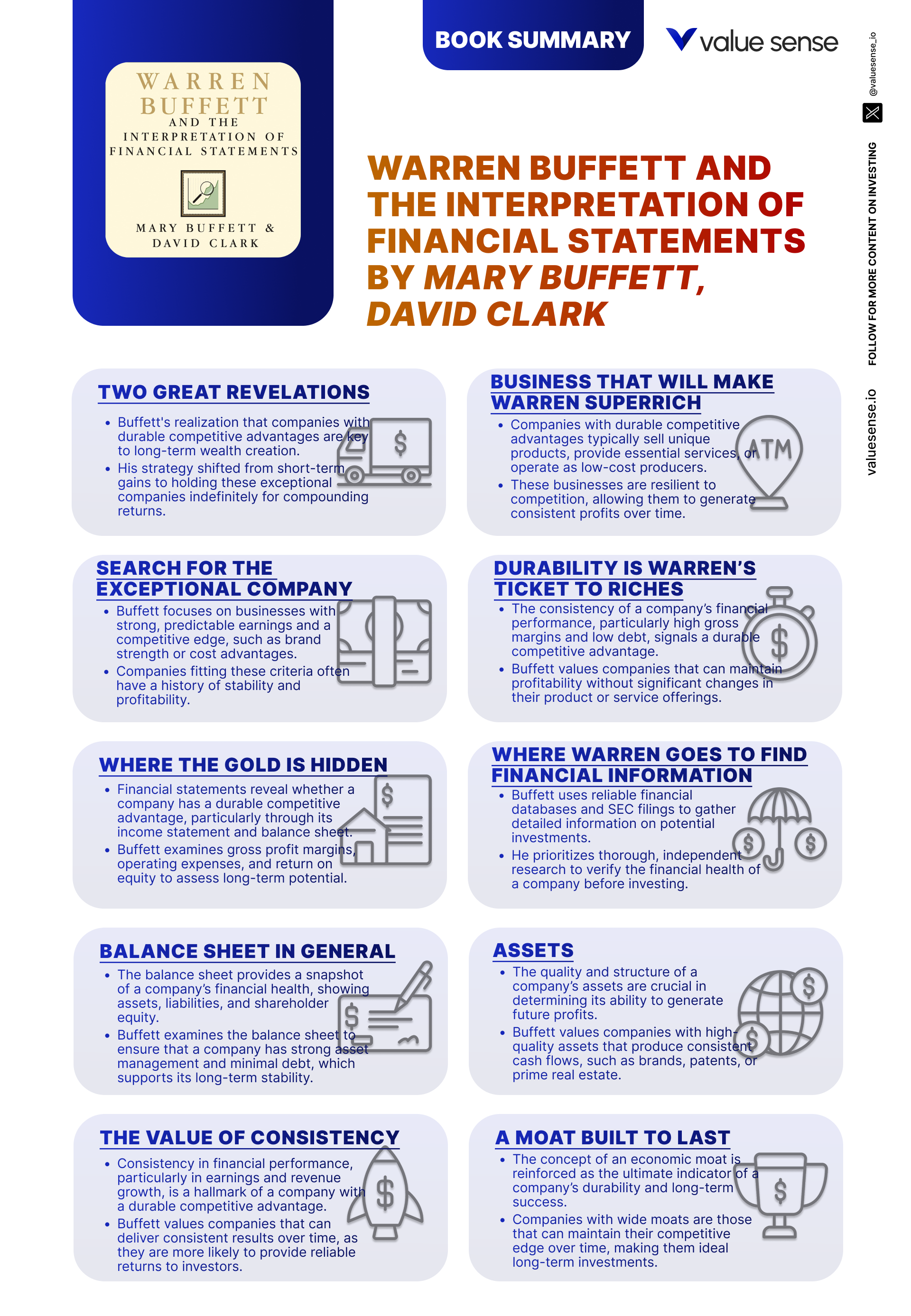

Warren Buffett and the Interpretation of Financial Statements by Mary Buffett and David Clark

Welcome to the Value Sense Blog, your resource for insights on the stock market! You're reading a book review written by the valuesense.io team.

On our platform, you'll find stock research and insights across all sectors. Dive into our research products and learn more about our unique approach at valuesense.io

We offer over 360+ automated stock ideas, a free AI-powered stock screener, interactive stock charting tools, and more than 10 intrinsic value models — all designed to help investors find undervalued growth opportunities.

