Seth Klarman - Baupost Group Portfolio in 2026: Top Holdings & Recent Changes

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

Seth Klarman, founder and CEO of Baupost Group, continues to demonstrate why he's regarded as one of the most disciplined value investors of our time. His Q4 2025 portfolio reveals a masterclass in selective investing, with $5.3 billion deployed across just 22 carefully chosen positions that reflect his signature distressed-value approach. The quarter showcased significant portfolio repositioning, with Klarman making bold moves in both established positions and new opportunities—most notably a dramatic 120% addition to Amazon while simultaneously trimming his massive Alphabet stake by 41.49%.

Portfolio Overview: Concentrated Value with Surgical Precision

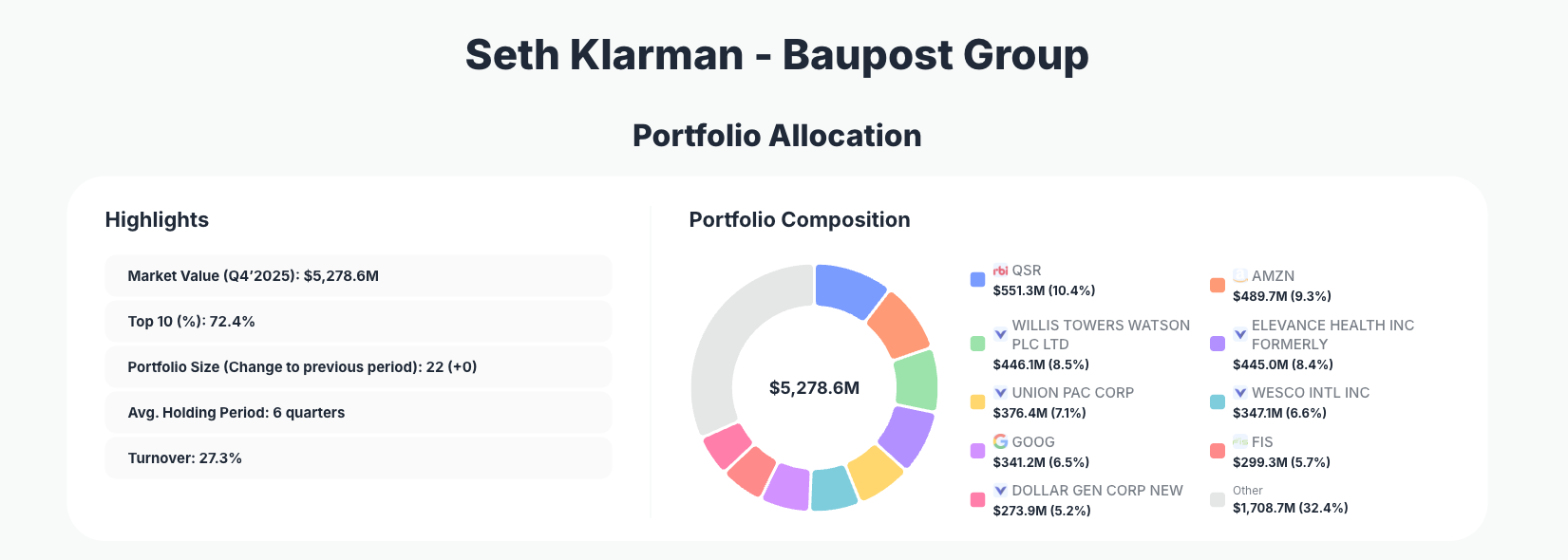

Portfolio Highlights (Q4 2025): - Market Value: $5,278.6M - Top 10 Holdings: 72.4% - Portfolio Size: 22 positions - Average Holding Period: 6 quarters - Turnover: 27.3%

Baupost's portfolio concentration tells a compelling story about Klarman's conviction in his selections. With the top 10 holdings representing 72.4% of the portfolio, this is not a fund spreading capital thinly across dozens of positions. Instead, it reflects the disciplined approach of a manager who invests heavily only when he identifies genuine value disconnects from market pricing. The 27.3% turnover rate indicates moderate activity—Klarman isn't a day trader, but he's also not afraid to make significant adjustments when market conditions or company fundamentals shift.

The portfolio's 6-quarter average holding period demonstrates Klarman's patience with his investments. This isn't a strategy built on short-term momentum or quarterly earnings surprises. Rather, it reflects a deep-value philosophy where positions are held long enough for the market to recognize the intrinsic value that Baupost identified at entry. The fact that the portfolio size remained flat at 22 positions quarter-over-quarter suggests Klarman is being highly selective about new capital deployment, preferring to optimize existing positions rather than chase new opportunities indiscriminately.

