Undervalued Growth vs Value Stocks: Which Strategy Wins in 2025?

Welcome to the Value Sense Blog, your resource for insights on the stock market! At Value Sense, we focus on intrinsic value tools and offer stock ideas with undervalued companies. Dive into our research products and learn more about our unique approach at valuesense.io

Explore diverse stock ideas covering technology, healthcare, and commodities sectors. Our insights are crafted to help investors spot opportunities in undervalued growth stocks, enhancing potential returns. Visit us to see evaluations and in-depth market research.

ValueSense's stock screener just uncovered something remarkable: high-quality companies trading way below their intrinsic value across both growth and value categories. These aren't obscure penny stocks or broken businesses—we're talking about industry leaders that the market has somehow mispriced.

Let's dig into what makes these companies special and why they ended up on both the undervalued growth and value stock lists.

The Undervalued Growth Champions

Taiwan Semiconductor (TSM) - The $1.2 Trillion Bargain

TSM tops the list with 72.6% undervaluation despite 39.5% revenue growth. This company literally makes chips for Apple, NVIDIA, and every major tech player. When you buy an iPhone or use ChatGPT, chances are TSM manufactured the processor. Yet somehow it's trading at a massive discount to fair value.

ASML Holding (ASML) - The Monopoly Nobody Talks About

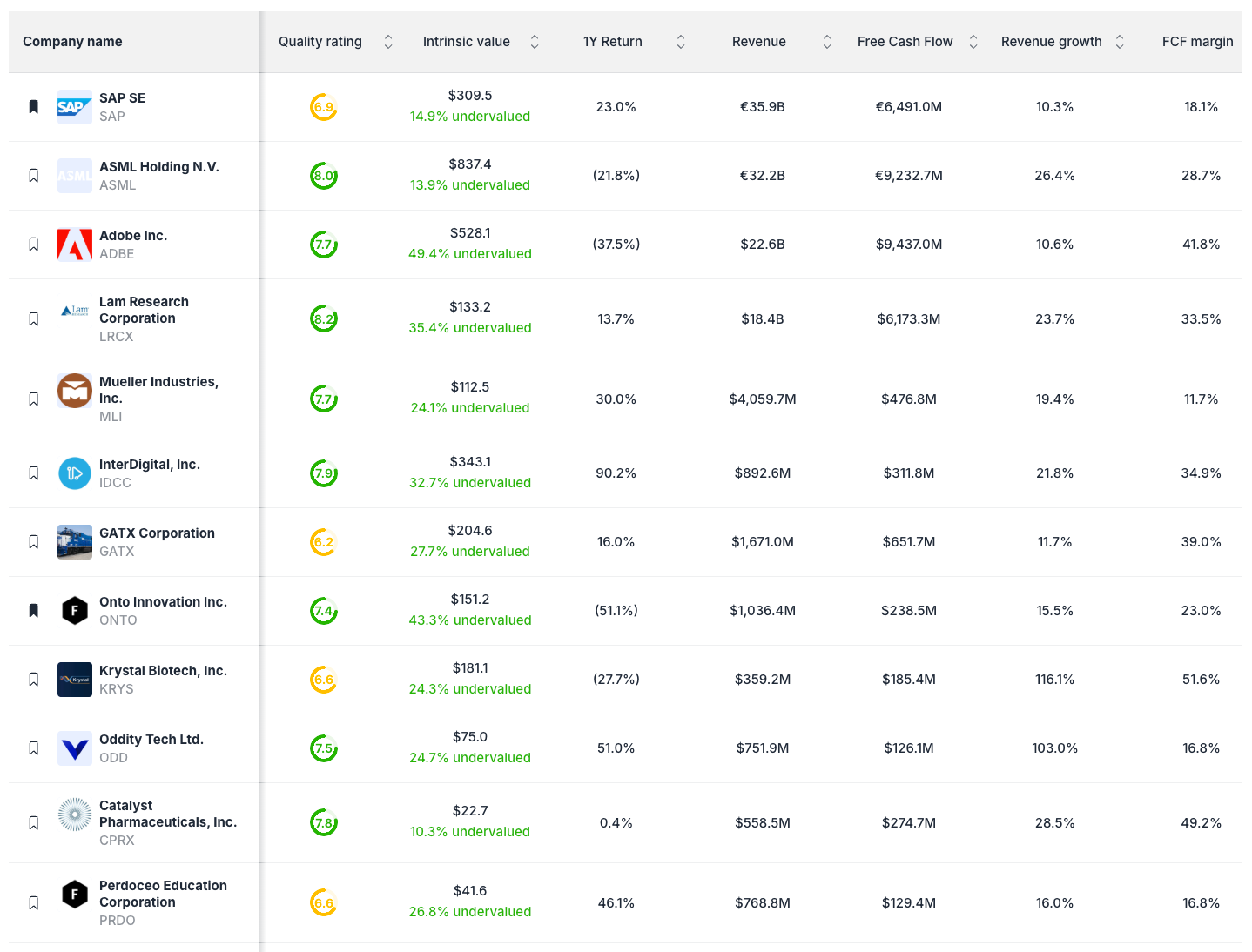

ASML builds the machines that make computer chips. They're the only company on Earth capable of producing extreme ultraviolet lithography equipment—the technology needed for cutting-edge semiconductors. Revenue grew 26.4% while the stock sits 13.9% undervalued. This isn't just a growth story; it's a technological moat that competitors can't breach.

