The Essays of Warren Buffett: Lessons for Corporate America by Warren E. Buffett, Lawrence A. Cunningham

Welcome to the Value Sense Blog, your resource for insights on the stock market! You're reading a book review written by the valuesense.io team.

On our platform, you'll find stock research and insights across all sectors. Dive into our research products and learn more about our unique approach at valuesense.io

We offer over 360+ automated stock ideas, a free AI-powered stock screener, interactive stock charting tools, and more than 10 intrinsic value models — all designed to help investors find undervalued growth opportunities.

Book Overview

Few names in the world of investing command as much respect and admiration as Warren Buffett. “The Essays of Warren Buffett: Lessons for Corporate America,” compiled and expertly edited by Lawrence A. Cunningham, offers an unparalleled window into the mind of the Oracle of Omaha. Buffett, the legendary chairman and CEO of Berkshire Hathaway, is renowned not only for his extraordinary investment track record but also for his clarity of thought and plainspoken wisdom. Cunningham, a respected law professor and corporate governance expert, has meticulously curated Buffett’s annual shareholder letters—transforming them into a cohesive guide for investors, managers, and students of finance.

The book was first published in the mid-1990s, a period marked by the tail end of a long bull market, the rise of technology stocks, and the beginnings of a shift in corporate governance standards. Since then, the book has seen several updated editions, each incorporating Buffett’s evolving thoughts as the markets and business landscape have changed. The historical context is vital: Buffett’s principles, forged over decades, have weathered multiple financial crises, bubbles, and paradigm shifts, providing a timeless framework for investment and corporate stewardship.

At its core, “The Essays of Warren Buffett” is more than just an investment manual. It is a treatise on rationality, integrity, and the enduring value of sound judgment. The book’s main theme revolves around the alignment of shareholder and management interests, the pursuit of intrinsic value, and the necessity of transparent, ethical governance. Buffett’s writing demystifies complex financial concepts, making them accessible to both seasoned professionals and novices. Through anecdotes, case studies, and clear logic, he stresses the importance of patience, discipline, and a long-term perspective.

This book is considered a classic for several reasons. First, it distills decades of practical wisdom from one of history’s greatest investors. Second, it bridges the gap between high finance and common sense, offering readers actionable lessons that are as relevant today as when they were first penned. The book’s enduring popularity stems from its unique blend of wit, humility, and deep insight into both markets and human nature. It is a must-read for investors seeking to understand not just how to make money, but how to think about money, risk, and business itself.

What sets this book apart from other investment classics is its structure and perspective. Rather than presenting a rigid, step-by-step formula, it offers a mosaic of essays organized by theme—corporate governance, investing, valuation, accounting, and more. Each essay is a standalone lesson, yet together they form a comprehensive philosophy that has shaped generations of investors. Whether you are a portfolio manager, a corporate executive, a student, or a business owner, Buffett’s essays provide a blueprint for navigating the complexities of finance with integrity and intelligence.

Key Themes and Concepts

Throughout “The Essays of Warren Buffett,” several powerful themes emerge, weaving together the lessons that have defined Buffett’s career. Rather than offering a linear, chapter-by-chapter narrative, the book presents a tapestry of interconnected ideas—each reinforcing the others and providing a holistic approach to investing and business management. The recurring motifs are not only theoretical but deeply practical, offering readers a robust toolkit for navigating real-world investment challenges.

Buffett’s essays are grounded in a philosophy that values rationality over speculation, stewardship over self-interest, and substance over form. The book’s central themes include the alignment of management and shareholder interests, the pursuit of intrinsic value, the importance of understanding risk, and the necessity of sound accounting and governance. Each theme is illustrated with vivid examples, historical anecdotes, and actionable advice, making the lessons both memorable and immediately applicable.

