Prem Watsa - Fairfax Financial Holdings Portfolio in 2026: Top Holdings & Recent Changes

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

Prem Watsa, the legendary Canadian investor and CEO of Fairfax Financial Holdings, continues to demonstrate why patient capital and contrarian conviction define his investment philosophy. His Q3 2025 portfolio reveals a masterclass in concentrated value investing, with $2.06 billion deployed across just 29 carefully selected positions that reflect his signature approach of finding deeply undervalued assets others overlook. The portfolio's composition tells a compelling story: heavy exposure to energy and commodities, strategic healthcare positions, and a willingness to hold unpopular stocks when fundamentals justify the conviction.

Portfolio Overview: Ultra-Concentrated Excellence in Contrarian Investing

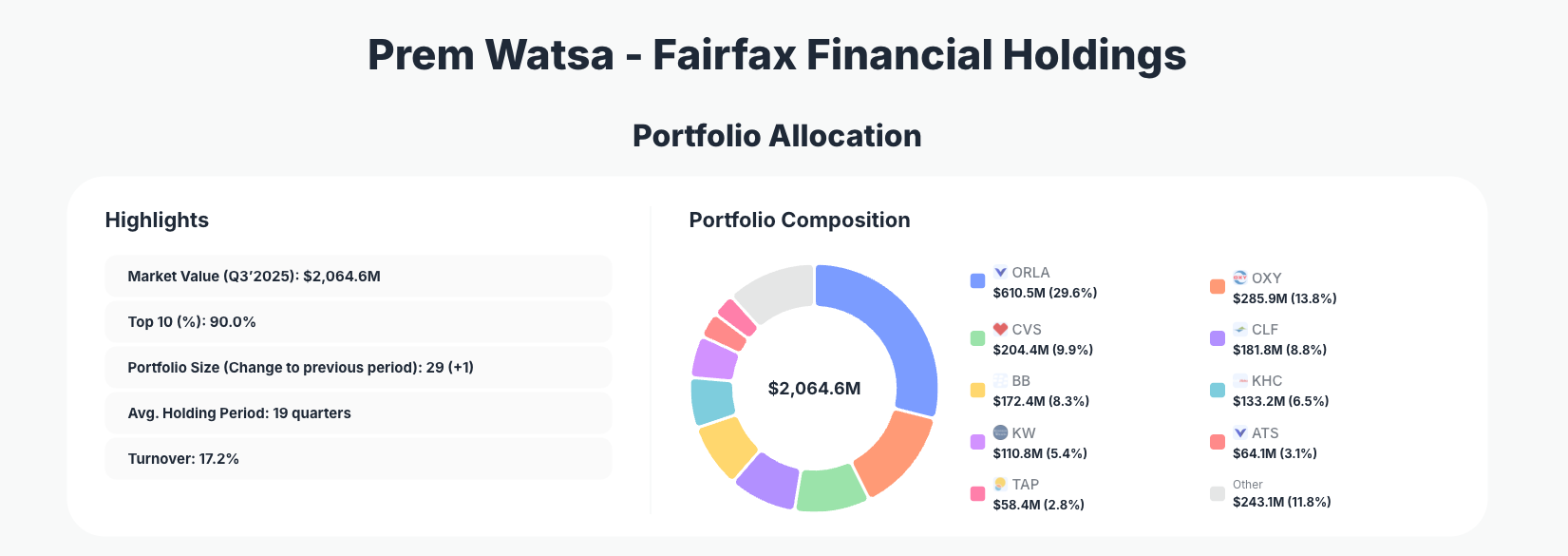

Portfolio Highlights (Q3 2025): - Market Value: $2,064.6M - Top 10 Holdings: 90.0% - Portfolio Size: 29 positions (+1 new addition) - Average Holding Period: 19 quarters (4.75 years) - Turnover: 17.2%

Fairfax Financial's portfolio exemplifies the power of concentrated conviction investing. With 90% of assets in the top 10 holdings, Watsa demonstrates absolute confidence in his thesis—a hallmark of his investment approach that has generated exceptional long-term returns. The 19-quarter average holding period reveals a patient investor who buys and holds through market cycles, resisting the temptation to chase short-term trends. This is not a portfolio built on quarterly momentum; it's constructed for multi-year wealth creation.

The modest 17.2% turnover rate indicates disciplined capital allocation. Rather than constantly trading, Watsa makes deliberate adjustments when conviction changes or opportunities emerge. The addition of one new position in Q3 2025 suggests selective deployment of capital into what he perceives as exceptional value opportunities. This measured approach to portfolio management reflects decades of experience navigating market cycles and understanding the difference between price and value.

