Undervalued Energy Stocks for November 2025: 6 Oil & Gas Value Plays Worth Your Attention

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

The energy sector has been a rollercoaster ride for investors, but smart money knows that volatility creates opportunity. As we head into September 2025, several oil and gas companies are trading at compelling valuations that savvy value investors shouldn't ignore.

After analyzing comprehensive financial metrics across multiple valuation frameworks, we've identified six energy stocks that appear significantly undervalued. These aren't speculative plays – they're established companies with strong fundamentals, healthy cash flows, and trading prices that don't reflect their intrinsic worth.

Why Energy Value Investing Makes Sense Now

The energy landscape has fundamentally shifted. Companies have learned to operate efficiently at lower oil prices, prioritize shareholder returns, and maintain disciplined capital allocation. This transformation has created a new breed of energy companies that generate substantial free cash flows even in challenging environments.

Current market conditions present a unique opportunity. While many investors remain skeptical about oil and gas investments due to ESG concerns and transition risks, this sentiment has pushed valuations to attractive levels for those willing to look beyond the headlines.

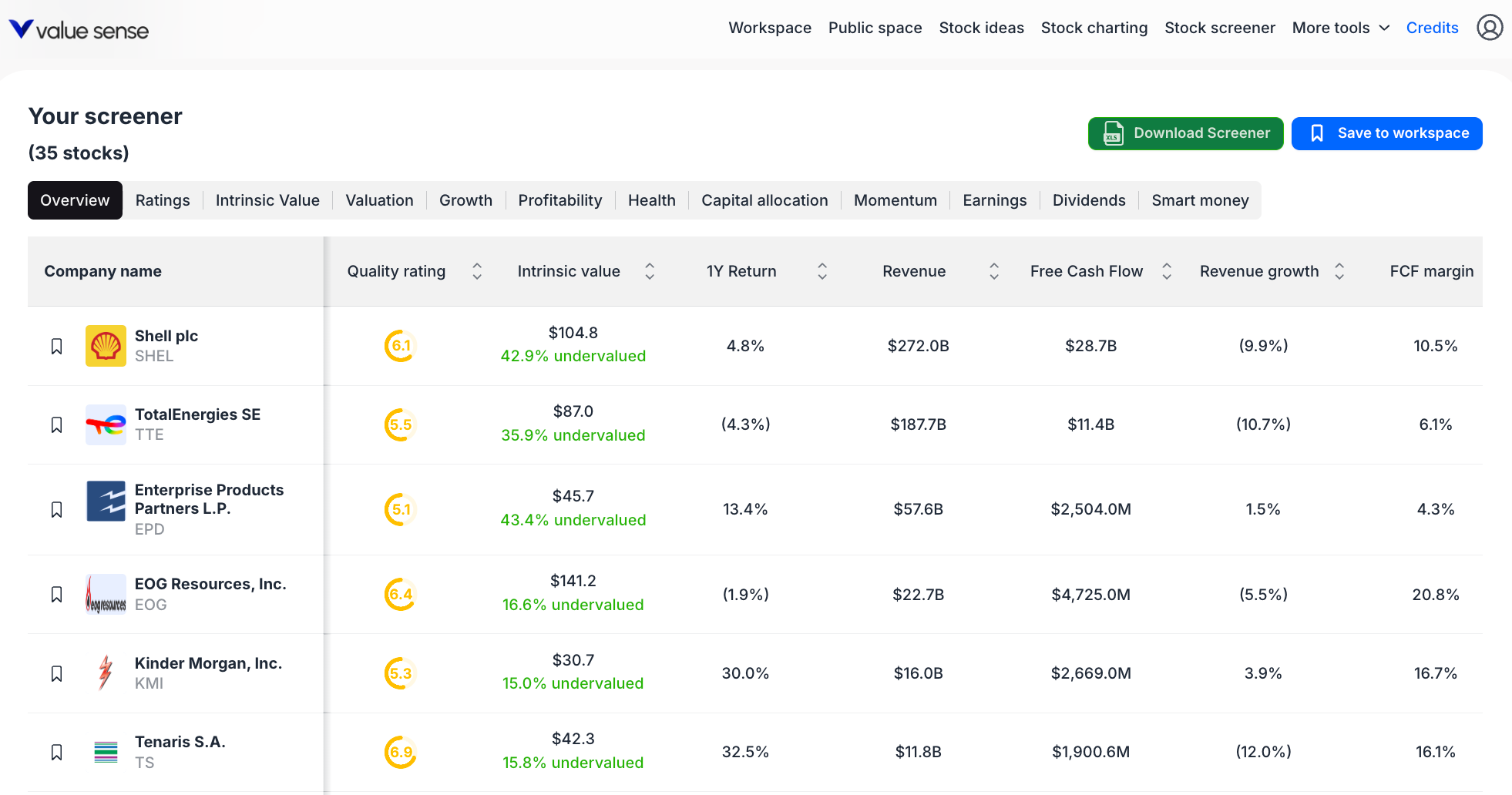

Our Top 6 Undervalued Energy Stocks for 2025

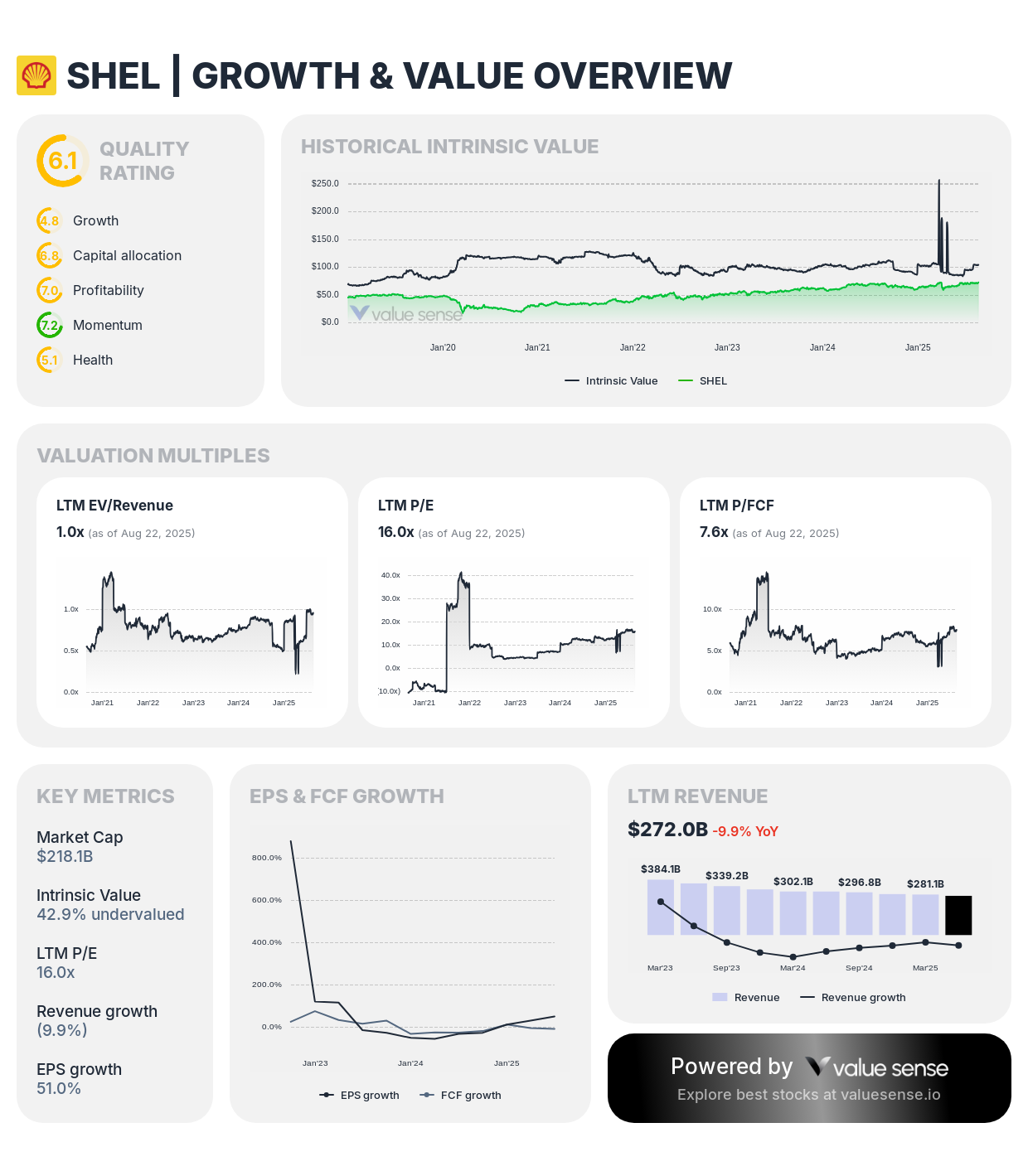

1. Shell plc (SHEL) - The Dividend Aristocrat Trading at Deep Discount

Shell stands out as perhaps the most compelling value proposition in our analysis. With a massive $272 billion in revenue and $28.7 billion in free cash flow, this energy giant is firing on all cylinders.

What makes Shell attractive:

- Trading 42.9% below calculated intrinsic value

- Impressive 10.5% free cash flow margin

- Strong 13.2% FCF yield provides excellent income potential

- Reasonable debt levels with 41.3% debt-to-equity ratio

- Diversified energy portfolio including renewables and LNG

The company's Ben Graham revised fair value analysis suggests it's trading at a staggering discount, making it a cornerstone holding for value-oriented portfolios.

