5 Most Undervalued Chip Stocks Right Now: Value Sense Algorithm's Top Picks

Welcome to Value Sense Blog

At Value Sense, we provide insights on the stock market, intrinsic value tools, and stock ideas with undervalued companies. You can explore our research products at valuesense.io and learn more about our approach on our site.

The semiconductor industry has experienced significant volatility recently, creating potential opportunities for value investors. After analyzing market data, we've identified five chip stocks that appear substantially undervalued according to our proprietary algorithm. Here's an in-depth look at each company and why they made our list.

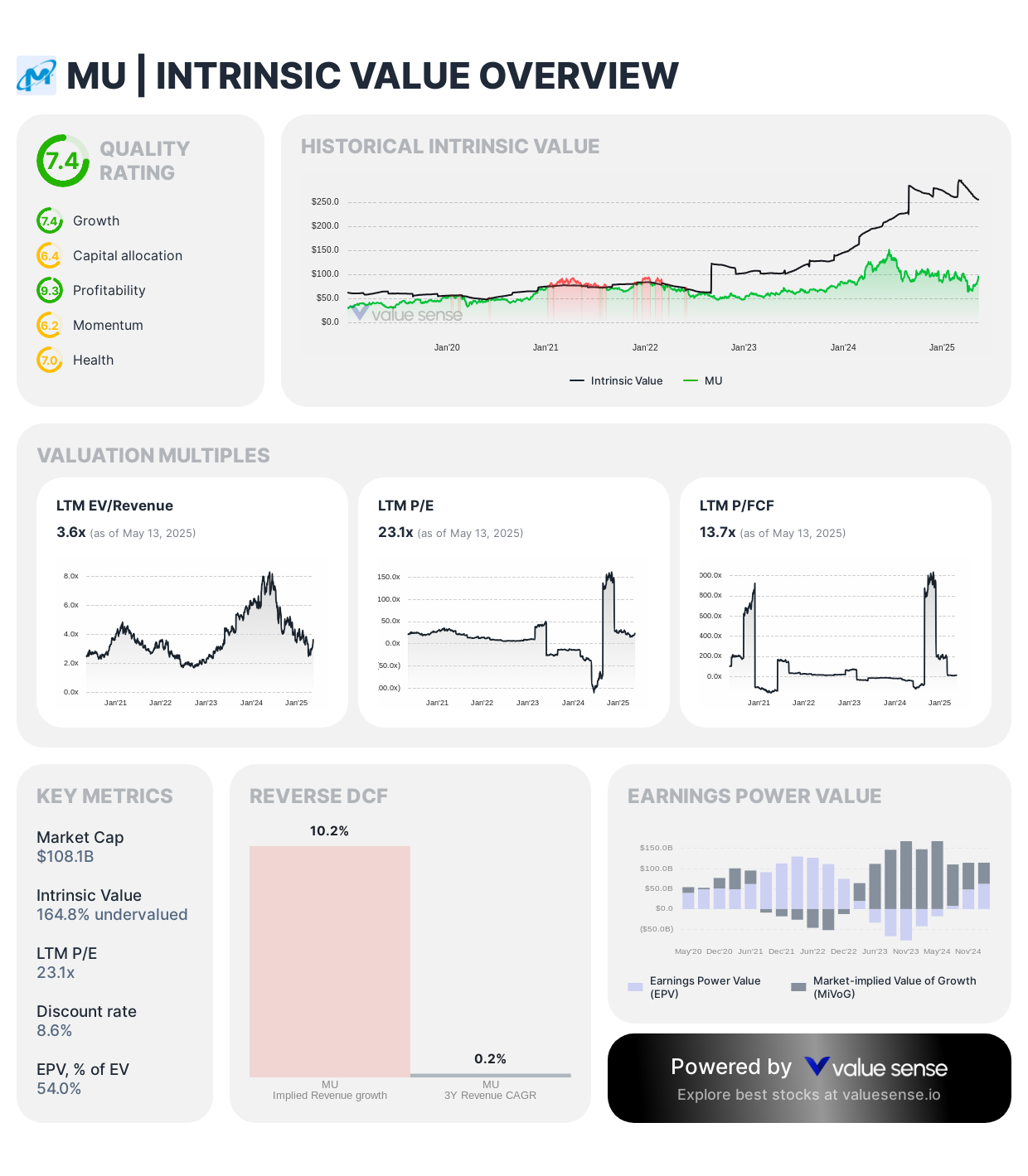

1. Micron Technology (MU): The Memory Giant

Current Valuation Status: 164.8% Undervalued

Micron Technology leads our list with impressive fundamentals:

- Market Cap: $108.1B

- Intrinsic Value: $256.7 per share

- Quality Rating: 7.4/10

- LTM P/E: 23.1x

- Free Cash Flow: $7.87B

Micron's valuation metrics suggest significant upside potential. The company maintains strong profitability with negative 20.9% returns while generating substantial free cash flow. As a leader in memory and storage solutions, Micron's position strengthens as data center demand and AI applications continue to grow.