Book Overview

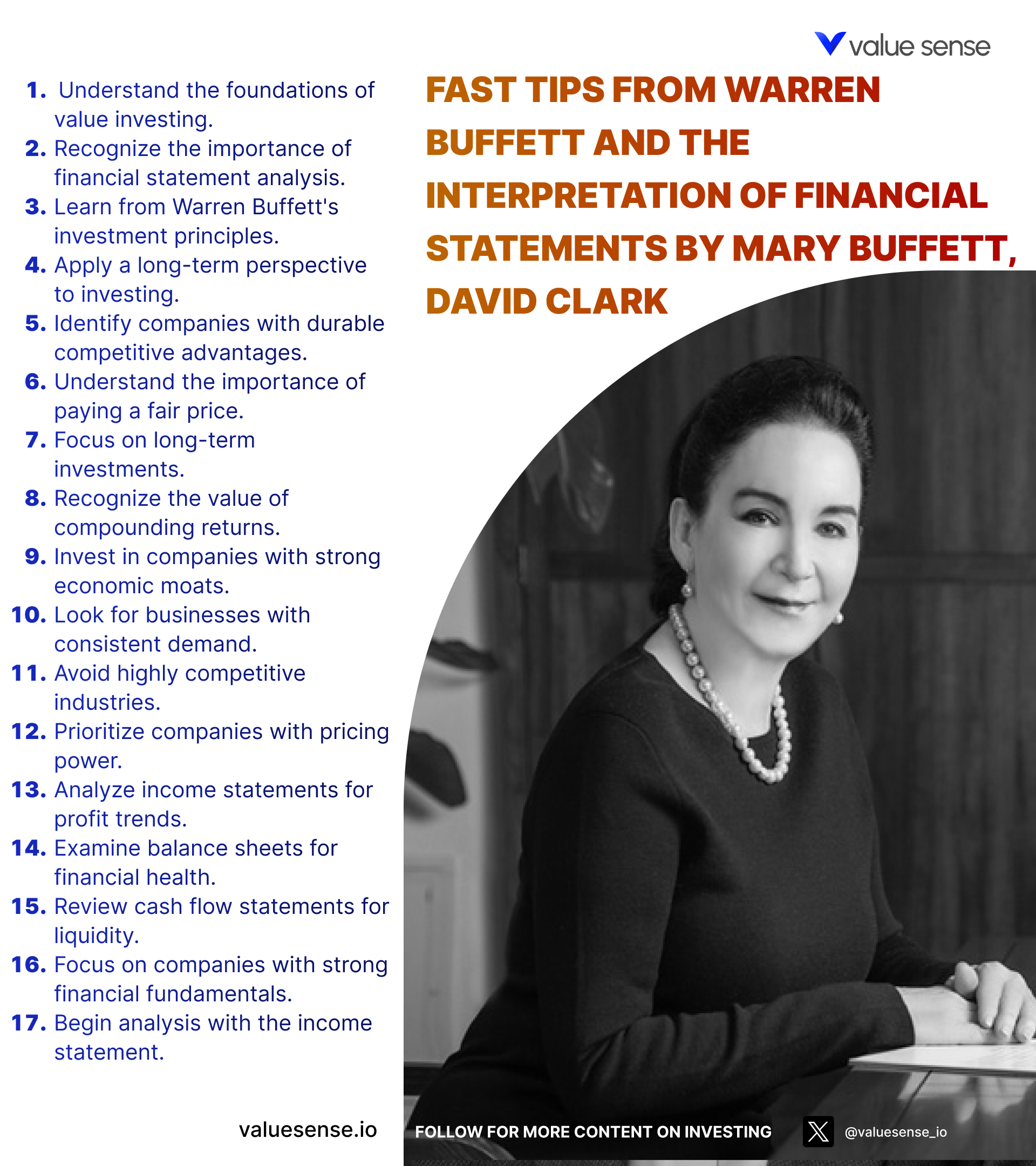

"Warren Buffett and the Interpretation of Financial Statements" by Mary Buffett and David Clark stands as an essential guide for anyone seeking to understand the analytical framework behind one of the most successful investors in history. Mary Buffett, former daughter-in-law of Warren Buffett, brings unique personal insight into Buffett’s thinking, while David Clark, a seasoned Buffettologist, adds rigorous financial analysis. Together, they distill decades of Buffett’s wisdom into a highly accessible format, making this book a staple for both novice and experienced investors.

First published in 2008, this book arrived at a critical moment—on the heels of the global financial crisis, when investors were seeking time-tested principles to navigate uncertainty. The historical context is significant: as financial markets reeled from excessive speculation and opaque accounting, Buffett’s disciplined, transparent approach to value investing offered a beacon of clarity. The book’s main theme is simple yet profound: mastering the interpretation of financial statements is the foundation of intelligent investing. By demystifying the numbers, Buffett’s approach empowers investors to identify companies with genuine, sustainable competitive advantages.

Unlike dense academic texts or purely anecdotal biographies, this book strikes a unique balance. It systematically walks readers through the three core financial statements—income statement, balance sheet, and cash flow statement—using Buffett’s own investment decisions as practical illustrations. The authors break down each line item, revealing how Buffett discerns hidden strengths and weaknesses that others might overlook. This hands-on, example-driven style makes the book not only educational but immediately actionable.

What sets this book apart is its relentless focus on the concept of "durable competitive advantage"—the holy grail of Buffett’s investing philosophy. Rather than chasing short-term trends or speculative growth, Buffett zeroes in on companies with enduring economic moats. The book explains, with clarity and precision, how to spot these moats in the numbers. It also addresses the differences between traditional value investing, as championed by Benjamin Graham, and Buffett’s evolved approach, which incorporates both value and growth elements.

This book is indispensable for anyone who wants to move beyond stock tips and develop a disciplined, analytical process for investment selection. Beginners will appreciate the clear explanations and step-by-step guidance, while seasoned investors will find nuanced insights into Buffett’s unique methodology. Whether you’re a DIY investor, a finance student, or a professional analyst, the book offers a toolkit for making smarter, more confident investment decisions in any market environment.

Key Themes and Concepts

At its core, "Warren Buffett and the Interpretation of Financial Statements" is a masterclass in the art and science of business analysis. The book weaves together several interlocking themes that underpin Buffett’s investment success. These themes are not confined to isolated chapters; rather, they recur throughout the book, reinforcing each other and building a comprehensive framework for long-term wealth creation.

The primary thread running through the narrative is the relentless pursuit of companies with a "durable competitive advantage." This concept is explored from multiple angles—through financial ratios, cash flow analysis, and management evaluation. Alongside this central idea, the book emphasizes rigorous financial statement analysis, prudent risk management, and the distinction between value and growth investing. Each theme is illustrated with real-world examples, making the lessons both vivid and practical.

Below are the most important themes that permeate the book, each offering investors actionable insights into Buffett’s process:

- Durable Competitive Advantage: This is the cornerstone of Buffett’s investment philosophy. The book repeatedly stresses that the best investments are in companies with a sustainable economic moat—something that protects them from competition and allows them to maintain superior profitability over time. Examples include strong brand recognition (like Coca-Cola), cost advantages, regulatory barriers, and network effects. The authors provide checklists and financial indicators—such as consistently high gross profit margins and low capital expenditure requirements—that signal the presence of such advantages. For investors, this theme underscores the importance of looking beyond surface-level metrics to assess a company’s true long-term prospects.