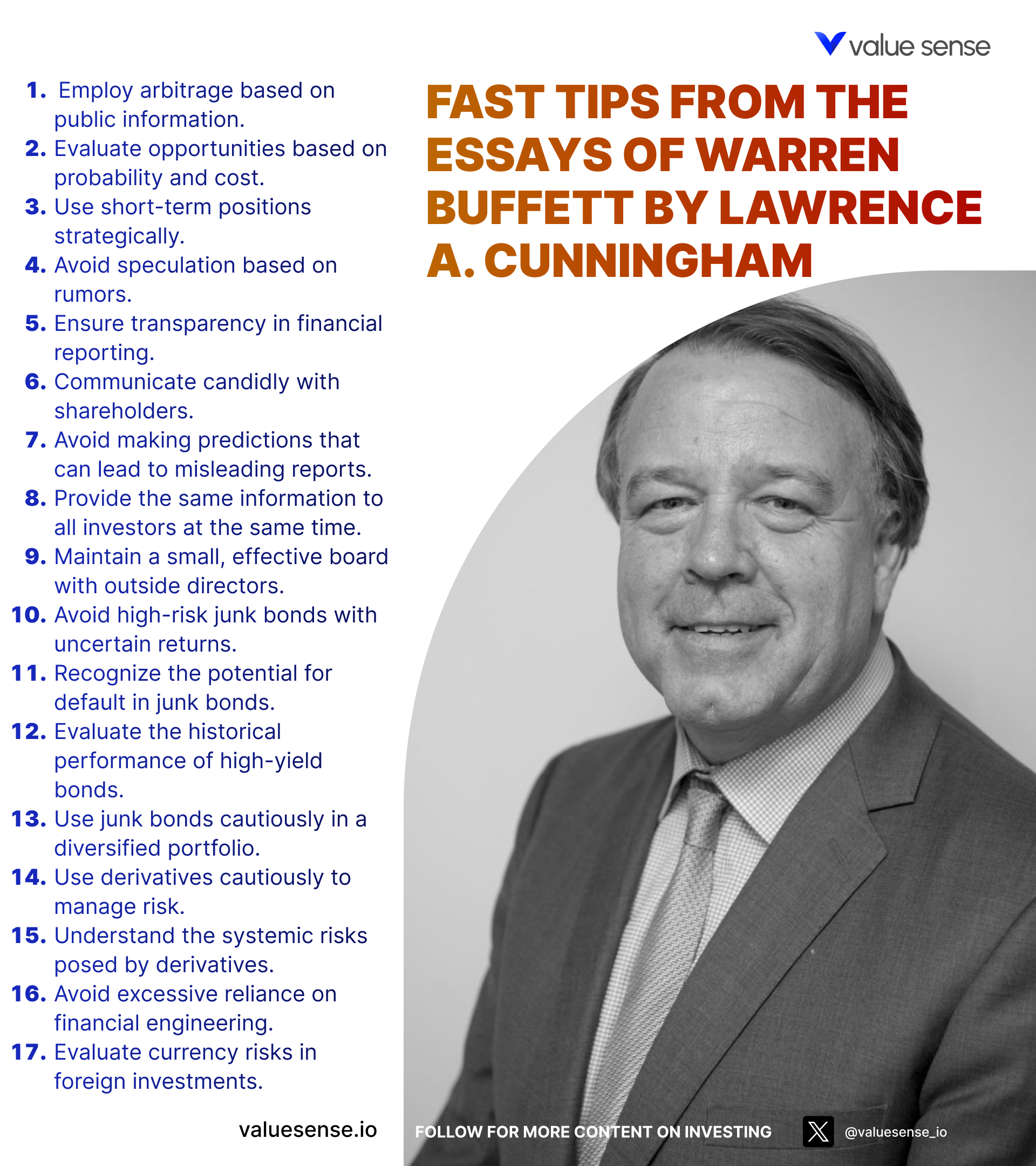

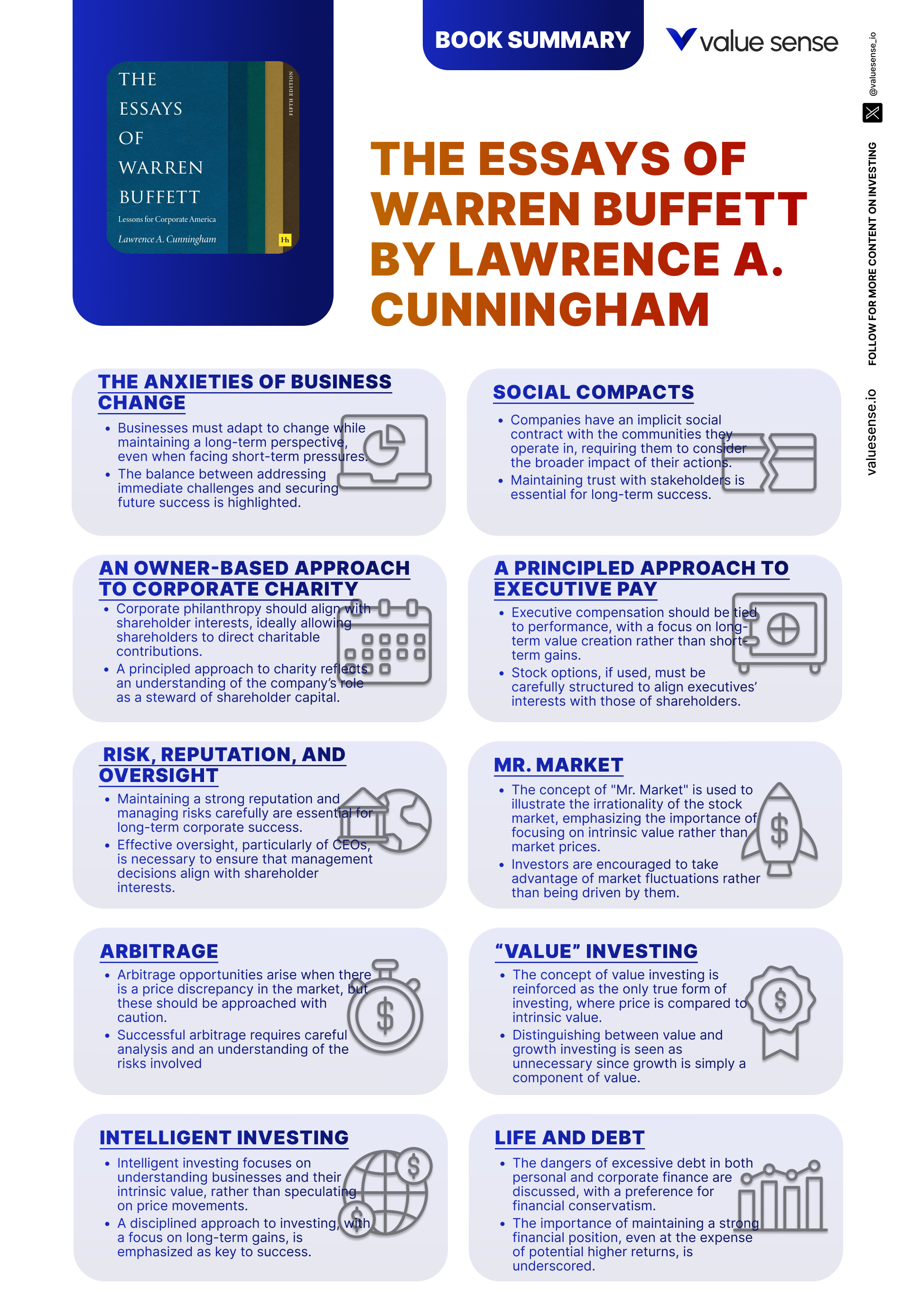

- Corporate Governance and Stewardship: One of the book’s foundational themes is the role of corporate managers as stewards of shareholder capital. Buffett argues that CEOs and boards must act with candor, integrity, and a long-term perspective. He criticizes selective disclosure and short-termism, advocating for transparent communication and alignment of management incentives with shareholder interests. For example, Buffett discusses his own approach at Berkshire Hathaway, where compensation is tied to long-term performance rather than quarterly earnings. This theme is highly relevant for investors evaluating management quality and for executives seeking to build lasting value.

- Value Investing and Intrinsic Value: At the heart of Buffett’s philosophy is the principle of value investing—buying businesses at prices below their intrinsic value. He emphasizes the importance of understanding what a business is truly worth, rather than being swayed by market sentiment or short-term price movements. The book explains how to estimate intrinsic value using owner earnings and discounted cash flows, and why a margin of safety is essential. Buffett’s famous analogy of “Mr. Market” underscores the folly of treating the stock market as a guide, rather than an opportunity provider. This theme equips investors with the mindset and tools to make rational, independent decisions.

- Investment Risk and Margin of Safety: Buffett challenges conventional notions of risk, arguing that true risk is not volatility but the possibility of permanent capital loss. He critiques the widespread use of beta and other statistical measures, instead urging investors to focus on business fundamentals, competitive advantages, and the sustainability of earnings. The margin of safety—buying with a sufficient cushion below intrinsic value—is presented as the cornerstone of prudent investing. Real-world examples, such as the collapse of over-leveraged companies, illustrate the dangers of ignoring these principles.