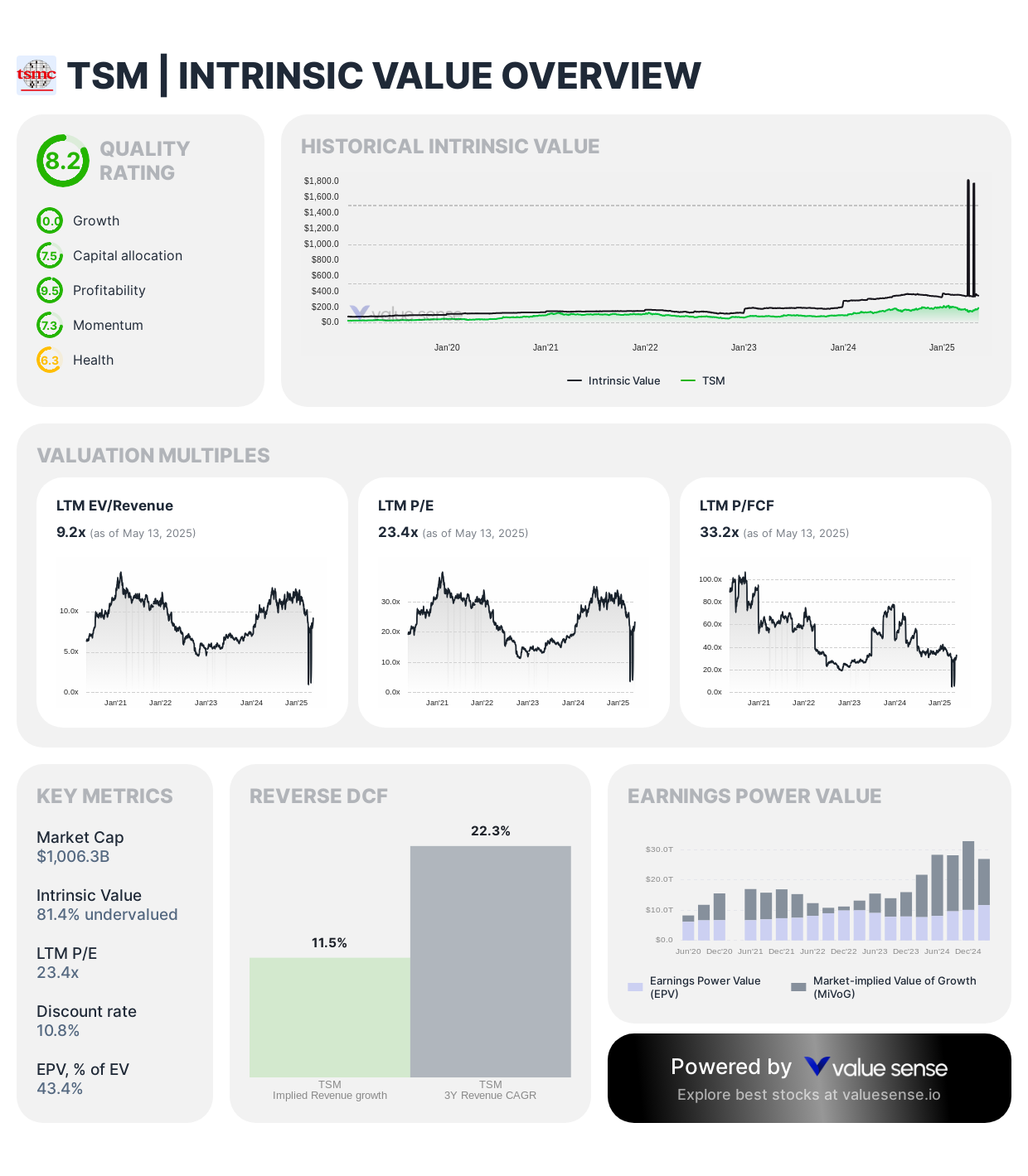

2. Taiwan Semiconductor Manufacturing (TSM): The Foundry Leader

Current Valuation Status: 81.4% Undervalued

TSMC remains the world's largest contract chip manufacturer:

- Market Cap: $1.006T

- Intrinsic Value: $352 per share

- Quality Rating: 8.2/10

- LTM P/E: 23.4x

- Revenue: $3,140.9B

TSM's dominant position in advanced chip manufacturing makes it indispensable to the tech industry. Despite geopolitical concerns, the company's exceptional quality rating and consistent profitability support its undervalued status.