Top Holdings Analysis: Energy Dominance and Selective Value Plays

The portfolio is anchored by Orla Mining Ltd at 29.6%, Watsa's largest conviction position and a clear signal of his bullish stance on precious metals and mining. Occidental Petroleum 13.8% remains unchanged, reflecting unwavering confidence in energy sector fundamentals despite market volatility. CVS Health 9.9% represents his healthcare exposure, a defensive position in a portfolio otherwise tilted toward cyclical assets.

Cleveland-Cliffs Inc. 8.8% rounds out the top four, providing additional exposure to commodities and industrial metals. However, the most significant recent move comes with BlackBerry Limited 8.3%, which saw a 13.21% reduction—a notable signal that Watsa is trimming exposure to this long-held position, though maintaining substantial conviction with over 8% of the portfolio still allocated.

The Kraft Heinz Company 6.5% received a 4.81% addition, suggesting Watsa sees further value in this consumer staples turnaround story. Kennedy-Wilson Holdings 5.4% remains a steady position in real estate and alternative investments. ATS Corporation 3.1% provides exposure to automation and industrial technology.

The portfolio's smaller positions reveal opportunistic moves: Molson Coors Beverage Company 2.8% received a 5.87% addition, indicating increased conviction in this dividend-paying consumer staple. Helmerich & Payne Inc. 1.3% saw a significant 20.53% addition, signaling aggressive deployment into oil services. Pfizer Inc. 1.1% received a 36.87% boost, suggesting Watsa sees pharmaceutical value at current prices. New positions in Lululemon Athletica Inc. and Dollar Tree, Inc. represent selective entry into consumer discretionary and discount retail, while a minor reduction in Garrett Motion Inc. 0.2% shows portfolio maintenance.

What the Portfolio Reveals About Watsa's Current Strategy

Prem Watsa's Q3 2025 positioning reveals several critical investment themes:

Energy and Commodities Conviction: With nearly 50% of the portfolio in energy, mining, and commodity-related positions, Watsa is making a bold bet on inflation, geopolitical tensions, and structural supply constraints. This is a contrarian stance when many investors have rotated toward technology and growth.

Selective Value in Consumer Staples: The additions to Kraft Heinz, Molson Coors, and Dollar Tree suggest Watsa sees exceptional value in beaten-down consumer companies trading below intrinsic value. These are businesses with pricing power, established brands, and cash generation—precisely what value investors seek.

Healthcare Rebalancing: The Pfizer addition and CVS holding indicate confidence in healthcare valuations, particularly in pharmaceutical and pharmacy retail sectors that have faced regulatory and competitive pressures.

Disciplined Trimming: The 13.21% reduction in BlackBerry, while maintaining an 8.3% position, demonstrates Watsa's willingness to take profits and rebalance when positions become overweight—a sign of mature portfolio management.

Opportunistic Deployment: New positions in Lululemon and Dollar Tree, combined with the Helmerich & Payne surge, show Watsa actively deploying capital into what he perceives as exceptional opportunities across consumer and energy sectors.

Portfolio Concentration Analysis

| Position | Value | % of Portfolio | Recent Change |

|---|---|---|---|

| Orla Mining Ltd | $610.5M | 29.6% | No change |

| Occidental Petroleum | $285.9M | 13.8% | No change |

| CVS Health Corporation | $204.4M | 9.9% | No change |

| Cleveland-Cliffs Inc. | $181.8M | 8.8% | No change |

| BlackBerry Limited | $172.4M | 8.3% | Reduce 13.21% |

| The Kraft Heinz Company | $133.2M | 6.5% | Add 4.81% |

| Kennedy-Wilson Holdings | $110.8M | 5.4% | No change |

| ATS Corporation | $64.1M | 3.1% | No change |

| Molson Coors Beverage Company | $58.4M | 2.8% | Add 5.87% |

| Vanguard Index Funds | $35.7M | 1.7% | Reduce 20.10% |

The concentration metrics reveal a portfolio structure that demands absolute conviction. The top 10 holdings representing 90% of assets means that Watsa's returns are entirely dependent on the performance of these core positions. This is not a diversified approach—it's a concentrated bet on his ability to identify undervalued assets.

The Orla Mining position at nearly 30% is particularly noteworthy. This represents Watsa's largest single conviction, suggesting he believes precious metals and mining equities offer exceptional value. The stability of his top four positions (Orla, Occidental, CVS, Cleveland-Cliffs) indicates these are core holdings unlikely to be sold absent fundamental deterioration.

The reduction in Vanguard Index Funds by 20.10% is telling: Watsa is rotating away from passive index exposure toward active stock picking, a clear signal of confidence in his ability to outperform through security selection.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Investment Lessons from Prem Watsa's Contrarian Approach

Watsa's portfolio offers several timeless investment principles:

Concentration Requires Conviction: Holding 90% of assets in 10 positions demands deep research and absolute confidence. Watsa doesn't diversify for comfort—he concentrates capital where he sees the greatest opportunity. This approach generates superior returns but requires the discipline to resist panic selling during downturns.