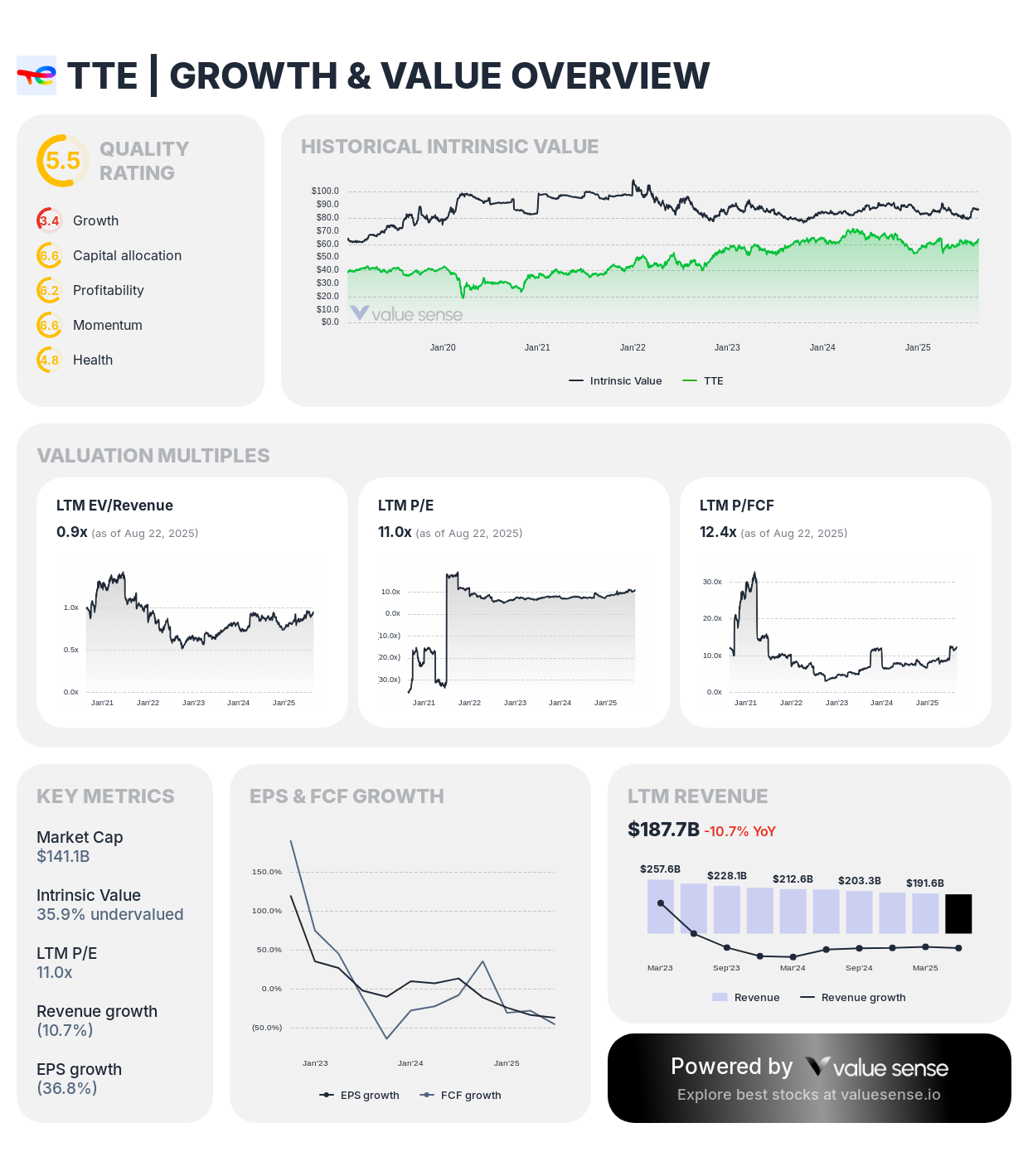

2. TotalEnergies SE (TTE) - European Energy Champion

TotalEnergies combines the stability of an integrated oil major with strategic positioning in the energy transition. At $187.7 billion in revenue, it's a formidable player trading below fair value.

Key investment highlights:

- 35.9% undervalued based on intrinsic value calculations

- Solid 6.1% FCF margin with $11.4 billion in free cash flow

- Attractive 8.1% FCF yield

- Conservative 52.3% debt-to-equity ratio

- Leading European position in renewable energy investments

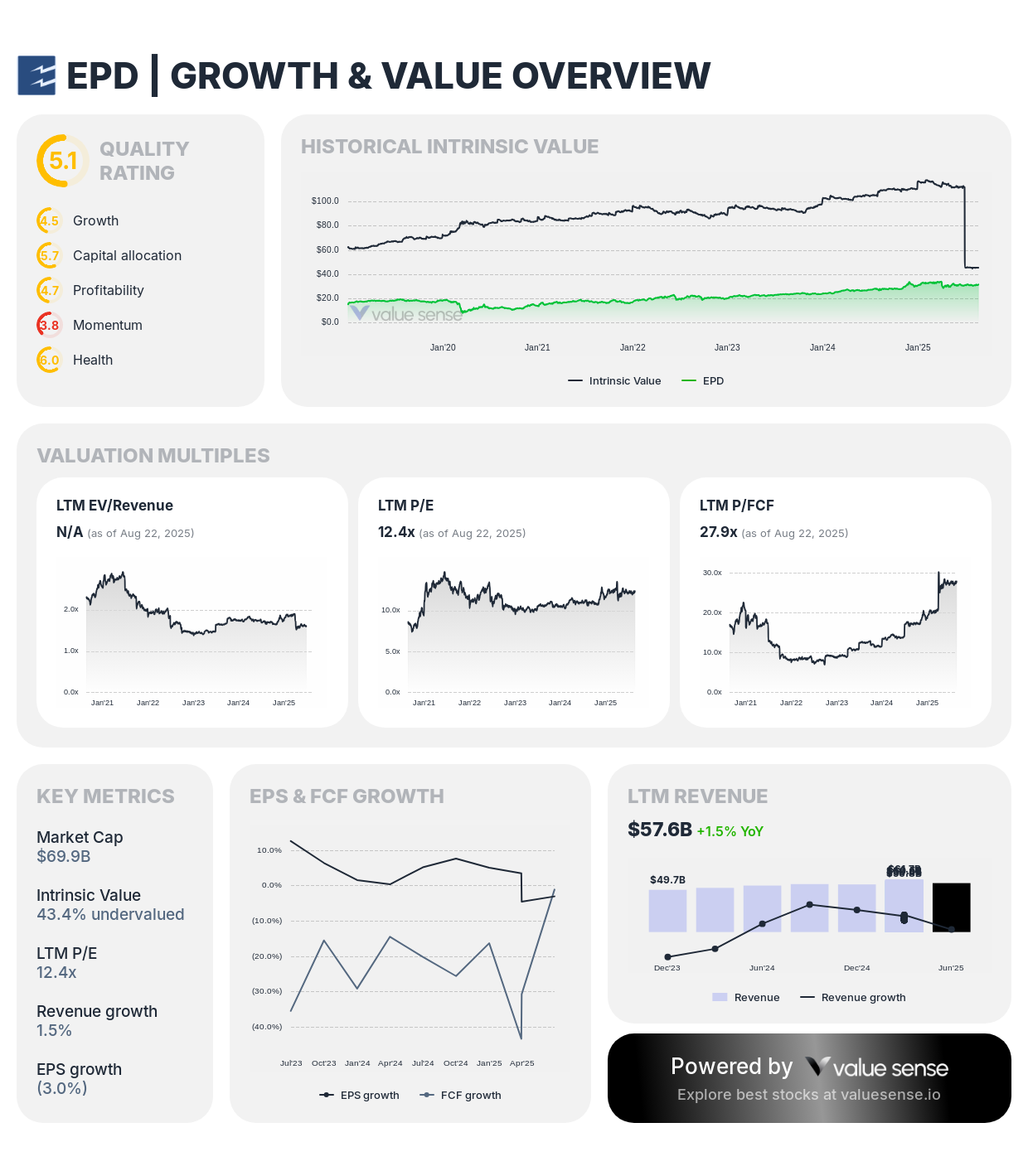

3. Enterprise Products Partners L.P. (EPD) - The Midstream Monster

This master limited partnership operates critical energy infrastructure, providing stable cash flows regardless of commodity price volatility.

Investment case:

- Deep 43.4% discount to intrinsic value

- Exceptional $2.5 billion in free cash flow from $57.6 billion revenue base

- Modest 4.3% FCF margin reflects capital-intensive nature but strong absolute returns