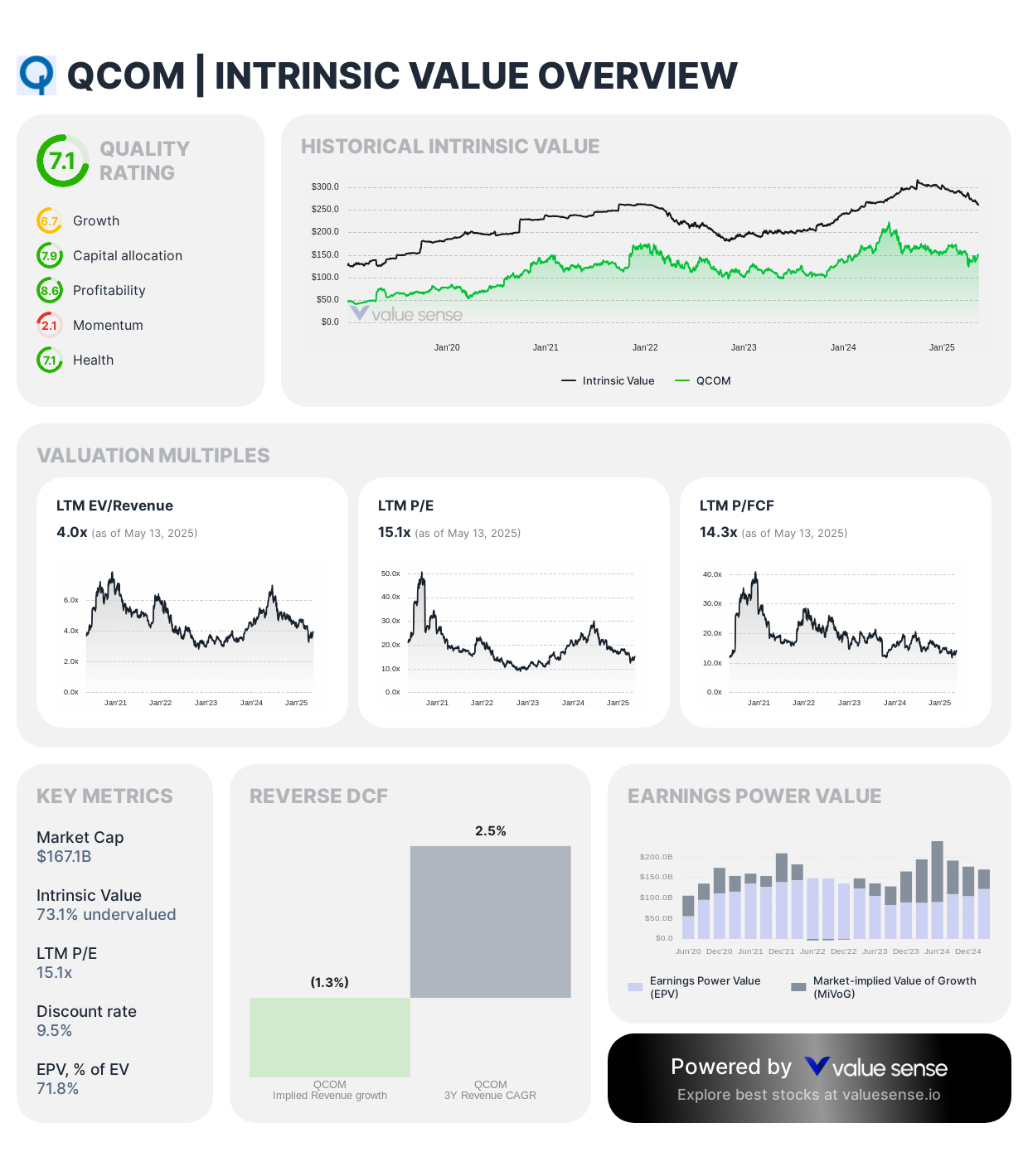

3. Qualcomm Incorporated (QCOM): 5G and Beyond

Current Valuation Status: 73.1% Undervalued

Qualcomm's diversification strategy appears to be paying off:

- Market Cap: $167.1B

- Intrinsic Value: $261.9 per share

- Quality Rating: 7.1/10

- LTM P/E: 15.1x

- Free Cash Flow: $11.7B

With strong positions in smartphone chips and expanding automotive markets, Qualcomm's 16.1% revenue growth demonstrates its successful transition beyond traditional mobile markets.