- Financial Instruments and Their Pitfalls: The book provides a sober analysis of various financial instruments, including junk bonds and derivatives. Buffett warns about the dangers of complexity, leverage, and misaligned incentives, drawing on historical episodes like the junk bond boom and the 2008 financial crisis. He explains why productive assets—businesses and real estate—tend to outperform speculative vehicles over time. This theme is crucial for investors navigating today’s landscape of increasingly complex financial products.

- Valuation Techniques and Owner Earnings: Buffett demystifies valuation by focusing on the economic realities of a business rather than accounting conventions. He introduces the concept of owner earnings as a superior measure of profitability, highlighting the limitations of traditional metrics like net income and EBITDA. The book explains how to distinguish between economic and accounting goodwill, and why cash flow analysis must account for reinvestment needs. These insights help investors avoid common pitfalls and make more informed decisions.

- Accounting Practices and Transparency: A recurring motif is the critique of traditional accounting practices that obscure economic reality. Buffett explains how aggressive accounting, selective disclosure, and off-balance-sheet maneuvers can mislead investors. He advocates for full and fair disclosure, clear reporting of owner earnings, and conservative accounting policies. This theme is vital for anyone seeking to analyze financial statements and assess the true health of a business.

- Long-Term Thinking and Rational Temperament: Perhaps the most pervasive theme is the importance of patience, discipline, and rationality. Buffett stresses that successful investing requires a temperament that can withstand market euphoria and panic, and a willingness to act independently of the crowd. He draws on psychological research, personal anecdotes, and historical market cycles to illustrate the power of long-term thinking. This theme is especially relevant in today’s fast-paced, information-saturated markets.