- Minimal debt concerns with partnership structure

- Essential midstream assets with long-term contracts

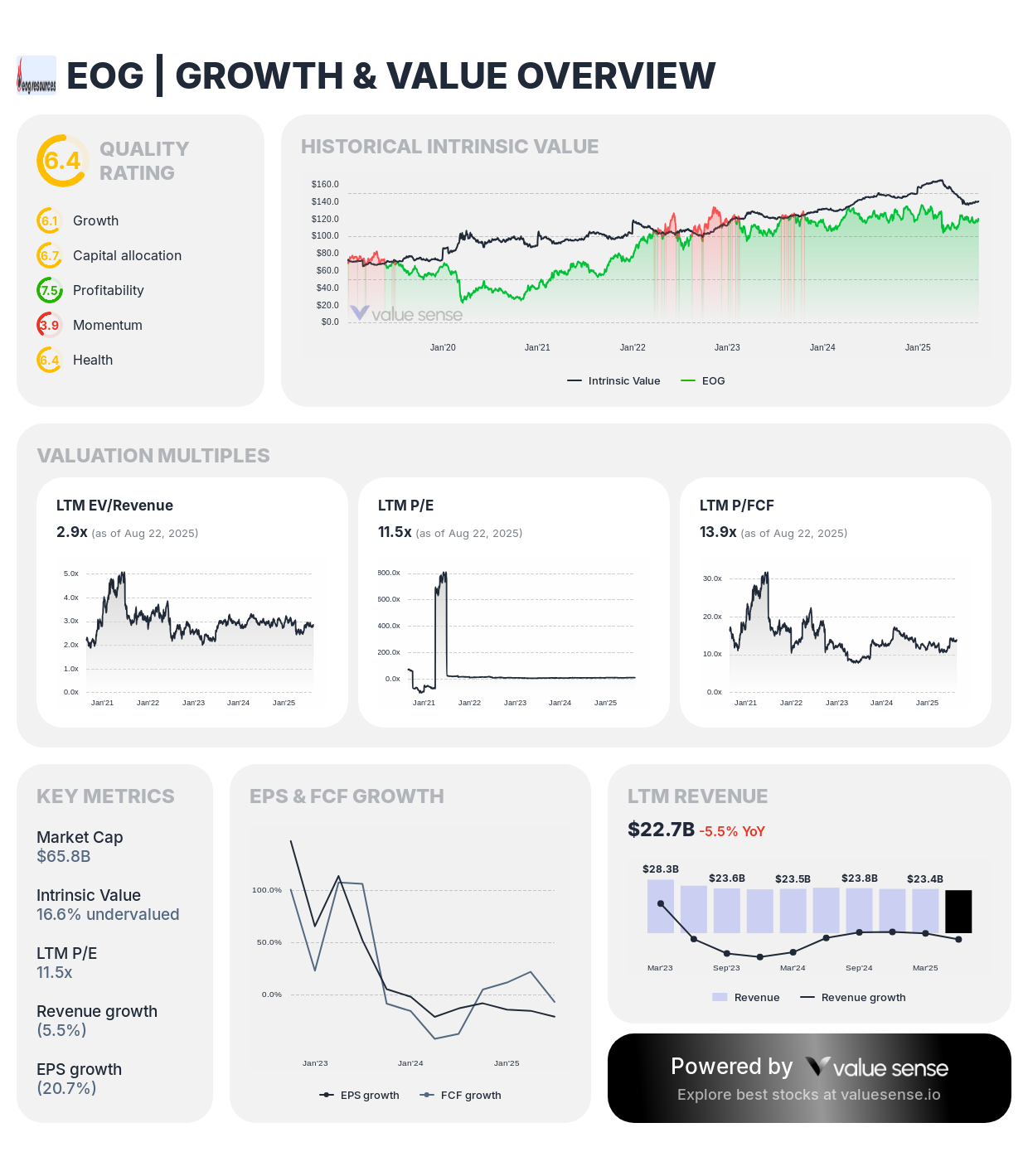

4. EOG Resources, Inc. (EOG) - The Shale Pioneer

EOG Resources has mastered the art of profitable shale production, maintaining strong returns across various oil price environments.

Why EOG deserves attention:

- Quality rating of 6.4 indicates strong financial health

- Impressive 20.8% FCF margin demonstrates operational efficiency

- $4.7 billion free cash flow from $22.7 billion in operations

- Conservative 15.7% debt-to-equity ratio

- Premium shale acreage in proven basins

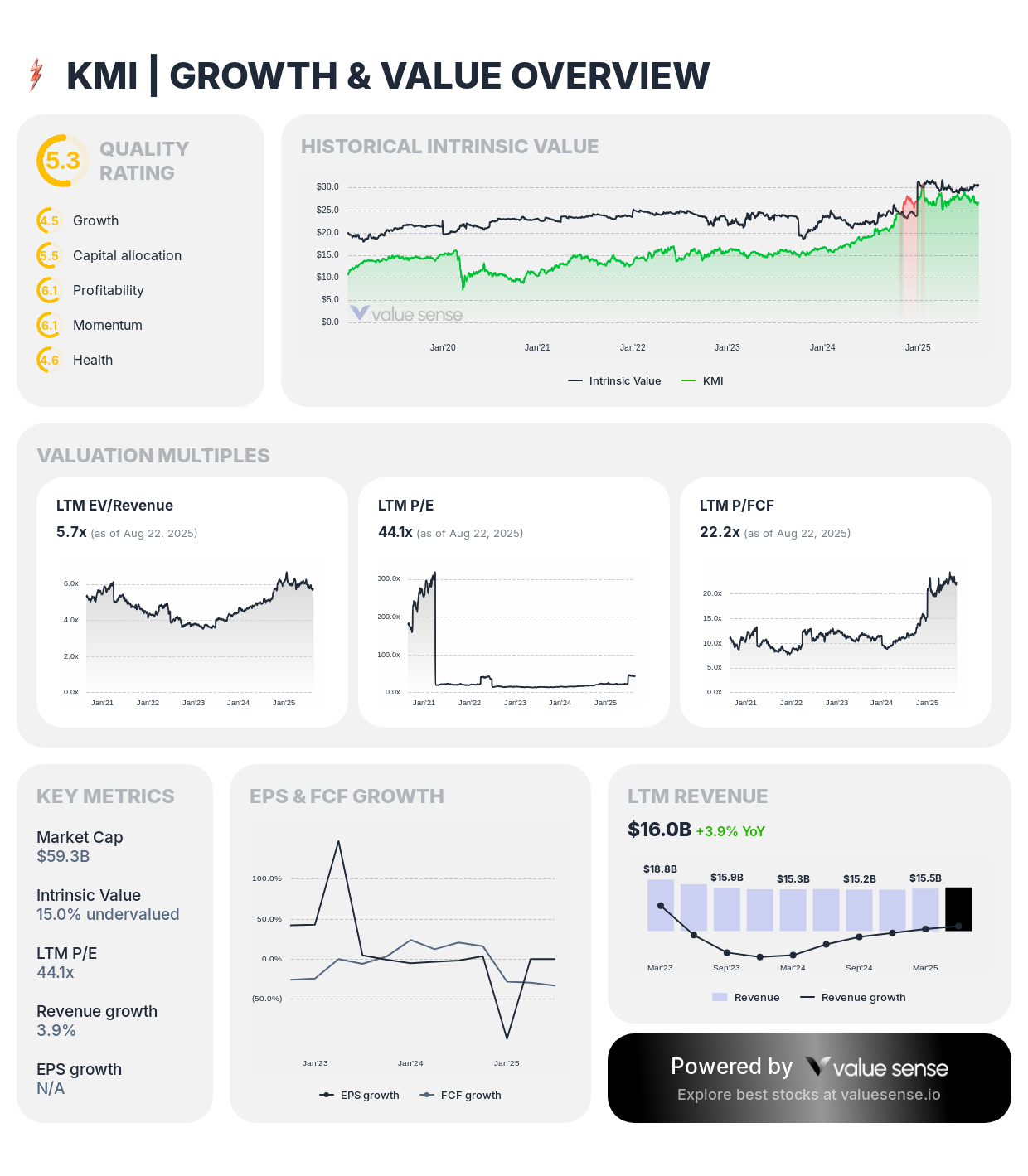

5. Kinder Morgan, Inc. (KMI) - Infrastructure Play with Upside

As North America's largest natural gas pipeline operator, Kinder Morgan provides essential energy transportation services.

Investment merits:

- 15.0% undervalued according to intrinsic value analysis

- Strong 30.0% one-year return demonstrates market recognition

- Substantial 16.7% FCF margin

- $2.7 billion in free cash flow provides steady income potential

- Regulated utility-like business model reduces commodity exposure

6. Tenaris S.A. (TS) - The Steel Tube Specialist

This Argentine company manufactures steel tubes for the energy industry, benefiting from increased drilling activity.

Compelling factors:

- Attractive 15.8% discount to intrinsic value