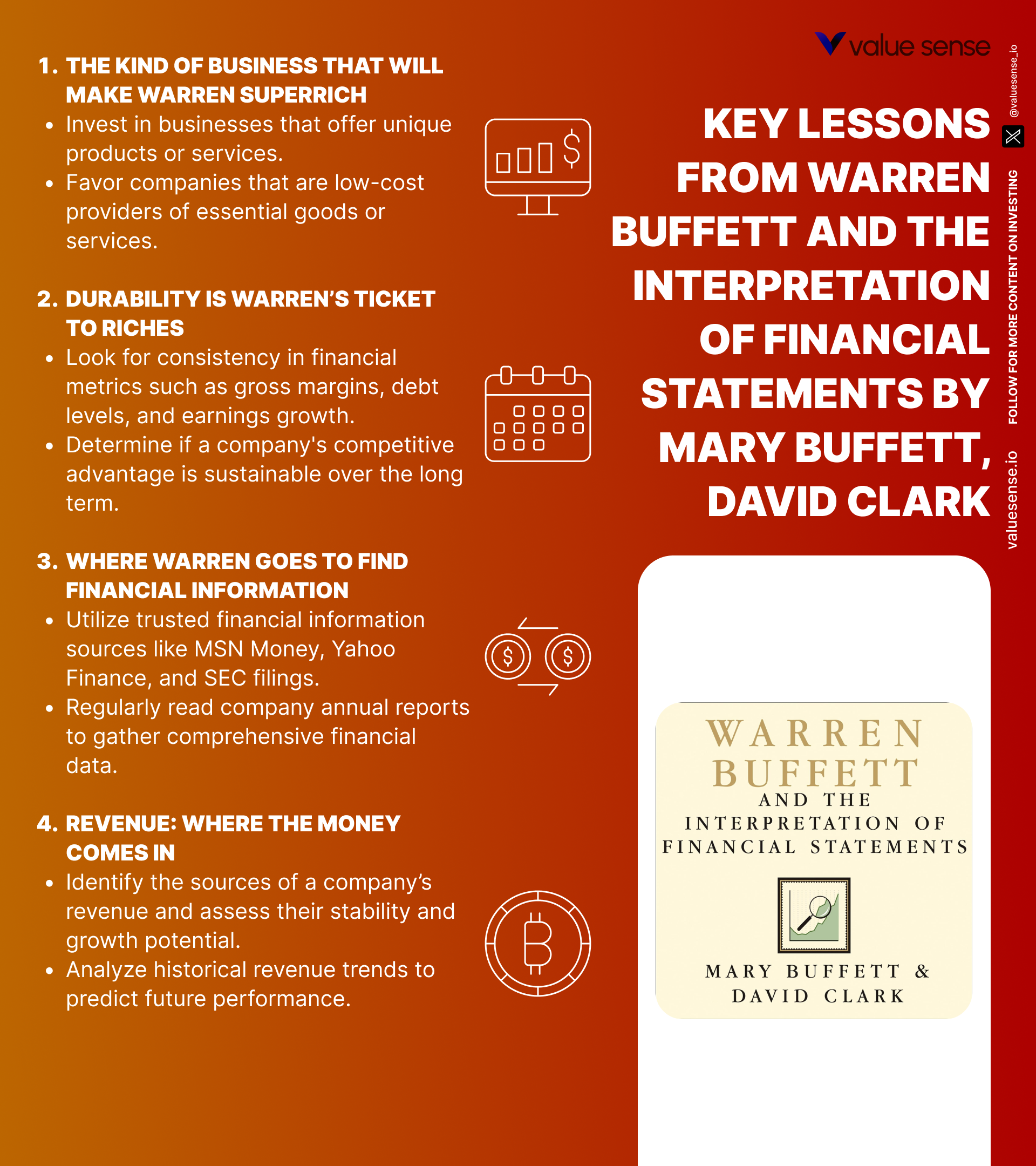

- Financial Statement Analysis: The book demystifies the three core financial statements, showing how Buffett uses them to uncover hidden value and potential red flags. It explains how to interpret line items like revenue, cost of goods sold, gross profit, operating expenses, and net income. For example, Buffett pays close attention to trends in gross profit margins and inventory turnover, using these as proxies for competitive strength. The authors walk readers through real company examples, highlighting how subtle changes in financial ratios can signal shifts in a company’s underlying economics. Mastery of this theme allows investors to move from speculation to evidence-based decision-making.

- Long-Term Investment Strategy: Buffett’s approach is the antithesis of short-term speculation. The book highlights his preference for holding investments indefinitely, provided the company’s fundamentals remain strong. This theme is reflected in his famous dictum: "Our favorite holding period is forever." The authors illustrate how Buffett evaluates a company’s ability to generate consistent earnings and reinvest profits at high rates of return. They also explain how he filters out businesses that may look attractive in the short run but lack staying power. For modern investors, this theme advocates patience, discipline, and a focus on compounding wealth over decades.

- Cash Flow Management: The ability to generate and manage cash is central to Buffett’s investment criteria. The book delves into cash flow statements, explaining why operating cash flow is a better indicator of business health than reported earnings. Buffett favors companies that produce more cash than they consume, as this enables them to weather downturns, invest in growth, and return capital to shareholders. The authors provide practical tools for assessing cash conversion cycles, free cash flow, and liquidity ratios—critical skills for any investor seeking to avoid value traps.

- Risk Management: Unlike many investors who chase high returns at any cost, Buffett is famously risk-averse. The book details how he uses financial statements to assess downside risk—scrutinizing leverage, off-balance-sheet liabilities, and the quality of earnings. The authors discuss Buffett’s aversion to debt-heavy companies and his preference for businesses with predictable cash flows. This theme is particularly relevant in volatile markets, reminding investors that preservation of capital is the first rule of investing.