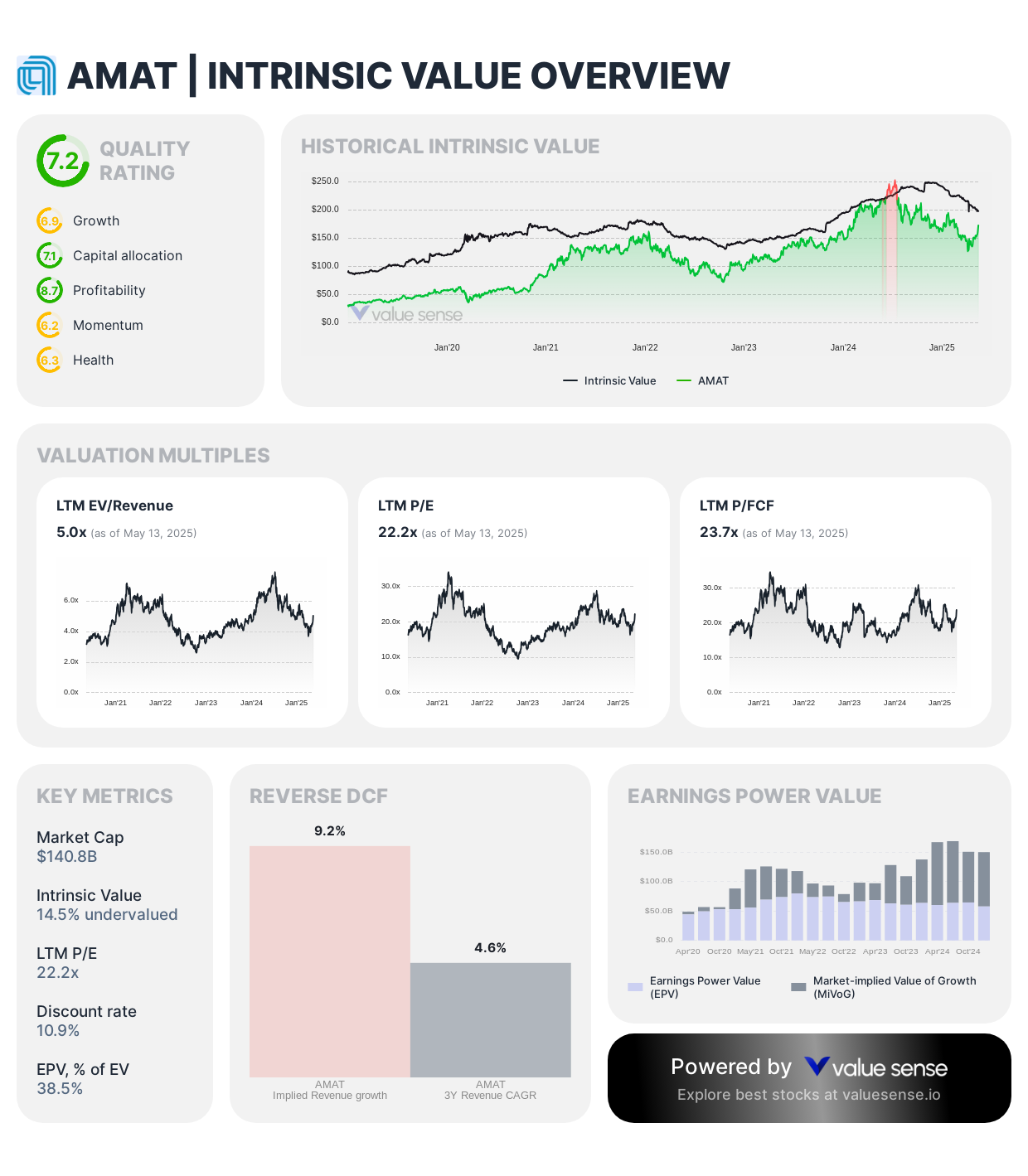

4. Applied Materials (AMAT): Enabling Chip Innovation

Current Valuation Status: 14.5% Undervalued

Applied Materials provides critical semiconductor manufacturing equipment:

- Market Cap: $140.8B

- Intrinsic Value: $198.2 per share

- Quality Rating: 7.2/10

- LTM P/E: 22.2x

- Free Cash Flow: $5.94B

As chip complexity increases, AMAT's equipment becomes more essential. The company's 38.5% earnings power value percentage indicates strong operational efficiency.