- Impressive 32.5% one-year return showing momentum

- Strong 16.1% FCF margin

- Ultra-low 2.8% debt-to-equity ratio provides financial flexibility

- Global footprint serving major oil producers

Financial Metrics Comparison Table

| Company | Ticker | Revenue (B) | FCF (B) | FCF Margin | Intrinsic Discount | FCF Yield | Debt/Equity |

|---|---|---|---|---|---|---|---|

| Shell | SHEL | $272.0 | $28.7 | 10.5% | 42.9% | 13.2% | 41.3% |

| TotalEnergies | TTE | $187.7 | $11.4 | 6.1% | 35.9% | 8.1% | 52.3% |

| Enterprise Products | EPD | $57.6 | $2.5 | 4.3% | 43.4% | 3.6% | N/A |

| EOG Resources | EOG | $22.7 | $4.7 | 20.8% | 16.6% | 7.2% | 15.7% |

| Kinder Morgan | KMI | $16.0 | $2.7 | 16.7% | 15.0% | 4.5% | 101.2% |

| Tenaris | TS | $11.8 | $1.9 | 16.1% | 15.8% | 9.7% | 2.8% |

Key Investment Considerations

Commodity Price Sensitivity: While these companies have improved their cost structures, oil and gas price fluctuations will still impact profitability. Current valuations appear to price in conservative commodity assumptions.