- Value vs. Growth Investing: The book clarifies the evolution of Buffett’s approach from strict value investing (buying statistically cheap stocks) to a hybrid model that incorporates growth potential. Buffett seeks companies that are not only undervalued but also capable of growing intrinsic value over time. The authors contrast this with the original Graham-style value investing, which focused primarily on low price-to-book and price-to-earnings ratios. For investors, this theme highlights the importance of integrating both value and growth characteristics into portfolio construction.

- Practical Application and Case Studies: Throughout the book, the authors supplement theory with real-world case studies—both Buffett’s successes and the pitfalls he avoids. These stories bring abstract concepts to life, showing readers how to apply the book’s lessons in their own investment process. The practical orientation makes the book not just a theoretical treatise but a hands-on manual for building wealth.

Book Structure: Major Sections

Part 1: Foundations of Buffett's Investment Philosophy

This foundational section (Chapters 1–5) introduces readers to the core pillars of Warren Buffett’s investment philosophy, emphasizing his two great revelations and the importance of a durable competitive advantage. The authors set the stage by contrasting Buffett’s evolved approach with the traditional value investing of Benjamin Graham, highlighting how Buffett’s focus shifted from buying statistically cheap stocks to acquiring high-quality businesses with sustainable moats.

Key concepts explored include Buffett’s criteria for identifying exceptional companies, the significance of economic moats, and the role of intrinsic value. The section underscores the importance of investing in businesses that can consistently generate above-average returns on capital with low capital expenditure requirements. Real-world examples such as Coca-Cola and Gillette are used to illustrate how these principles translate into long-term wealth creation. The authors also explain why Buffett avoids companies in highly competitive industries or those with rapidly changing technology, as these lack the predictability and durability he seeks.

For investors, this section provides a blueprint for screening potential investments: look for companies with strong brands, pricing power, and recurring revenue streams. The practical takeaway is to prioritize business quality over statistical cheapness, using qualitative and quantitative filters to narrow the universe of investable stocks. The emphasis on durable competitive advantage encourages a long-term mindset, discouraging short-term speculation.

The lessons in this section remain highly relevant in today’s market, where technological disruption and global competition can erode competitive advantages quickly. Buffett’s insistence on quality and predictability offers a timeless antidote to market hype. For modern investors, the focus on economic moats and business fundamentals is as vital now as it was when Buffett first articulated these principles.

Part 2: Analyzing Financial Statements

Chapters 6–10 form the analytical core of the book, teaching readers how to interpret the three key financial statements—income statement, balance sheet, and cash flow statement. This section provides a step-by-step guide to deciphering the numbers that reveal a company’s true economic engine. The authors demystify complex accounting terms and show how Buffett uses financial data to separate winners from losers.

Key concepts include understanding revenue, cost of goods sold, gross profit, operating expenses, and net income. The book explains why Buffett prioritizes gross profit margins as a critical indicator of competitive strength and how he uses trends in operating expenses to identify operational efficiency. The authors also highlight the importance of consistency in earnings and the dangers of one-time gains or accounting gimmicks. Real-world examples are provided to illustrate how subtle changes in financial ratios can signal shifts in a company’s underlying economics.

Investors can apply these lessons by developing a checklist for analyzing financial statements: calculate and compare gross profit margins, scrutinize expense trends, and look for red flags such as declining margins or rising debt. The practical approach enables investors to move from gut-feel investing to evidence-based decision-making, reducing the risk of costly mistakes.

In the current era of financial engineering and creative accounting, the ability to interpret financial statements is more important than ever. This section’s focus on transparency, consistency, and underlying business economics equips investors to navigate an increasingly complex investment landscape with confidence.

Part 3: Balance Sheet Insights

This section (Chapters 21–25) dives deep into the balance sheet, showing how assets and liabilities reveal a company’s financial strength and competitive position. The authors explain how Buffett evaluates the quality and composition of assets, the significance of cash reserves, and the implications of inventory and receivables management.

Key points include the role of cash and cash equivalents as a buffer against uncertainty, the importance of manageable inventory levels, and the dangers of excessive leverage. The authors detail how Buffett distinguishes between productive and unproductive assets, and why he favors companies with conservative balance sheets. Specific examples illustrate how changes in asset composition can signal shifts in business strategy or risk profile.

For investors, this section provides actionable tools for assessing balance sheet health: analyze liquidity ratios, monitor inventory turnover, and evaluate the sustainability of debt levels. The insights enable investors to avoid companies with hidden risks and to identify those with the financial flexibility to weather downturns and capitalize on opportunities.

These lessons are particularly relevant in today’s environment of rising interest rates and economic uncertainty. Companies with strong balance sheets are better positioned to survive and thrive, while those with excessive leverage or poor asset quality are vulnerable. This section’s emphasis on prudent financial management is a timeless principle for investors.

Part 4: Cash Flow and Long-Term Investments

Chapters 32–36 focus on the cash flow statement and the role of long-term investments in building durable wealth. The authors highlight why Buffett pays close attention to operating cash flow, free cash flow, and the quality of earnings, arguing that cash—not accounting profits—is the lifeblood of a business.

Key concepts include understanding the components of cash flow statements, the impact of capital expenditures, and the significance of long-term investment assets. The section explains how Buffett distinguishes between companies that generate excess cash and those that are cash-starved, and how he uses this information to assess financial resilience. Real-world case studies illustrate how strong cash flow enables companies to reinvest, pay dividends, and buy back shares.

Investors can apply these insights by prioritizing companies with robust, consistent cash flows and prudent capital allocation policies. The practical takeaway is to look beyond reported earnings and focus on the company’s ability to generate and deploy cash efficiently. This approach helps investors avoid value traps and select businesses with true staying power.

In an era of volatile earnings and aggressive accounting, the focus on cash flow remains highly relevant. The ability to distinguish between accounting profits and real economic value is a critical skill for today’s investors, especially in sectors where capital intensity and working capital needs vary widely.