Novo Nordisk (NVO) - Beyond the Ozempic Hype

Everyone knows about Ozempic and weight loss drugs, but the numbers tell a deeper story. Revenue jumped 20.9% while the stock trades 37.4% below intrinsic value. Novo Nordisk isn't riding a fad—they're solving the obesity epidemic with breakthrough treatments that have decades of runway ahead.

Qualcomm (QCOM) - The 5G Infrastructure Play

QCOM shows up as 85.8% undervalued with 15.8% revenue growth. This company designed the chips powering most smartphones and the infrastructure enabling 5G networks. As connectivity becomes central to everything from cars to refrigerators, Qualcomm collects royalties on the technology making it possible.

Anheuser-Busch InBev (BUD) - The Contrarian's Dream

BUD trades 30.9% undervalued despite recent controversies. Here's the thing about beer companies: people keep drinking beer regardless of social media outrage. Revenue grew 22.7% while the stock got hammered on sentiment. Sometimes the best opportunities hide in companies everyone loves to hate.

Lam Research (LRCX) - The Picks and Shovels Play

LRCX makes equipment for manufacturing semiconductors, growing revenue 23.7% while trading 35.4% undervalued. When the chip industry expands, equipment companies like Lam Research get multiple bites at the apple—selling machines, providing service, and upgrading existing installations.

Enbridge (ENB) - The Cash Flow Machine

ENB operates oil and gas pipelines across North America, generating 48.5% revenue growth while trading 76.5% undervalued. Pipeline companies are like toll roads for energy—they collect fees regardless of commodity prices. Enbridge has raised dividends for 29 consecutive years.

The Value Stock Treasure Hunt

Adobe (ADBE) - The Creative Software King

Adobe shows 49.4% undervaluation with 10.6% revenue growth. This company owns creative workflow—Photoshop, Illustrator, Premiere Pro, Acrobat. Every designer, photographer, and video editor pays monthly subscriptions. It's a subscription business with incredible customer stickiness trading at a significant discount.

SAP SE (SAP) - The Enterprise Software Giant

SAP trades 14.9% undervalued while growing revenue 10.3%. They run the backbone systems for most large corporations worldwide. When companies implement SAP, switching costs become enormous. It's boring, profitable, and apparently on sale.

Lam Research (LRCX) - The Crossover Star

LRCX appears on both lists—35.4% undervalued with 23.7% revenue growth. Semiconductor equipment companies bridge growth and value investing perfectly. They benefit from chip industry expansion while trading at reasonable valuations due to cyclical concerns.

Mueller Industries (MLI) - The Infrastructure Beneficiary

MLI makes copper tubing and industrial components, showing 24.1% undervaluation with 19.4% revenue growth. Infrastructure spending creates steady demand for basic materials. It's not glamorous, but infrastructure bills need copper pipes and fittings.

InterDigital (IDCC) - The Patent Goldmine

IDCC returned 90.2% last year while remaining 32.7% undervalued with 21.8% revenue growth. They own crucial wireless technology patents, collecting royalties from smartphone manufacturers. Patent portfolios provide predictable cash flows with built-in inflation protection.

GATX Corporation (GATX) - The Boring Business That Works

GATX leases railcars and aircraft, growing revenue 11.7% while trading 27.7% undervalued. Leasing businesses generate recurring income with physical assets backing the value. Companies need transportation equipment regardless of economic cycles.

Onto Innovation (ONTO) - The Semiconductor Testing Specialist

ONTO provides process control equipment for chip manufacturing, showing 43.3% undervaluation with 15.5% revenue growth. As semiconductors become more complex, testing and quality control become more critical. ONTO benefits from both industry growth and increasing complexity.

Krystal Biotech (KRYS) - The Rare Disease Solution

KRYS develops gene therapies for rare skin diseases, trading 24.3% undervalued with explosive 116.1% revenue growth. Rare disease treatments command premium pricing with limited competition. When you solve problems affecting thousands rather than millions, profit margins can be extraordinary.

What Makes These Lists Special

Several patterns emerge from both the growth and value selections:

Semiconductor Dominance: TSM, ASML, QCOM, and LRCX all benefit from chip industry expansion. Whether making processors, manufacturing equipment, or designing technology, semiconductor exposure appears across both categories.