Book Structure: Major Sections

Part 1: Corporate Governance

This section, encompassing the first three chapters, lays the groundwork for Buffett’s philosophy on corporate governance. The unifying theme is the role of managers as stewards of shareholder capital and the critical importance of transparency, candor, and accountability in corporate communications. Buffett shares his views on what constitutes effective governance, the selection and evaluation of CEOs, and the pitfalls of misaligned incentives.

Key concepts from these chapters include the necessity of forthrightness in shareholder communications, the dangers of selective disclosure, and the importance of aligning management compensation with long-term value creation. Buffett provides detailed examples from Berkshire Hathaway’s own practices, such as his refusal to provide earnings guidance and his emphasis on honest, comprehensive annual letters. He also discusses the criteria for CEO selection, highlighting integrity, rationality, and a shareholder-oriented mindset as essential traits. The alignment of interests between shareholders and management is underscored as a prerequisite for sustained corporate success.

For investors, these insights translate into concrete evaluation criteria when analyzing companies: Is management transparent and candid in its communications? Are compensation structures designed to reward long-term performance? Is there evidence of alignment between management and shareholder interests? By applying these standards, investors can better assess the quality of corporate leadership and the likelihood of value creation over time.

In today’s environment of increased scrutiny on corporate behavior and governance, Buffett’s principles remain highly relevant. The emphasis on transparency, ethical leadership, and accountability is echoed in modern ESG (environmental, social, and governance) frameworks. Investors who internalize these lessons are better equipped to identify companies with sustainable competitive advantages and avoid those vulnerable to governance-related risks.

Part 2: Finance and Investing

Chapters 4, 5, and 6 are grouped under the theme of finance and investing, providing a deep dive into Buffett’s investment philosophy. This section critiques modern finance theory, particularly the efficient market hypothesis and the use of beta as a risk measure. Instead, Buffett advocates for value investing principles, emphasizing the importance of intrinsic value, the margin of safety, and understanding the psychological dynamics of markets.

Key concepts include the “Mr. Market” analogy, which personifies the market as an emotional partner offering to buy or sell shares at varying prices. Buffett encourages investors to take advantage of market fluctuations rather than being dictated by them. He stresses that investing is most intelligent when it is most businesslike, urging readers to focus on business fundamentals, sustainable competitive advantages, and reasonable valuations. The margin of safety is highlighted as the central tenet of value investing, protecting investors from errors in judgment and unforeseen events.

Investors can apply these lessons by developing a disciplined investment process centered on intrinsic value analysis. This involves estimating a company’s true worth based on future owner earnings, discounting them at an appropriate rate, and requiring a margin of safety before committing capital. By ignoring market noise and focusing on long-term value, investors can avoid common pitfalls such as panic selling or chasing speculative trends.

Buffett’s critique of modern finance theory remains pertinent in a world dominated by algorithmic trading, passive investing, and short-term speculation. The principles of value investing—patience, discipline, and independent thinking—are as relevant today as ever. By adopting Buffett’s approach, investors can navigate volatile markets with confidence and clarity.

Part 3: Investment Alternatives

The third thematic section covers chapters 7 and 8, focusing on alternative investment vehicles such as junk bonds and derivatives. Buffett provides a candid assessment of the risks and returns associated with these instruments, drawing on historical examples to illustrate their potential for both profit and peril.

Key concepts include the dangers of high leverage, the complexity of derivatives, and the importance of creditworthiness. Buffett critiques the use of junk bonds as a financing tool, highlighting their role in high-profile corporate failures and financial crises. He also warns about the systemic risks posed by derivatives, which can amplify losses and create hidden vulnerabilities within the financial system. The section concludes with a reaffirmation of the superiority of investing in productive assets—businesses and real estate—over speculative financial engineering.

For investors, the practical takeaway is to exercise caution when considering complex or highly leveraged instruments. Buffett’s advice is to stick to simple, understandable investments with clear, sustainable cash flows. He urges investors to thoroughly assess the risks of any financial product and to avoid situations where they do not fully understand the underlying dynamics.

In the wake of the 2008 financial crisis and the ongoing proliferation of complex financial products, Buffett’s warnings about leverage and derivatives have proven prescient. Investors who heed these lessons are better positioned to avoid catastrophic losses and to build portfolios that can withstand market shocks.

Part 4: Valuation and Accounting

The final major section, encompassing chapters 9 and 10, delves into the intricacies of valuation and accounting. The unifying theme is the distinction between economic reality and accounting conventions, with a focus on understanding intrinsic value, owner earnings, and the limitations of traditional financial metrics.

Key concepts include the calculation of intrinsic value as the present value of future owner earnings, the shortcomings of book value as a measure of business worth, and the importance of distinguishing between economic and accounting goodwill. Buffett introduces the concept of owner earnings as a more accurate reflection of a company’s profitability, accounting for necessary reinvestments and true cash generation. He also critiques the use of EBITDA and other metrics that can obscure economic reality.

Investors can apply these insights by adopting a more nuanced approach to financial analysis. Rather than relying solely on reported earnings or book value, they should focus on the underlying cash flows, reinvestment needs, and the sustainability of economic profits. This approach enables more accurate valuation and better investment decisions.