Capital Allocation Discipline: Modern energy companies prioritize shareholder returns over growth-at-any-cost strategies. This shift has improved free cash flow generation and return profiles.

ESG and Transition Risks: Environmental regulations and the energy transition present long-term challenges. However, many of these companies are adapting through lower-carbon investments and improved efficiency.

Geopolitical Factors: Energy companies benefit from geopolitical tensions that support higher commodity prices, but they also face risks from sanctions and supply disruptions.

How to Approach These Value Plays

Portfolio Allocation: Consider limiting energy exposure to 5-10% of a diversified portfolio to manage sector-specific risks while capturing upside potential.

Timing Considerations: Dollar-cost averaging into positions can help smooth out commodity price volatility and improve entry points.

Dividend Focus: Many of these companies offer attractive dividend yields, making them suitable for income-focused strategies.

Risk Management: Set position sizes based on individual risk tolerance and monitor key metrics like debt levels and commodity prices.

The Bottom Line on Cheap Oil Stocks

The current environment has created genuine value opportunities in the energy sector. These six companies demonstrate strong fundamentals, conservative balance sheets, and trading prices that don't reflect their intrinsic worth.

While energy investing isn't without risks, the combination of improved operational efficiency, disciplined capital allocation, and attractive valuations makes a compelling case for selective exposure to undervalued energy stocks.

Smart investors understand that the best opportunities often emerge when sectors fall out of favor. For those willing to look past short-term headlines and focus on long-term fundamentals, these energy value plays deserve serious consideration.

Remember, successful energy value investing requires patience, diversification, and a clear understanding of the risks involved. But for investors who get it right, the current setup could deliver substantial returns as these undervalued companies realize their full potential.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2025)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

More Articles You Might Like

📖 Undervalued Growth vs Value Stocks: Which Strategy Wins in 2025?

📖 Amazon Stock Analysis: E-commerce Giant's Undervalued AWS Division

📖 Warren Buffett's Berkshire Hathaway Portfolio 2025

FAQ about value energy stocks

Q: What makes an energy stock "undervalued" in 2025?

A: An undervalued energy stock trades significantly below its intrinsic value based on discounted cash flow analysis, asset valuations, and peer comparisons. Our analysis uses multiple valuation frameworks including Ben Graham methods, Peter Lynch fair value, and DCF models to identify companies trading at 15-43% discounts to calculated fair values.

Q: Are oil and gas stocks risky investments given the energy transition?

A: Energy stocks do carry transition risks, but many companies are adapting by improving efficiency, reducing costs, and investing in lower-carbon technologies. The key is selecting companies with strong balance sheets, conservative debt levels, and diversified operations that can generate cash flows across various scenarios.

Q: How do I know when to buy undervalued energy stocks?

A: Focus on companies with strong free cash flow generation, reasonable debt levels, and trading prices below multiple valuation metrics. Our analysis suggests current levels offer attractive entry points, but dollar-cost averaging can help manage commodity price volatility.

Q: What's the difference between integrated oil majors and pure-play producers?

A: Integrated majors like Shell and TotalEnergies operate across the entire value chain (upstream, downstream, chemicals), providing more stability but potentially lower growth. Pure-play producers like EOG Resources focus on oil and gas extraction, offering higher leverage to commodity prices but more volatility.

Q: Should I invest in energy MLPs like Enterprise Products Partners?

A: Master Limited Partnerships (MLPs) like EPD offer attractive distribution yields and tax advantages but come with K-1 tax forms and different risk profiles. They typically own midstream infrastructure with stable cash flows from long-term contracts, making them less sensitive to commodity price swings than traditional energy stocks.