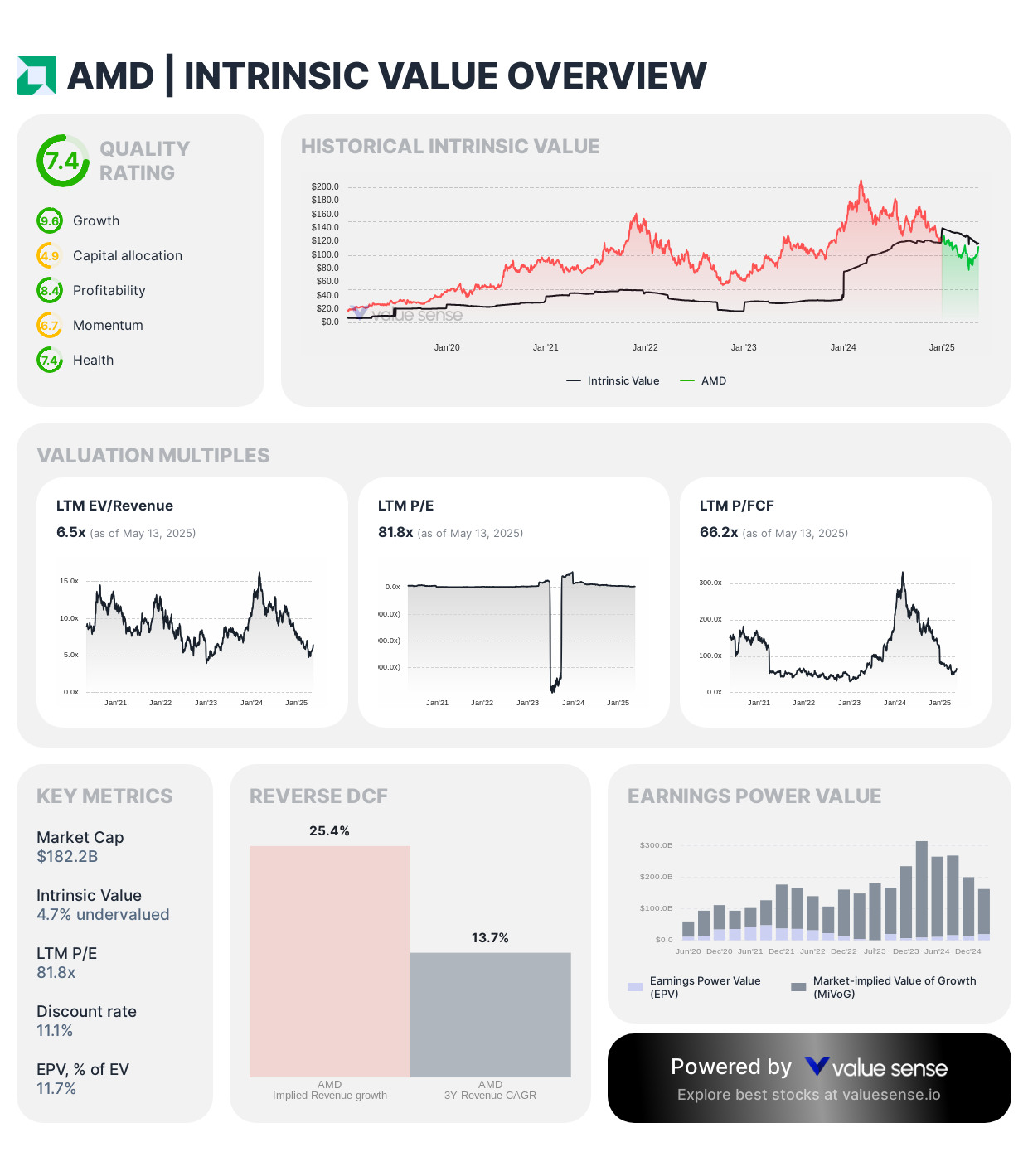

5. Advanced Micro Devices (AMD): The Data Center Disruptor

Current Valuation Status: 4.7% Undervalued

AMD rounds out our list with impressive growth metrics:

- Market Cap: $182.2B

- Intrinsic Value: $117.8 per share

- Quality Rating: 7.4/10

- LTM P/E: 81.8x

- Revenue Growth: 21.7%

Despite its high P/E ratio, AMD's aggressive market share gains in data centers and AI accelerators justify premium valuations. The company's discount rate of 11.1% reflects moderate risk levels.

Investment Considerations

Key Factors Supporting These Valuations:

- AI Revolution: All five companies benefit from AI infrastructure buildout

- Supply Chain Stabilization: Post-pandemic recovery improving margins

- Diversification: Expansion beyond traditional markets (automotive, IoT, edge computing)

- Strong Cash Flows: Healthy balance sheets supporting R&D investments

Risk Factors to Monitor:

- Geopolitical tensions, particularly US-China relations

- Cyclical nature of semiconductor demand

- Potential overcapacity in certain chip segments

- Technology transition risks (especially for memory manufacturers)

Conclusion

Our algorithm identifies these five semiconductor stocks as presenting compelling value opportunities. Each company demonstrates:

- Strong quality ratings (all above 7.0)

- Significant gaps between market price and intrinsic value

- Robust cash flow generation

- Strategic positioning in growth markets

While past performance doesn't guarantee future results, these undervalued chip stocks merit consideration for investors seeking exposure to the semiconductor sector. The combination of fundamental strength and valuation discounts could provide attractive risk-reward profiles for patient investors.