In an era where financial engineering and aggressive accounting are increasingly common, Buffett’s emphasis on economic substance over form is more relevant than ever. Investors who master these valuation techniques are better equipped to identify truly undervalued businesses and to avoid value traps.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Deep Dive: Essential Chapters

Chapter 1: Full and Fair Disclosure

This opening chapter is critically important because it establishes the ethical foundation of Buffett’s approach to business and investing. “Full and Fair Disclosure” addresses the necessity of transparency in corporate communications, highlighting the dangers of selective disclosure and the responsibilities of management to shareholders. Buffett’s insistence on forthrightness sets the tone for the entire book, framing the relationship between company leaders and owners as one of trust and stewardship.

Buffett recounts instances where companies have withheld negative information or spun results to create a favorable impression, only for the truth to emerge later and damage shareholder interests. He emphasizes that CEOs must communicate with the same candor in private as they do in public, and that annual letters should be written as if to a partner rather than a faceless crowd. Specific examples from Berkshire Hathaway’s own reporting practices illustrate this point, such as Buffett’s refusal to sugarcoat bad news or to issue earnings guidance that could mislead investors.

Investors can apply these lessons by scrutinizing the quality of management communications when evaluating potential investments. Look for companies that provide comprehensive, honest disclosures—even when the news is unfavorable. Avoid firms that engage in selective disclosure, aggressive accounting, or evasive language. This approach not only reduces the risk of unpleasant surprises but also aligns investment decisions with ethical principles.

Historically, the lack of transparency has been at the root of many corporate scandals, from Enron to WorldCom. In contrast, companies that prioritize full and fair disclosure tend to build lasting trust with investors and are better positioned to weather crises. Buffett’s emphasis on candor remains a gold standard in an era of increasing regulatory scrutiny and demand for corporate accountability.

Chapter 4: Mr. Market

“Mr. Market” is one of the most influential chapters in the book, introducing a metaphor that has become a cornerstone of value investing. Buffett personifies the stock market as an emotional partner who offers to buy or sell shares at different prices each day, often driven by fear or greed rather than rational analysis. This chapter is essential because it teaches investors how to interpret market fluctuations as opportunities rather than threats.

Buffett explains that Mr. Market’s moods should not dictate an investor’s actions. Instead, the intelligent investor takes advantage of market irrationality by buying when prices are unduly low and selling when they are excessively high. He uses historical examples to show how market panics and bubbles have created opportunities for disciplined investors. The chapter includes memorable quotes, such as, “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

To apply these lessons, investors should develop the discipline to act independently of market sentiment. This means conducting their own analysis of intrinsic value and making decisions based on fundamentals rather than price movements. Buffett advises maintaining a watchlist of quality businesses and being prepared to act when Mr. Market offers a favorable price, rather than being swept up in the prevailing mood.

The concept of Mr. Market is particularly relevant during periods of high volatility, such as the 2008 financial crisis or the COVID-19 market crash. Investors who remained calm and rational during these episodes were able to acquire quality assets at bargain prices, while those who panicked often locked in losses. Buffett’s metaphor remains a powerful tool for cultivating the temperament required for long-term investment success.

Chapter 5: Value Investing: A Redundancy

This chapter is vital because it articulates the core philosophy that underpins all of Buffett’s investment decisions: the idea that all true investing is value investing. Buffett argues that the distinction between “value” and “growth” investing is artificial, as the value of any investment is ultimately determined by its future cash flows relative to its price. The chapter challenges readers to rethink common categorizations and to focus on the relationship between price and intrinsic value.

Buffett provides detailed examples of how growth can be a component of value, and he warns against paying excessive prices for anticipated growth. He introduces the concept of the “margin of safety,” borrowed from his mentor Benjamin Graham, as the essential buffer that protects investors from errors in judgment or unforeseen events. The chapter includes data on historical returns for value versus growth stocks, demonstrating the long-term outperformance of strategies grounded in intrinsic value analysis.

Investors can implement these lessons by conducting thorough analysis of a company’s future earning power and comparing it to the current market price. Buffett recommends seeking investments where the price is significantly below a conservative estimate of intrinsic value, thus ensuring a margin of safety. This approach requires patience, discipline, and a willingness to ignore market fads.

Historically, value investing has proven resilient across market cycles, from the Great Depression to the dot-com bust and beyond. Buffett’s insistence that value and growth are not mutually exclusive has influenced generations of investors and remains a guiding principle for those seeking sustainable, long-term returns.

Chapter 6: Intelligent Investing

“Intelligent Investing” serves as a comprehensive guide to Buffett’s investment philosophy, emphasizing the importance of understanding the businesses in which one invests. The chapter is crucial because it distills decades of experience into a set of actionable principles, including the concept of the “circle of competence” and the dangers of the “institutional imperative.”