Strategic Holdings: Where Klarman is Placing His Bets

The portfolio is anchored by Restaurant Brands International at 10.4% $551.3M, though Klarman made a modest 2.09% reduction, suggesting slight profit-taking or rebalancing rather than a loss of conviction. The most dramatic move came with Amazon, which received a stunning 120.07% addition to reach 9.3% of the portfolio $489.7M—a clear signal that Klarman sees compelling value in the e-commerce and cloud computing giant at current levels.

Willis Towers Watson 8.5% received a 24.66% boost, indicating growing confidence in the insurance and benefits consulting firm. Elevance Health 8.4% saw a modest 3.77% reduction despite remaining a core holding, while Union Pacific 7.1% was increased by 8.76%, reflecting Klarman's continued belief in railroad infrastructure plays. Wesco International 6.6% experienced a 5.61% trim, suggesting some profit-taking on what may have been a successful position.

The most notable reduction came in Alphabet, which was cut by 41.49% to 6.5% $341.2M. This dramatic move signals either that Klarman believes the stock has become fairly valued after recent gains, or that he's reallocating capital to what he perceives as more attractive opportunities. Fidelity National Information Services 5.7% received an 18.84% addition, showing increased conviction in the financial services technology provider. Dollar General 5.2% was trimmed by 22.65%, suggesting Klarman may be concerned about the discount retailer's valuation or competitive positioning. Finally, Ferguson 4.8% saw a minor 1.60% reduction.

What the Portfolio Reveals About Baupost's Strategy

Several key themes emerge from Klarman's Q4 positioning:

Selective Tech Exposure with Discipline: Rather than avoiding technology entirely, Klarman is carefully selecting tech positions where he sees value. The massive Amazon addition combined with the Alphabet reduction suggests he's distinguishing between different tech narratives—favoring Amazon's diversified revenue streams and cloud dominance while becoming more cautious on Alphabet's valuation.

Infrastructure and Defensive Positioning: The continued emphasis on Union Pacific and the addition to Willis Towers Watson reflect a preference for essential services and infrastructure plays that generate steady cash flows regardless of economic cycles.

Retail and Consumer Selectivity: Holdings in Restaurant Brands and the reduction in Dollar General suggest Klarman is being highly selective in consumer-facing businesses, likely favoring those with strong brand moats and pricing power.

Financial Services Conviction: Multiple positions in financial services (Willis Towers Watson, Fidelity National Information Services, Elevance Health) indicate Klarman sees value in this sector, potentially betting on higher interest rates and financial system stability.

Active Rebalancing: The 27.3% turnover and significant position adjustments show this isn't a "set and forget" portfolio. Klarman is actively managing positions as valuations shift and opportunities emerge.

Portfolio Concentration Analysis

| Position | Value | % of Portfolio | Recent Change |

|---|---|---|---|

| Restaurant Brands International | $551.3M | 10.4% | Reduce 2.09% |

| Amazon.com | $489.7M | 9.3% | Add 120.07% |

| Willis Towers Watson | $446.1M | 8.5% | Add 24.66% |

| Elevance Health | $445.0M | 8.4% | Reduce 3.77% |

| Union Pacific | $376.4M | 7.1% | Add 8.76% |

| Wesco International | $347.1M | 6.6% | Reduce 5.61% |

| Alphabet Inc. | $341.2M | 6.5% | Reduce 41.49% |

| Fidelity National Information Services | $299.3M | 5.7% | Add 18.84% |

| Dollar General | $273.9M | 5.2% | Reduce 22.65% |

| Ferguson | $253.1M | 4.8% | Reduce 1.60% |

The concentration metrics reveal a portfolio built on conviction rather than diversification for its own sake. The top 10 holdings at 72.4% means that Klarman's success or failure is heavily dependent on getting these 10 positions right. This is not a strategy for the faint of heart, but it reflects the confidence of a manager who has spent decades identifying value opportunities that others miss.

The quarter-over-quarter changes show active management: five positions received additions (Amazon, Willis Towers Watson, Union Pacific, Fidelity National Information Services, and implicitly others outside the top 10), while five received reductions (Restaurant Brands, Elevance Health, Wesco International, Alphabet, Dollar General, Ferguson). This balanced approach to adjustments suggests Klarman is neither aggressively expanding nor contracting overall exposure—rather, he's optimizing the portfolio's composition based on changing valuations and opportunities.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Investment Lessons from Seth Klarman's Approach

Conviction Requires Concentration: Klarman's willingness to place 10.4% of his portfolio in a single position (Restaurant Brands) demonstrates that true value investors don't fear concentration when they've done their homework. This runs counter to modern portfolio theory's emphasis on diversification, but it reflects the reality that deep research and conviction should be rewarded with meaningful position sizes.