Part 5: Practical Application of Buffett's Principles

The final major section (Chapters 50–54) translates Buffett’s philosophy and analytical tools into actionable strategies for investors. The authors present case studies of successful investments, highlight common pitfalls, and provide a framework for building a resilient portfolio.

Key points include the importance of patience, discipline, and a long-term perspective. The section explores how Buffett avoids emotional decision-making, sticks to his circle of competence, and waits for high-probability opportunities. The authors also discuss the dangers of over-diversification, market timing, and chasing hot stocks, offering practical alternatives rooted in Buffett’s own practices.

For investors, this section offers a roadmap for implementing Buffett’s principles: develop a watchlist of quality companies, wait for attractive valuations, and invest for the long haul. The focus on real-world examples makes the lessons tangible and immediately applicable, helping investors navigate the psychological and practical challenges of the market.

These principles are as relevant today as ever, especially in an age of information overload and short-termism. Buffett’s emphasis on simplicity, discipline, and focus provides a counterweight to market noise, enabling investors to achieve superior results over time.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Deep Dive: Essential Chapters

Chapter 1: Two Great Revelations That Made Warren the Richest Person in the World

This opening chapter is foundational, laying out the two critical insights that transformed Warren Buffett from a disciple of Benjamin Graham into the world’s preeminent investor. The first revelation was Buffett’s realization that buying statistically cheap stocks (the Graham approach) was not enough; the real magic lay in acquiring high-quality businesses with enduring competitive advantages. The second was his understanding of the compounding power of retained earnings when invested at high rates of return. These insights set the stage for all subsequent analysis and are referenced throughout the book as the bedrock of Buffett’s philosophy.

The authors illustrate these revelations with specific examples, notably Buffett’s investments in companies like Coca-Cola and Gillette. They quote Buffett’s own words about the importance of “economic moats” and show how he shifted from “cigar butt” investing to focusing on businesses that could compound value over decades. The chapter provides data on long-term returns for companies with durable competitive advantages, contrasting them with the fleeting gains from deep-value stocks. It also discusses the role of management, capital allocation, and reinvestment in sustaining high returns.

To apply these lessons, investors should prioritize quality over price, seeking out companies with strong brands, pricing power, and predictable earnings. The chapter recommends screening for high returns on equity, consistent profit margins, and low capital expenditure requirements. Investors are encouraged to think in terms of decades, not quarters, and to focus on the power of compounding rather than short-term gains.

Historically, this shift in approach enabled Buffett to outperform not only the market but also his value investing peers. The chapter’s lessons remain highly relevant in today’s market, where the temptation to chase cheap, risky stocks is ever-present. By internalizing these two revelations, modern investors can build portfolios that are both resilient and capable of exceptional long-term growth.

Chapter 2: The Kind of Business That Will Make Warren Superrich

This chapter is critical because it defines the specific business characteristics that Buffett seeks in his investments. The authors detail how Buffett’s focus shifted from buying undervalued stocks to acquiring businesses with a sustainable competitive edge, or “economic moat.” The chapter underscores the importance of predictability, consistency, and the ability to generate high returns on capital without requiring constant reinvestment.

Examples include Buffett’s investments in See’s Candies and American Express, both of which possess strong brands and customer loyalty. The authors quote Buffett on the dangers of “commodity businesses” and provide data on the superior long-term returns of companies with pricing power. The chapter also discusses the role of intangible assets, such as patents and trademarks, in sustaining competitive advantage. Charts and tables illustrate the correlation between high gross profit margins and long-term wealth creation.

Investors are advised to look for companies with recurring revenue, low susceptibility to technological disruption, and the ability to raise prices without losing customers. The chapter suggests concrete metrics—such as return on assets, return on equity, and gross profit margin—to screen for these qualities. The practical takeaway is to avoid businesses in highly competitive or rapidly changing industries, as these lack the predictability Buffett values.

In the broader historical context, this chapter explains why Buffett has consistently outperformed the market by avoiding the “herd mentality” of Wall Street. Modern examples, such as Google and Apple, demonstrate how companies with strong moats continue to dominate their industries. The chapter’s lessons are timeless, offering a framework for identifying businesses that can generate wealth across multiple market cycles.

Chapter 5: Financial Statement Overview: Where the Gold is Hidden

This chapter is indispensable because it introduces the three core financial statements—income statement, balance sheet, and cash flow statement—and explains why they are the key to uncovering investment opportunities. The authors argue that true investing success depends on the ability to interpret these documents and identify the “hidden gold” within a company’s numbers.

The chapter provides detailed breakdowns of each statement, with examples from real companies. It explains how to read income statements to assess profitability, how balance sheets reveal financial strength, and how cash flow statements indicate liquidity and operational efficiency. The authors highlight specific line items—such as gross profit, operating expenses, and retained earnings—that Buffett scrutinizes. Quotes from Buffett reinforce the importance of understanding the numbers beneath the headlines.

For practical application, investors are encouraged to develop a systematic approach to financial statement analysis. The chapter suggests creating a checklist for each statement, focusing on key metrics like net income growth, asset turnover, and free cash flow generation. The authors also warn against relying solely on earnings per share or headline revenue, as these can be manipulated or misleading.

Historically, Buffett’s mastery of financial statement analysis has enabled him to identify undervalued gems overlooked by the market. In today’s world of complex accounting and financial engineering, these skills are more valuable than ever. The chapter’s step-by-step guidance empowers investors to make informed, evidence-based decisions in any market environment.

Chapter 7: Where Warren Starts: The Income Statement

This chapter is crucial because it reveals Buffett’s process for evaluating a company’s economic engine, starting with the income statement. The authors explain how Buffett dissects revenue, cost of goods sold, gross profit, operating expenses, and net income to assess profitability and operational efficiency. This granular approach allows him to distinguish between companies with genuine earning power and those relying on accounting tricks.

