for changes in management quality or capital allocation, and rebalance positions if necessary. Avoid reacting to short-term market noise; instead, let data and fundamentals guide your decisions.

- Document Decisions and Communicate Rationale: Keep detailed records of your investment decisions, including the reasoning behind each buy, sell, or hold. Write periodic memos or letters to yourself (or clients) explaining portfolio changes, performance drivers, and lessons learned. Use data, charts, and examples to support your arguments. This discipline fosters accountability, helps you learn from mistakes, and builds confidence in your process.

- Prepare a Crisis Playbook and Maintain Liquidity: Anticipate future market downturns by having a plan for deploying capital during periods of volatility. Maintain a watchlist of target companies with pre-set buy prices based on intrinsic value. Keep a portion of your portfolio in cash or highly liquid assets to act quickly when opportunities arise. Review your playbook at least annually and update it based on new information or changes in market conditions.

- Continuously Educate Yourself and Challenge Assumptions: Stay abreast of new research, industry trends, and evolving best practices. Read widely—books, shareholder letters, academic papers—and seek out diverse perspectives. Regularly revisit your investment philosophy and criteria, updating them as you gain experience or as markets evolve. Use platforms like Value Sense to access research tools, screen for undervalued stocks, and benchmark your process.

--- ---

10+ Free intrinsic value tools

For investors looking to find a stock's fair value, our analytics team has you covered with intrinsic value tools:

📍 Free Intrinsic Value Calculator

📍 Reverse DCF & DCF value tools

📍 Peter Lynch Fair Value Calculator

📍 Ben Graham Fair Value Calculator

📍 Relative Value tool

...and plenty more.

🔍 Explore all these tools for free on the Value Sense platform and start discovering what your favorite stocks are really worth.

FAQ: Common Questions About Investing for Growth: How to make money by only buying the best companies in the world

1. What is Terry Smith’s core investment philosophy in “Investing for Growth”?

Terry Smith’s philosophy centers on buying and holding shares in high-quality companies with strong competitive advantages, high returns on capital, and consistent growth. He advocates for a disciplined, long-term approach that prioritizes business fundamentals over short-term market movements. Smith believes that paying a premium for quality is justified, as these companies can compound returns over time. His approach rejects market timing and unnecessary complexity, focusing instead on transparency and simplicity.

2. How does the book critique traditional fund management practices?

Smith is highly critical of the traditional fund management industry, particularly its fee structures and lack of alignment with investors. He exposes how high management and performance fees erode returns, and how many fund managers fail to invest their own capital alongside clients. The book calls for greater transparency, lower costs, and meaningful co-investment by managers. Smith’s arguments are supported by data and real-world examples, encouraging investors to scrutinize the funds they choose.

3. What lessons does the book draw from historical market events and crises?

The book uses case studies such as the Wall Street Crash and the Global Financial Crisis to highlight recurring patterns of speculation, leverage, and investor psychology. Smith argues that market crises are inevitable but can present valuable opportunities for disciplined investors. He emphasizes the importance of maintaining a long-term perspective, avoiding excessive leverage, and focusing on business fundamentals. These lessons are reinforced with historical data and practical advice for navigating volatility.

4. How should investors approach share buybacks and capital allocation, according to Smith?

Smith recommends evaluating share buybacks on a case-by-case basis, favoring those conducted at prices below intrinsic value and funded by genuine excess cash. He warns against buybacks driven by management incentives or financial engineering. The book also stresses the importance of rational capital allocation, transparent accounting, and shareholder-friendly management. Investors should review company disclosures and management track records to assess the quality of capital allocation decisions.

5. Is it still relevant to “pay up for quality” in today’s markets?

According to Smith, paying a premium for high-quality companies remains a sound strategy, even in today’s markets. He provides evidence that quality businesses with durable competitive advantages continue to outperform over the long term, despite periods of high valuations or market volatility. The key is to focus on intrinsic value, growth prospects, and management quality, rather than being fixated on short-term price multiples. Smith’s framework is adaptable to modern market conditions and remains highly relevant for investors seeking sustainable growth.