Valuation Discipline Trumps Narrative: The 41.49% reduction in Alphabet despite its strong business fundamentals suggests Klarman prioritizes valuation over growth narratives. When a stock becomes fairly valued or expensive, even a quality business gets trimmed. This discipline prevents the trap of "falling in love" with positions.

Patience Pays Off: The 6-quarter average holding period shows Klarman isn't trying to time the market or chase quarterly performance. He's willing to hold positions long enough for the market to recognize the value he identified, which reduces trading costs and taxes while allowing compounding to work.

Active Rebalancing Captures Value: The 27.3% turnover demonstrates that value investing isn't passive. As positions appreciate and valuations shift, Klarman actively rebalances—taking profits on winners and redeploying capital to new opportunities. This disciplined rebalancing is a key source of alpha.

Sector Rotation Within Value Framework: Rather than being locked into specific sectors, Klarman rotates capital based on where he sees the best risk-reward. The Amazon addition and Alphabet reduction show he's willing to shift within technology based on valuation, not ideology.

Quality Matters: Even within a value framework, Klarman's holdings tend to be quality businesses with strong competitive positions (Amazon, Willis Towers Watson, Union Pacific). This "quality value" approach avoids the trap of catching falling knives in genuinely deteriorating businesses.

Looking Ahead: What Comes Next?

With $5.3 billion deployed across 22 positions and a 27.3% turnover rate, Baupost appears to have meaningful dry powder for new opportunities. The dramatic Amazon addition suggests Klarman identified a compelling entry point, but the question remains: where does he deploy additional capital in 2026?

Several factors will likely shape Baupost's positioning going forward:

Interest Rate Environment: Klarman's historical preference for distressed situations and special situations means he benefits from market dislocations. If interest rates remain elevated or rise further, opportunities in stressed credit and restructuring situations may emerge.

Technology Valuation Normalization: The Alphabet reduction and Amazon addition suggest Klarman is carefully parsing the technology sector. If valuations continue to compress, he may find additional opportunities in quality tech businesses trading at reasonable multiples.

Macro Uncertainty: Baupost's history of thriving during market dislocations suggests Klarman may be positioning for potential volatility. The relatively flat portfolio size and moderate turnover could indicate he's maintaining flexibility to act quickly if opportunities emerge.

Sector Rotation: The emphasis on financial services, infrastructure, and selective consumer plays suggests Klarman is positioning for an environment where steady cash flows and pricing power matter more than growth-at-any-price narratives.

FAQ About Seth Klarman's Baupost Portfolio

Q: Why did Klarman add 120% to Amazon in Q4 2025?

A: The dramatic Amazon addition signals that Klarman identified compelling value at current price levels. This could reflect his assessment that the market was undervaluing Amazon's cloud computing growth, e-commerce dominance, or advertising business. For value investors like Klarman, such large additions typically indicate a significant valuation disconnect—the stock was trading below his calculated intrinsic value by a meaningful margin.

Q: What does the 41.49% reduction in Alphabet mean?

A: This substantial trim likely indicates that Klarman believes Alphabet has become fairly valued or expensive relative to his intrinsic value estimates. It doesn't necessarily mean he's bearish on Google's business—rather, it suggests the risk-reward has shifted unfavorably. This is classic value investing discipline: sell when valuations become stretched, regardless of business quality.

Q: How can I track Baupost's portfolio changes?

A: ValueSense provides real-time tracking of Baupost's 13F filings, which are required quarterly disclosures of large equity positions. Note that 13F filings have a 45-day reporting lag, meaning the positions disclosed in Q4 2025 filings were actually held as of December 31, 2025. ValueSense's platform makes it easy to monitor these changes and compare them to previous quarters, helping you understand Klarman's evolving strategy.

Q: Is Baupost's portfolio suitable for retail investors to copy?

A: While Klarman's investment principles—focusing on intrinsic value, maintaining discipline, and avoiding overpaying—are universally applicable, directly copying his portfolio has limitations. Baupost has advantages retail investors lack: access to distressed debt, special situations, and private investments not available to the general public. Additionally, Klarman's deep research capabilities and decades of experience mean he can identify value others miss. Instead of copying positions, retail investors should study his methodology: how he analyzes businesses, calculates intrinsic value, and maintains discipline around valuation.

Q: What's the significance of the 72.4% concentration in the top 10 holdings?

A: This high concentration reflects Klarman's conviction in his research and analysis. Rather than spreading capital across 50+ positions, he concentrates in his best ideas. This approach works for skilled investors who can identify genuine value opportunities, but it also means portfolio performance is heavily dependent on these 10 positions performing as expected. For retail investors, this suggests the importance of position sizing based on conviction—your largest positions should be in your highest-conviction ideas where you've done the most thorough analysis.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2026)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!