B2B Focus: Most companies sell to other businesses rather than consumers. Enterprise customers create stickier relationships and more predictable revenue streams than fickle retail buyers.

Infrastructure Plays: From Enbridge's pipelines to GATX's railcars to Mueller's copper tubing, basic infrastructure components show up repeatedly. Boring businesses often generate the most reliable returns.

Patent Protection: QCOM's chip designs, InterDigital's wireless patents, and KRYS's gene therapies all benefit from intellectual property moats that competitors can't easily replicate.

The Crossover Champions

Some companies appear compelling regardless of growth vs. value classification:

Lam Research (LRCX) bridges both categories perfectly—strong growth prospects with reasonable valuations. Semiconductor equipment benefits from industry expansion while avoiding the premium valuations of pure-play chip stocks.

ASML and TSM represent different parts of the semiconductor value chain but similar investment themes. Both companies possess irreplaceable technology advantages in rapidly growing markets.

Adobe and SAP show how software businesses can trade at value prices despite subscription model advantages. Market concerns about competition or growth rates create opportunities for patient investors.

Risk Factors Worth Considering

These opportunities come with legitimate risks that explain their undervaluations:

Cyclical Concerns: Semiconductor companies face boom-bust cycles that can crush earnings during downturns. Equipment manufacturers like ASML and LRCX get hit particularly hard when chip companies reduce capital spending.

Regulatory Risks: Taiwan Semi faces geopolitical tensions between China and Taiwan. Tobacco and alcohol companies like BUD navigate changing social attitudes and potential regulation.

Competition Threats: Even dominant companies like Adobe face challenges from emerging technologies and new competitors. AI tools might disrupt traditional creative workflows.

Economic Sensitivity: Industrial companies like Mueller and GATX depend on economic growth and infrastructure spending that could decline during recessions.

Building Positions in Undervalued Leaders

The beauty of ValueSense's screening approach lies in identifying quality companies at discount prices. Rather than choosing between growth and value strategies, focus on businesses trading below intrinsic value regardless of category.

Consider position weights based on:

- Conviction level: Higher weights for companies with multiple competitive advantages

- Quality ratings: Green-rated companies warrant larger positions than yellow or red-rated names

- Diversification needs: Avoid concentration in single sectors like semiconductors

- Risk tolerance: Growth stocks typically show higher volatility than value plays

The Bottom Line on Market Opportunities

Both lists reveal the same truth: excellent companies sometimes trade below fair value for temporary reasons. Whether it's cyclical concerns in semiconductors, geopolitical fears around Taiwan, or social media backlash against beer companies, markets create opportunities for investors willing to look past short-term noise.

The key lies in recognizing quality businesses at discount prices rather than getting caught up in growth vs. value labels. Taiwan Semi and Adobe both represent compelling opportunities despite falling into different investment categories.

Focus on companies with sustainable competitive advantages, strong financial positions, and reasonable valuations relative to long-term earning power. The market will eventually recognize value in quality businesses—your job involves patience and proper position sizing while waiting for recognition.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2025)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

More Articles You Might Like

📖 Rule of 40 Stocks August 2025: Best Growth-Efficiency Plays

📖 Amazon Stock Analysis: E-commerce Giant's Undervalued AWS Division

📖 Microsoft vs Google: Which Tech Giant Is More Undervalued in 2025?

FAQ about Undervalued Growth vs Value Stocks

Q: Why do quality companies like TSM and Adobe trade below intrinsic value?

A: Multiple factors create temporary mispricings. TSM faces geopolitical concerns about Taiwan, while Adobe deals with competition fears from AI tools. Cyclical worries affect semiconductor companies despite strong fundamentals. Markets often overreact to short-term concerns while ignoring long-term competitive advantages.

Q: How reliable are ValueSense's undervaluation percentages?

A: Intrinsic value calculations provide useful frameworks rather than precise predictions. The percentages help identify potentially mispriced companies for further research. Focus on businesses showing consistent undervaluation across multiple methodologies rather than relying on single metrics.

Q: Should investors buy both growth and value stocks from these lists?

A: Diversification across both categories reduces portfolio risk while capturing different market opportunities. Consider weighting based on individual risk tolerance and investment timeline. Younger investors might emphasize growth names, while those nearing retirement could prefer dividend-paying value stocks.

Q: What's the biggest risk with these undervalued companies?

A: Being early. Markets can stay irrational longer than expected, keeping quality companies undervalued for extended periods. Proper position sizing and diversification help manage this timing risk. Avoid concentrating too heavily in single sectors like semiconductors despite attractive opportunities.

Q: How often should investors review these undervalued stock lists?

A: Quarterly reviews work well for most investors. Companies graduate from undervalued status as prices reach fair value, while new opportunities emerge during market volatility. Focus on business fundamentals rather than daily price movements when making buy/sell decisions.