Buffett illustrates how investors should focus on businesses they can truly understand, avoiding the temptation to stray into unfamiliar industries or complex products. He discusses the psychological pressures that drive herd behavior in institutional settings, such as the desire to conform or to chase short-term performance. The chapter includes quotes such as, “Risk comes from not knowing what you’re doing,” and provides data on the pitfalls of over-diversification and closet indexing.

Investors can apply these lessons by clearly defining their own circle of competence and resisting the urge to invest outside of it. This involves honest self-assessment and a commitment to continuous learning. Buffett also recommends developing a checklist to evaluate business fundamentals, management quality, and competitive advantages before making investment decisions.

The principles outlined in this chapter have stood the test of time, as evidenced by the consistent outperformance of investors who focus on their areas of expertise. In a world of ever-increasing complexity and information overload, the discipline to stick to what you know remains a key differentiator in achieving superior investment results.

Chapter 7: Junk Bonds

This chapter is a critical analysis of the risks associated with high-yield, or “junk,” bonds. Buffett’s examination is important because it exposes the dangers of excessive leverage and the allure of seemingly high returns. He draws on historical examples to illustrate how junk bonds have contributed to corporate failures and financial instability.

Buffett recounts the rise and fall of the junk bond market in the 1980s and 1990s, highlighting cases where companies took on unsustainable debt loads to finance acquisitions or growth initiatives. He provides data on default rates and the long-term underperformance of junk bonds relative to investment-grade securities. The chapter also explores the role of creditworthiness and the importance of conservative capital structures.

For investors, the lesson is clear: avoid the temptation of high yields that come with disproportionate risk. Buffett advises focusing on companies with strong balance sheets, predictable cash flows, and prudent financing. He stresses the importance of understanding the underlying business and its ability to service debt, rather than being seduced by yield alone.

The warnings in this chapter have been borne out by numerous financial crises, from the collapse of Drexel Burnham Lambert to the subprime mortgage meltdown. Investors who prioritize credit quality and avoid excessive leverage are better positioned to preserve capital and achieve steady returns over the long run.

---

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best) overall value plays for 2025

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

---

Chapter 8: Derivatives

“Derivatives” is a cautionary chapter that examines the systemic risks posed by complex financial instruments. Buffett famously described derivatives as “financial weapons of mass destruction,” and this chapter explains why. The discussion is essential for understanding the hidden dangers that can lurk in seemingly sophisticated investment products.

Buffett provides examples of how derivatives have been used to obscure risk, amplify leverage, and create interconnected vulnerabilities within the financial system. He cites the role of derivatives in the collapse of Long-Term Capital Management and the 2008 financial crisis, providing data on the sheer scale of outstanding contracts and the opacity of counterparty exposures. The chapter also critiques the incentives that drive financial innovation, often at the expense of stability.

Investors can apply these lessons by avoiding investments they do not fully understand and by being wary of financial products that promise high returns with little apparent risk. Buffett advises sticking to simple, transparent investments and conducting rigorous due diligence on counterparties and underlying exposures.

The relevance of this chapter has only increased in the years since its publication, as the proliferation of derivatives and structured products continues to pose challenges for regulators and investors alike. Buffett’s warnings serve as a reminder to prioritize simplicity and transparency in all investment decisions.

Chapter 9: Intrinsic Value, Book Value, and Market Price

This chapter is pivotal because it clarifies the key valuation concepts that underpin all intelligent investment decisions. Buffett explains the differences between intrinsic value, book value, and market price, providing a framework for assessing what a business is truly worth. The chapter demystifies valuation and helps investors avoid common traps.

Buffett uses examples from Berkshire Hathaway’s own history to illustrate how book value can diverge from economic reality. He explains that intrinsic value is the present value of future cash flows, while book value is merely an accounting construct. The chapter includes data on historical premiums and discounts to book value, and discusses situations where market price fails to reflect underlying business worth.

Investors can use these lessons by focusing their analysis on intrinsic value rather than being distracted by market price fluctuations or accounting metrics. This involves building detailed financial models, estimating future owner earnings, and discounting them at an appropriate rate. Buffett recommends maintaining a disciplined approach and not being swayed by short-term market movements.

The distinction between intrinsic value and market price is especially important during periods of market exuberance or panic. Investors who anchor their decisions in intrinsic value are less likely to overpay in bull markets or to sell in bear markets, leading to superior long-term outcomes.

Chapter 10: Owner Earnings and the Cash Flow Fallacy

The final key chapter introduces the concept of “owner earnings,” which Buffett presents as a more accurate measure of a company’s profitability than traditional accounting metrics. This chapter is crucial because it addresses the limitations of net income, EBITDA, and reported cash flow, offering a more meaningful way to assess business performance.

Buffett defines owner earnings as net income plus depreciation and amortization, less capital expenditures required to maintain the business. He provides examples showing how companies can manipulate reported cash flow by deferring necessary investments or capitalizing expenses. The chapter includes detailed calculations and case studies from Berkshire Hathaway’s portfolio companies, illustrating how owner earnings provide a clearer picture of economic reality.