Patient Capital Wins: The 19-quarter average holding period demonstrates that Watsa buys and holds through market cycles. He's not trading quarterly earnings surprises; he's investing in businesses trading below intrinsic value and waiting for the market to recognize that value.

Contrarian Positioning Pays: When most investors fled energy and commodities, Watsa doubled down. When consumer staples faced headwinds, he added to positions. Contrarian investing requires the courage to act when sentiment is negative and valuations are depressed.

Rebalancing Discipline: The BlackBerry reduction and Vanguard trimming show Watsa actively manages position sizing. As positions appreciate or circumstances change, he rebalances to maintain portfolio discipline and lock in gains.

Opportunistic Deployment: Rather than deploying capital continuously, Watsa waits for exceptional opportunities. The new positions in Lululemon and Dollar Tree, combined with the Helmerich & Payne surge, show capital being deployed selectively into what he perceives as exceptional value.

Quality Matters: Despite the value focus, Watsa's holdings are predominantly quality businesses—Occidental Petroleum, CVS Health, Kraft Heinz, Molson Coors. He's not buying distressed junk; he's buying quality companies trading at distressed valuations.

Looking Ahead: What Comes Next?

Fairfax Financial's positioning sets up the portfolio for several potential scenarios:

Energy Upside: With nearly 50% in energy and commodities, Watsa is positioned to benefit significantly if geopolitical tensions, supply constraints, or inflation drive energy prices higher. The Helmerich & Payne addition suggests he's building exposure to oil services ahead of potential demand acceleration.

Consumer Staples Recovery: The additions to Kraft Heinz, Molson Coors, and Dollar Tree position the portfolio to benefit from a consumer staples rebound if these companies successfully navigate inflationary pressures and demonstrate pricing power.

Healthcare Opportunity: The Pfizer addition and CVS holding suggest Watsa sees pharmaceutical and pharmacy valuations as attractive, potentially positioning for a healthcare sector rotation.

Selective Deployment: With 17.2% turnover and the addition of new positions, Watsa appears to be actively deploying capital. The question for investors is whether he has identified additional exceptional opportunities that will drive future additions.

Inflation Hedge: The portfolio's heavy weighting toward commodities, energy, and real estate (Kennedy-Wilson) suggests Watsa is positioning for an inflationary environment where hard assets and pricing power matter.

FAQ About Prem Watsa's Fairfax Financial Portfolio

Q: Why did Watsa reduce BlackBerry by 13.21% if he still holds 8.3% of the portfolio?

A: The reduction signals that while Watsa maintains conviction in BlackBerry's long-term value, the position had become overweight relative to his target allocation. This is disciplined rebalancing—taking some profits while maintaining exposure to a position he still believes in. It's a nuanced move that shows portfolio management sophistication.

Q: What does the 90% concentration in top 10 holdings tell us about Watsa's confidence?

A: This extreme concentration reflects absolute conviction in his research and stock-picking ability. Watsa isn't diversifying for comfort; he's concentrating capital where he sees the greatest opportunity. This approach generates superior returns during bull markets but requires the discipline to hold through downturns. It's a strategy only suitable for investors with high conviction and long time horizons.

Q: Why is Watsa adding to energy and commodities when many investors are rotating away?

A: Watsa is a contrarian investor who buys when sentiment is negative and valuations are depressed. His energy and commodities positioning suggests he believes these sectors are undervalued relative to long-term fundamentals. Whether driven by inflation expectations, geopolitical concerns, or supply constraints, Watsa sees value where others see risk.

Q: How should retail investors use this portfolio information?

A: While you shouldn't blindly copy Watsa's holdings, his portfolio offers valuable lessons about value investing discipline. Track his moves through ValueSense's superinvestor tracker, which updates quarterly based on 13F filings. Note that 13F filings have a 45-day reporting lag, so positions may have changed since the filing date. Use Watsa's portfolio as a research starting point—investigate why he owns these positions and whether the thesis applies to your investment goals.

Q: What's the significance of the new positions in Lululemon and Dollar Tree?

A: These additions suggest Watsa sees exceptional value in consumer discretionary and discount retail. Lululemon represents premium consumer discretionary, while Dollar Tree represents value retail. Together, they suggest Watsa is finding opportunities across the consumer spectrum, likely driven by valuation rather than sector rotation.

Q: How does Watsa's 19-quarter holding period compare to typical investors?

A: The 19-quarter (4.75-year) average holding period is extraordinarily long, reflecting Watsa's buy-and-hold philosophy. Most active investors turn over portfolios annually or faster. Watsa's approach demonstrates that patient capital—buying undervalued businesses and holding through market cycles—is a superior wealth-creation strategy. This requires the discipline to resist trading on short-term noise and the conviction to hold through volatility.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2026)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!