Detailed examples include side-by-side comparisons of income statements from leading consumer goods companies. The authors show how Buffett identifies trends in gross profit margins, monitors expense ratios, and assesses the consistency of earnings over time. Quotes from Buffett reinforce the importance of focusing on recurring, rather than one-time, income. The chapter also discusses the significance of stable or rising gross profit margins as a sign of competitive strength.

Investors can apply these lessons by building their own income statement analysis templates. The chapter recommends tracking key ratios, such as gross profit margin and operating margin, and comparing them to industry benchmarks. It also suggests looking for red flags, such as declining margins or volatile earnings, which may indicate structural weaknesses.

In historical context, Buffett’s focus on the income statement has helped him avoid companies with deteriorating business models or unsustainable growth. Modern investors can use these techniques to assess companies in any sector, ensuring that their portfolios are built on a foundation of real, repeatable earnings power.

Chapter 10: Gross Profit/Gross Profit Margin: Key Numbers for Warren in His Search for Long-Term Gold

This chapter is a deep dive into one of Buffett’s favorite metrics: gross profit margin. The authors explain why high and stable gross profit margins are a hallmark of companies with durable competitive advantages. The chapter provides a framework for calculating and interpreting gross profit margins, using real-world examples from industries like food, beverages, and consumer products.

Specific data is presented to show how companies like Coca-Cola and Procter & Gamble maintain gross profit margins far above industry averages, signaling pricing power and operational efficiency. The authors quote Buffett on the importance of “economic moats” and provide charts comparing gross profit margins across sectors. They also discuss how changes in input costs or competitive dynamics can erode margins, serving as an early warning sign for investors.

For practical application, the chapter recommends screening for companies with gross profit margins consistently above 40%, as these are more likely to have sustainable competitive advantages. Investors are advised to monitor trends in margins over time and to investigate any significant fluctuations. The chapter also suggests using gross profit margin as a filter in stock screeners and as a benchmark for comparing companies within the same industry.

Historically, Buffett’s reliance on gross profit margin has helped him identify winners in industries where price competition is fierce. Modern investors can use this metric to avoid commodity businesses and focus on companies with genuine pricing power and brand strength. The chapter’s lessons are particularly relevant in today’s inflationary environment, where cost pressures can quickly erode profitability.

---

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best) overall value plays for 2025

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

---

Chapter 21: Balance Sheet in General

This chapter introduces the balance sheet as a critical tool for assessing a company’s financial position and stability. The authors explain the structure of the balance sheet—assets, liabilities, and equity—and how each component reveals insights into a company’s operational and financial health. The chapter emphasizes the importance of net worth (equity) as a buffer against business risk.

Examples include balance sheets from leading industrial and consumer companies, with detailed breakdowns of cash, inventory, receivables, and debt. The authors quote Buffett on the dangers of excessive leverage and the importance of a conservative capital structure. Charts and tables illustrate how changes in asset and liability composition can affect a company’s risk profile and investment appeal.

Investors are encouraged to analyze liquidity ratios (current and quick ratios), debt-to-equity ratios, and trends in working capital. The chapter recommends avoiding companies with high levels of short-term debt or rapidly rising liabilities, as these are signs of financial stress. The practical takeaway is to prioritize companies with strong, flexible balance sheets that can weather economic downturns.

Historically, Buffett’s focus on balance sheet strength has helped him avoid catastrophic losses during market crises. Modern investors can use these lessons to build more resilient portfolios, especially in volatile or uncertain environments. The chapter’s emphasis on financial conservatism remains a timeless principle for long-term success.

Chapter 24: Cash and Cash Equivalents: Warren's Pile of Loot

This chapter highlights the strategic role of cash reserves in Buffett’s investment approach. The authors explain how cash and cash equivalents provide companies with the flexibility to seize opportunities, fund growth, and weather downturns. The chapter details how Buffett evaluates the size and composition of cash holdings on the balance sheet, and why he favors companies with ample liquidity.

Examples include case studies of companies that survived recessions or capitalized on acquisitions thanks to strong cash positions. The authors quote Buffett on the importance of “dry powder” and provide data on the cash balances of Berkshire Hathaway and its subsidiaries. Charts illustrate the correlation between cash reserves and business resilience, especially during periods of market stress.

Investors can apply these lessons by analyzing the cash and cash equivalents line item on the balance sheet and comparing it to short-term liabilities. The chapter recommends screening for companies with current ratios above 1.5 and monitoring trends in cash generation and usage. The practical takeaway is to avoid companies with thin liquidity or excessive reliance on external financing.

Historically, Buffett’s preference for cash-rich companies has protected his portfolio during market downturns and enabled him to act decisively when opportunities arise. Modern investors can use these insights to build more flexible and resilient portfolios, especially in uncertain or rapidly changing markets.

Chapter 32: Long-Term Investments: One of the Secrets to Warren's Success

This chapter explores the significance of long-term investments in Buffett’s portfolio strategy. The authors explain how Buffett distinguishes between short-term speculation and long-term wealth creation, focusing on companies that can compound value over decades. The chapter details how long-term investments are reported on the balance sheet and how Buffett evaluates their quality and sustainability.

Real-world examples include Berkshire Hathaway’s holdings in Coca-Cola, American Express, and other blue-chip companies. The authors quote Buffett on the importance of patience and provide data on the long-term returns of his core holdings. Charts and tables illustrate the impact of compounding and the benefits of holding investments through multiple market cycles.

For practical application, investors are advised to adopt a long-term perspective, focusing on businesses with predictable earnings and robust growth prospects. The chapter recommends screening for companies with high returns on invested capital and stable or growing dividends. The practical takeaway is to avoid frequent trading and to let compounding work its magic over time.