Investors can apply this concept by adjusting reported financials to account for true maintenance capital expenditures and by focusing on sustainable, recurring cash flows. Buffett recommends using owner earnings in valuation models and as a basis for comparing companies across industries and accounting regimes.

The owner earnings concept has gained widespread acceptance among sophisticated investors and analysts, providing a valuable tool for cutting through accounting noise. Its relevance has only increased in an era of aggressive financial engineering and creative accounting. By adopting this approach, investors can make more informed, rational decisions and avoid being misled by superficial metrics.

Practical Investment Strategies

- Focus on Economic Moats: Identify companies with sustainable competitive advantages—such as strong brands, cost leadership, network effects, or regulatory barriers. Begin by screening for high and stable return on invested capital (ROIC) and consistent free cash flow generation. Analyze annual reports and industry data to assess the durability of the moat. Invest only when the moat is clear and the price offers a margin of safety.

- Use Owner Earnings for Valuation: Replace traditional metrics like EBITDA or reported net income with owner earnings. Calculate owner earnings as net income plus depreciation/amortization, minus required capital expenditures. Use these figures in your discounted cash flow (DCF) models to estimate intrinsic value. This approach helps avoid overvaluing businesses with aggressive accounting or unsustainable cash flows.

- Maintain a Watchlist and Act Decisively: Develop a list of high-quality businesses you understand well. Set target buy prices based on conservative estimates of intrinsic value, and wait patiently for Mr. Market to offer attractive opportunities. When prices fall below your threshold, act decisively without being swayed by prevailing market sentiment or short-term noise.

- Assess Management Quality and Alignment: Evaluate the track record, communication style, and compensation structure of company management. Look for evidence of shareholder orientation, such as significant insider ownership, candid annual letters, and long-term incentive plans. Avoid companies where management pursues empire-building, excessive leverage, or short-term bonuses at the expense of sustainable value creation.

- Avoid Complex and High-Leverage Instruments: Steer clear of investments you do not fully understand, particularly those involving derivatives, structured products, or excessive leverage. Focus instead on simple, transparent businesses with clear cash flows. Use scenario analysis to stress-test your portfolio against adverse events, and maintain sufficient liquidity to take advantage of market dislocations.

- Emphasize Margin of Safety in Every Investment: Require a significant discount to intrinsic value before committing capital. This margin of safety protects against errors in analysis, unforeseen events, and market volatility. Use conservative assumptions in your valuation models and be willing to walk away if the price does not meet your criteria.

- Regularly Review and Reassess Investments: Schedule periodic portfolio reviews—quarterly or semiannually—to reassess the fundamentals of each holding. Update intrinsic value estimates based on new information, changes in competitive dynamics, or shifts in management strategy. Be willing to sell when a company’s moat erodes, valuation becomes excessive, or better opportunities emerge.

- Think Long-Term and Ignore Short-Term Noise: Anchor your investment decisions in long-term business fundamentals rather than short-term market movements. Resist the temptation to trade frequently or react to headlines. Instead, focus on compounding returns over multi-year periods, reinvesting dividends and capital gains in your best ideas.

Modern Applications and Relevance

Buffett’s principles, as distilled in “The Essays of Warren Buffett,” remain profoundly relevant in today’s rapidly evolving financial landscape. While technology, regulation, and market structures have changed dramatically since the book’s first publication, the core tenets of value investing, transparency, and rationality are as vital as ever. In an era of algorithmic trading, meme stocks, and social media-driven volatility, the discipline to focus on intrinsic value and long-term fundamentals provides a crucial anchor for investors.

One of the most significant changes since the book’s release is the rise of passive investing and the proliferation of exchange-traded funds (ETFs). While these vehicles offer low-cost diversification, they can also exacerbate market swings and disconnect prices from underlying value. Buffett’s advice to treat the market as a partner, not a guide, is especially pertinent when index funds drive prices to extremes. The lessons of Mr. Market and the importance of acting independently are more relevant than ever in a world of herd-driven flows.

Accounting practices have also evolved, with increased scrutiny on non-GAAP metrics, off-balance-sheet liabilities, and aggressive revenue recognition. Yet the dangers Buffett warned about—creative accounting, selective disclosure, and the temptation to obscure economic reality—have not disappeared. Investors must remain vigilant, using owner earnings and conservative valuation methods to cut through the noise and assess true business health.

Recent financial crises, from the dot-com bust to the global financial crisis and the pandemic-induced volatility, have underscored the timelessness of Buffett’s focus on margin of safety, sound balance sheets, and prudent risk management. Companies with strong moats, conservative capital structures, and transparent leadership have consistently outperformed during turbulent periods. The growing emphasis on ESG factors and corporate governance further validates Buffett’s insistence on stewardship and alignment of interests.