Disclaimer: This analysis is based on algorithmic calculations and should not be considered investment advice. Always conduct your own research and consult with financial professionals before making investment decisions.

Explore More Investment Opportunities

For investors seeking undervalued companies with high fundamental quality, our analytics team provides curated stock lists:

📌 50 Undervalued Stocks (Best overall value plays for 2025)

📌 50 Undervalued Dividend Stocks (For income-focused investors)

📌 50 Undervalued Growth Stocks (High-growth potential with strong fundamentals)

🔍 Check out these stocks on the Value Sense platform for free!

More Articles You Might Like

📖 How Big Tech Makes Money

📖 The Definitive Guide to Finding Operational Metrics & KPIs

📖 15 High ROIC Stocks With 5%+ FCF Yields

FAQ: 5 Most Undervalued Chip Stocks Right Now

Q1: What are the most undervalued chip stocks according to algorithmic analysis?

A: According to our algorithmic analysis, the five most undervalued chip stocks are:

- Micron Technology (MU) - 164.8% undervalued

- Taiwan Semiconductor Manufacturing (TSM) - 81.4% undervalued

- Qualcomm (QCOM) - 73.1% undervalued

- Applied Materials (AMAT) - 14.5% undervalued

- Advanced Micro Devices (AMD) - 4.7% undervalued

Each stock shows a significant gap between its current market price and intrinsic value, with quality ratings above 7.0.

Q2: Why is Micron Technology considered the most undervalued semiconductor stock?

A: Micron Technology is considered the most undervalued with an intrinsic value of $256.7 per share, representing a 164.8% upside from current levels. The company boasts strong fundamentals including:

- $7.87B in free cash flow

- 71.1% revenue growth

- Quality rating of 7.4/10

- P/E ratio of 23.1x These metrics suggest the market hasn't fully recognized Micron's value, especially given growing demand for memory chips in AI applications.

Q3: Which semiconductor companies benefit most from AI growth?

A: All five undervalued chip stocks benefit from AI growth, but in different ways:

- Micron: Supplies high-bandwidth memory essential for AI training

- TSMC: Manufactures advanced chips for AI processors

- Qualcomm: Develops AI chips for edge computing and smartphones

- Applied Materials: Provides equipment for manufacturing AI chips

- AMD: Produces data center GPUs competing directly in AI acceleration

Each company plays a crucial role in the AI infrastructure buildout.

Q4: What valuation metrics determine if a chip stock is undervalued?

A: Key valuation metrics for semiconductor stocks include:

- Intrinsic Value: Calculated using discounted cash flow analysis

- P/E Ratio: Price-to-earnings multiple compared to industry averages

- Free Cash Flow: Indicates financial health and dividend potential

- Quality Rating: Comprehensive score considering growth, profitability, and momentum

- Revenue Growth: Year-over-year expansion rates

Our algorithm weighs these factors to identify stocks trading below their fair value.

Q5: What risks should investors consider when buying undervalued semiconductor stocks?

A: Key risks for semiconductor investors include:

- Cyclical Demand: Chip industry experiences regular boom-bust cycles

- Geopolitical Tensions: US-China relations affect companies like TSMC

- Technology Transitions: Rapid innovation can make products obsolete

- Supply Chain Disruptions: Manufacturing complexities create vulnerabilities

- Competition: Intense rivalry can pressure margins

Despite these risks, the current undervaluations and strong fundamentals suggest favorable risk-reward profiles for patient investors.