Historically, Buffett’s long-term approach has enabled him to ride out market volatility and capture the full value of his investments. Modern investors can use these lessons to build portfolios that are both resilient and capable of generating superior returns over the long run. The chapter’s emphasis on patience and discipline is a key differentiator in today’s fast-paced markets.

Chapter 50: Practical Application of Buffett's Principles

This chapter is the capstone of the book, translating Buffett’s philosophy and analytical tools into practical steps for investors. The authors present case studies of successful investments, highlight common pitfalls, and provide a framework for building a resilient portfolio. The chapter distills Buffett’s approach into actionable advice, making it accessible to investors at all levels.

Examples include detailed breakdowns of real-world investment decisions, with quotes from Buffett on the importance of patience, discipline, and sticking to one’s circle of competence. The authors provide checklists for screening companies, evaluating financial statements, and assessing management quality. Charts and tables illustrate the impact of compounding and the dangers of over-diversification and market timing.

Investors are encouraged to develop a watchlist of quality companies, wait for attractive valuations, and invest for the long haul. The chapter recommends setting clear investment criteria, maintaining a long-term perspective, and avoiding emotional decision-making. The practical takeaway is to focus on process over prediction, building a portfolio that can withstand market volatility and deliver consistent returns.

Historically, Buffett’s disciplined approach has enabled him to achieve superior results with lower risk. Modern investors can use these lessons to navigate today’s complex and unpredictable markets, building portfolios that are both resilient and capable of compounding wealth over time. The chapter’s emphasis on practical application makes it an indispensable resource for anyone serious about investing.

Practical Investment Strategies

- Focus on Companies with Durable Competitive Advantages: Begin by screening for companies with consistently high gross profit margins (typically above 40%), strong brand recognition, and recurring revenue streams. Use tools like the Value Sense screener to filter for these characteristics. Analyze qualitative factors such as customer loyalty, regulatory barriers, and network effects. Prioritize businesses with a history of maintaining or growing market share in stable or slowly evolving industries. This approach reduces the risk of disruption and provides a foundation for long-term compounding.

- Master Financial Statement Analysis: Develop a systematic process for reviewing income statements, balance sheets, and cash flow statements. Start by calculating key ratios: gross profit margin, operating margin, return on equity, and debt-to-equity. Look for consistency and upward trends over at least five years. Use the Value Sense platform to automate ratio calculations and visualize trends. Always read the footnotes for hidden risks or accounting adjustments. This rigorous analysis helps you avoid value traps and identify genuine investment opportunities.

- Prioritize Cash Flow over Reported Earnings: Focus on companies that generate strong and consistent operating cash flow, as this is a better indicator of business health than net income. Calculate free cash flow by subtracting capital expenditures from operating cash flow. Screen for companies with positive free cash flow in most years, and compare cash flow growth to net income growth for signs of earnings quality. Avoid businesses with large swings in cash flow or those reliant on external financing. This strategy ensures your investments are backed by real, repeatable cash generation.

- Maintain a Conservative Approach to Leverage: Use balance sheet analysis to avoid companies with excessive debt or off-balance-sheet liabilities. Calculate the current ratio, quick ratio, and debt-to-equity ratio for each candidate. Favor businesses with current ratios above 1.5 and debt-to-equity ratios below 0.5, especially in cyclical or capital-intensive industries. Monitor trends in interest coverage and watch for rising debt levels relative to earnings. This conservative approach minimizes downside risk and enhances portfolio resilience.

- Invest for the Long Term and Let Compounding Work: Build a watchlist of quality businesses and wait for attractive entry points—typically when the stock trades at a reasonable multiple of normalized earnings or free cash flow. Once invested, resist the urge to trade frequently or react to short-term market noise. Set a minimum holding period of five years, and review each holding annually for changes in fundamentals. Reinvest dividends and allow winners to compound. This discipline magnifies returns and reduces transaction costs.

- Use Intrinsic Value Models to Avoid Overpaying: Calculate intrinsic value using discounted cash flow (DCF) analysis, owner earnings, or other Buffett-inspired models. Compare current market price to your estimate of intrinsic value, and require a margin of safety of at least 20–30%. The Value Sense platform offers multiple intrinsic value calculators to streamline this process. Only purchase when the stock trades below your fair value estimate, and be patient—opportunities arise during market corrections or when quality companies face temporary setbacks.

- Monitor Management Quality and Capital Allocation: Evaluate the track record of company leadership by reviewing historical decisions on dividends, share buybacks, and acquisitions. Look for evidence of shareholder-friendly policies and prudent capital allocation. Avoid companies with frequent management turnover, excessive executive compensation, or a history of value-destroying acquisitions. This qualitative assessment complements your financial analysis and helps ensure your investments are managed by capable stewards.

- Continuously Educate Yourself and Refine Your Process: Stay current by reading annual reports, investor presentations, and industry news. Use platforms like Value Sense to access automated research, stock screeners, and valuation tools. Regularly review your portfolio for changes in fundamentals, and be willing to make adjustments as new information emerges. Join investment communities, attend webinars, and read classic investment books to deepen your understanding. Continuous learning is essential for long-term success in investing.

Modern Applications and Relevance

The principles outlined in "Warren Buffett and the Interpretation of Financial Statements" are remarkably resilient, even as the investment landscape evolves. Today’s markets are characterized by rapid technological change, globalization, and unprecedented access to information. Yet, the fundamental truths that underlie Buffett’s approach—business quality, financial discipline, and long-term thinking—remain as relevant as ever. Investors who internalize these lessons are better equipped to filter out noise and focus on what truly matters: the underlying economics of the businesses they own.

Since the book’s publication, several trends have emerged that test the durability of Buffett’s principles. The rise of intangible assets (such as software, data, and brand equity) has made traditional financial statement analysis more challenging, but not obsolete. Buffett’s emphasis on competitive advantage and cash generation is especially useful in evaluating modern tech giants like Alphabet, Microsoft, and Apple. These companies exhibit many of the hallmarks Buffett seeks: high margins, network effects, and enormous free cash flow. By applying the book’s framework, investors can adapt classic analysis to new business models.