Modern examples abound: Apple, a Berkshire holding, exemplifies the power of economic moats, capital discipline, and shareholder-friendly management. Conversely, the collapse of highly leveraged or opaque businesses—such as Enron, Lehman Brothers, or Archegos Capital—reinforces the dangers of ignoring Buffett’s warnings about leverage, complexity, and lack of transparency. By adapting these classic lessons to current conditions, investors can navigate new challenges while avoiding the perennial pitfalls of speculation and short-termism.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Implementation Guide

- Define Your Circle of Competence: Begin by honestly assessing which industries, business models, and types of investments you truly understand. Make a list of sectors where you have expertise, either through professional experience, study, or deep research. Avoid the temptation to stray into unfamiliar territory, regardless of market hype or peer pressure.

- Build a Watchlist of Quality Businesses: Over the next 1-3 months, identify companies with durable competitive advantages, strong balance sheets, and shareholder-oriented management. Use tools like Value Sense’s stock screener to filter for high return on capital, consistent free cash flow, and low debt. Study annual reports, investor presentations, and management letters to deepen your understanding.

- Estimate Intrinsic Value and Set Target Prices: For each company on your watchlist, develop a detailed valuation model based on owner earnings and discounted cash flow. Use conservative assumptions for growth, margins, and required reinvestment. Set target buy prices that provide a meaningful margin of safety—typically 25-40% below your estimate of intrinsic value.

- Construct a Concentrated, Diversified Portfolio: Once attractive opportunities arise, allocate capital to your best ideas while maintaining diversification across sectors and business models. Limit position sizes to 10-15% of the portfolio for any single stock, and ensure that no single risk factor dominates your holdings. Reinvest dividends and capital gains in your highest-conviction ideas.

- Implement Ongoing Review and Risk Management: Schedule quarterly or semiannual portfolio reviews. Update your intrinsic value estimates based on new financial results, industry changes, or management actions. Monitor for signs of moat erosion, excessive leverage, or deteriorating alignment of interests. Be willing to trim or exit positions if the investment thesis weakens or valuations become stretched.

- Document Decisions and Maintain an Investment Journal: For each purchase or sale, record your rationale, assumptions, and expected outcomes. Review these notes periodically to learn from successes and mistakes. This practice fosters discipline, reduces emotional bias, and supports continuous improvement.

- Leverage Resources for Ongoing Education: Dedicate regular time—monthly or quarterly—to reading shareholder letters, investment books, and reputable financial analysis. Use platforms like Value Sense, company filings, and industry reports to stay informed. Attend annual meetings, webinars, or investor conferences to gain new perspectives and deepen your understanding.

--- ---

10+ Free intrinsic value tools

For investors looking to find a stock's fair value, our analytics team has you covered with intrinsic value tools:

📍 Free Intrinsic Value Calculator

📍 Reverse DCF & DCF value tools

📍 Peter Lynch Fair Value Calculator

📍 Ben Graham Fair Value Calculator

📍 Relative Value tool

...and plenty more.

🔍 Explore all these tools for free on the Value Sense platform and start discovering what your favorite stocks are really worth.

FAQ: Common Questions About The Essays of Warren Buffett: Lessons for Corporate America

1. What is the main message of “The Essays of Warren Buffett”?

The main message is that successful investing and corporate management are grounded in rationality, transparency, and long-term thinking. Buffett emphasizes the importance of understanding intrinsic value, maintaining a margin of safety, and aligning management interests with those of shareholders. The book advocates for ethical stewardship, disciplined investing, and a focus on economic realities rather than market speculation or accounting gimmicks.

2. How does Buffett’s approach differ from traditional finance theory?

Buffett rejects the efficient market hypothesis and the use of volatility (beta) as a measure of risk. Instead, he focuses on the risk of permanent capital loss, business fundamentals, and intrinsic value. He critiques the reliance on complex financial models and encourages investors to think independently, act rationally, and ignore short-term market fluctuations. This approach is rooted in value investing principles and a deep understanding of the businesses being purchased.

3. Why is “owner earnings” an important concept in the book?

Owner earnings provide a more accurate measure of a company’s true profitability than traditional metrics like net income or EBITDA. Buffett defines owner earnings as net income plus depreciation and amortization, minus required capital expenditures. This metric accounts for the actual cash available to owners after maintaining and growing the business, helping investors avoid being misled by aggressive accounting or unsustainable cash flows.

4. Can beginners benefit from reading this book, or is it only for professionals?

While the book contains advanced concepts, it is written in a clear, accessible style that makes it valuable for both beginners and experienced investors. Buffett’s use of plain language, real-world examples, and actionable advice ensures that readers at all levels can grasp the key lessons. Beginners will gain a solid foundation in investment principles, while professionals will appreciate the depth and nuance of Buffett’s thinking.

5. How can investors apply the lessons from the book in today’s markets?

Investors can apply the lessons by focusing on intrinsic value, maintaining a margin of safety, and prioritizing transparency and ethical management. In today’s fast-moving and often speculative markets, these principles provide a stable framework for decision-making. By conducting thorough analysis, avoiding leverage and complexity, and thinking long-term, investors can build resilient portfolios that outperform over time.