What has changed most is the speed and volatility of markets, driven by algorithmic trading and social media-fueled speculation. The temptation to chase short-term gains or react to headlines is greater than ever. Yet, Buffett’s insistence on patience, discipline, and a focus on intrinsic value provides a powerful counterweight. The book’s lessons on risk management, balance sheet strength, and cash flow resilience are particularly relevant in times of market stress, as seen during the COVID-19 pandemic and recent inflationary shocks.

Timeless elements of the book include the focus on business fundamentals, the importance of a margin of safety, and the value of independent thinking. Modern investors can leverage technology—such as automated stock screeners and intrinsic value calculators—to implement these principles at scale. Platforms like Value Sense make it easier than ever to apply Buffett’s methodology, democratizing access to high-quality investment research.

In summary, the book’s principles are both enduring and adaptable. While the tools and context may change, the core ideas—invest in what you understand, demand a competitive advantage, and let compounding work over time—are as relevant in the digital age as they were in Buffett’s early years. By staying true to these fundamentals, investors can navigate the complexities of today’s markets with confidence and clarity.

Most investors waste time on the wrong metrics. We've spent 10,000+ hours perfecting our value investing engine to find what actually matters.

Want to see what we'll uncover next - before everyone else does?

Find Hidden Gems First!

Implementation Guide

- Start with a Quality Screen: Use a stock screener (such as the Value Sense platform) to filter for companies with consistently high gross profit margins (above 40%), strong returns on equity, and low debt-to-equity ratios. Focus on sectors and industries you understand well, and prioritize businesses with stable or growing market share. Begin by building a watchlist of 20–30 candidates that meet these quantitative and qualitative criteria.

- Conduct In-Depth Financial Analysis (Weeks 1–4): For each company on your watchlist, download and review the last five years of financial statements. Calculate key ratios: gross profit margin, operating margin, return on equity, current ratio, and free cash flow yield. Read footnotes for information on accounting changes, off-balance-sheet liabilities, or unusual items. Eliminate any companies with declining fundamentals, excessive leverage, or erratic earnings. Narrow your list to 5–10 high-quality prospects.

- Construct Your Portfolio (Month 2): Allocate capital to 5–10 companies, aiming for equal-weighted or conviction-weighted positions. Limit any single holding to no more than 20% of your total portfolio to manage risk. Consider diversification across industries, but avoid over-diversification that dilutes your best ideas. Use limit orders to buy shares at or below your estimate of intrinsic value, ensuring a margin of safety of at least 20–30%.

- Ongoing Portfolio Management (Quarterly Reviews): Review each holding at least once per quarter. Reassess business fundamentals, management quality, and competitive positioning. Track changes in financial ratios and monitor news for signs of disruption or strategic shifts. Rebalance only if a company’s fundamentals deteriorate or if it becomes significantly overvalued. Resist the urge to trade based on short-term price movements or market noise.

- Continuous Improvement and Learning (Ongoing): Commit to ongoing education by reading annual reports, investment books, and financial news. Use resources like Value Sense to access new stock ideas, valuation models, and research tools. Join investment communities, attend webinars, and seek feedback from experienced investors. Periodically review your investment process and update your criteria as you gain experience. Continuous learning and disciplined process improvement are essential for long-term success.

--- ---

10+ Free intrinsic value tools

For investors looking to find a stock's fair value, our analytics team has you covered with intrinsic value tools:

📍 Free Intrinsic Value Calculator

📍 Reverse DCF & DCF value tools

📍 Peter Lynch Fair Value Calculator

📍 Ben Graham Fair Value Calculator

📍 Relative Value tool

...and plenty more.

🔍 Explore all these tools for free on the Value Sense platform and start discovering what your favorite stocks are really worth.

FAQ: Common Questions About Warren Buffett and the Interpretation of Financial Statements

1. What makes this book different from other investment guides?

This book stands out for its practical, step-by-step approach to financial statement analysis, grounded in Warren Buffett’s actual investment process. Unlike generic investing books, it demystifies the numbers and focuses on real-world application, using Buffett’s own investments as case studies. The authors break down complex concepts into actionable checklists, making it accessible to both beginners and advanced investors. Its emphasis on durable competitive advantage and long-term wealth creation sets it apart from more speculative or trend-driven investing guides.

2. Do I need an accounting background to benefit from this book?

No, the book is written in plain English and is designed for readers without a formal accounting background. The authors explain each financial statement line by line, providing definitions, examples, and practical tips. They use real company data and simple calculations to illustrate key concepts. Even if you’re new to investing, you’ll find the explanations clear and the checklists easy to implement in your own analysis.

3. How can I apply the book’s lessons to today’s technology companies?

The book’s principles are highly adaptable to modern tech companies, which often rely on intangible assets and network effects. Focus on identifying durable competitive advantages, such as strong brands, intellectual property, and recurring revenue models. Analyze gross profit margins, free cash flow generation, and balance sheet strength. The framework helps you filter for quality and resilience, even in fast-changing industries like software, cloud computing, or digital media.

4. Is this book only for value investors, or can growth investors benefit too?

Both value and growth investors can benefit from this book. While it draws from Buffett’s value investing roots, it also incorporates his evolved approach, which blends value and growth by seeking companies with strong moats and long-term earnings potential. The emphasis on financial discipline, competitive advantage, and intrinsic value is relevant for any investor looking to build a robust, long-term portfolio—regardless of style.

5. How often should I review financial statements as an investor?

It’s recommended to review the financial statements of your portfolio companies at least once per quarter, coinciding with earnings releases. For new investments, conduct a thorough five-year analysis before buying. Ongoing monitoring helps you spot changes in fundamentals, management quality, or competitive dynamics. Regular review ensures you stay informed and can make timely decisions to protect and grow your capital.